Why did the rent-to-income ratio rise in the 1980s but stay flat ever since?

Because of compositional changes that led to fewer tenants paying below market rents.

I’ve previously argued that the market equilibrium for housing rents is at a fixed proportion of household income.

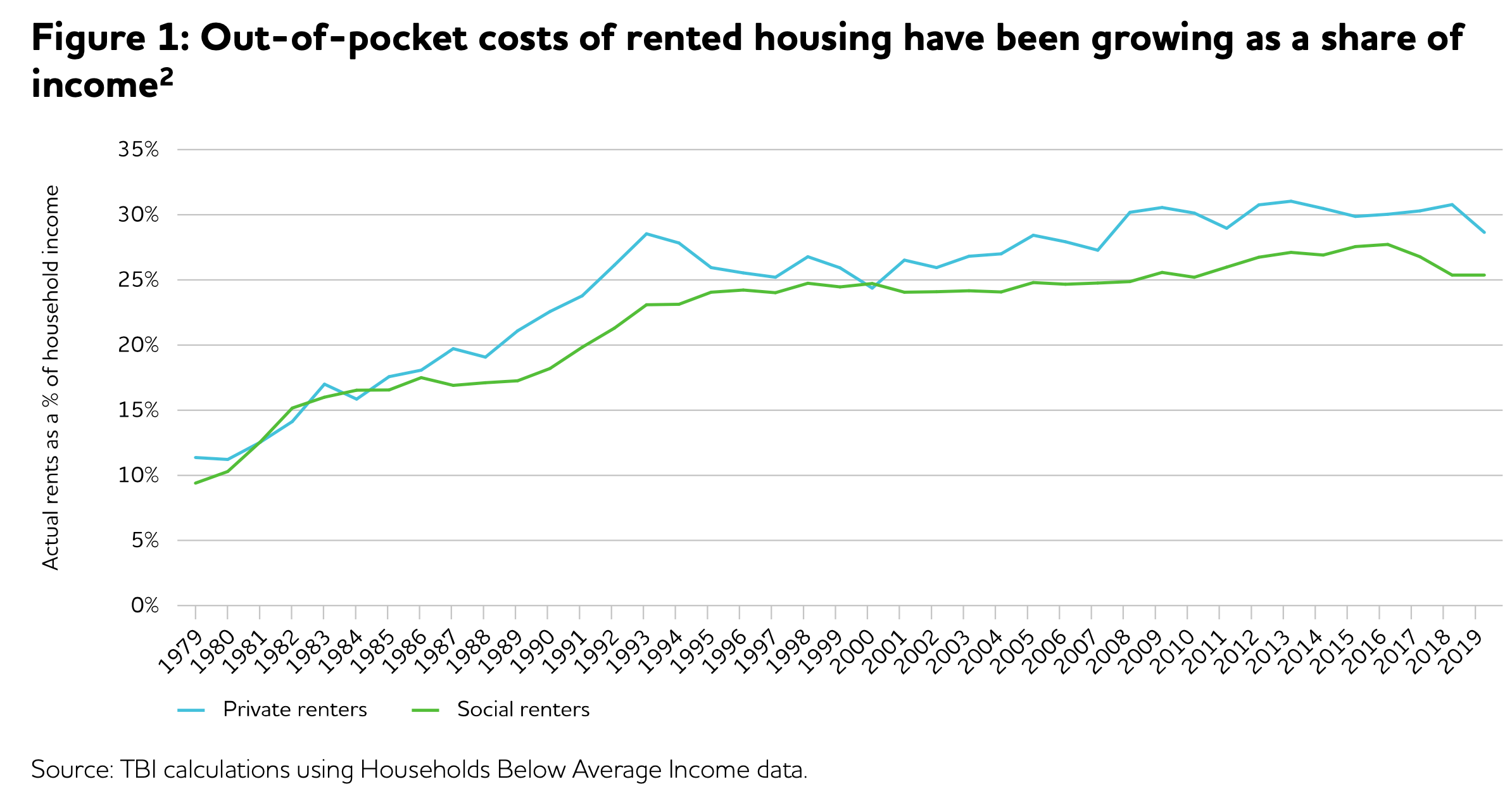

A flat rent-to-income ratio is common in many countries since the 1990s. But prior to that, rent-to-income ratios were much lower. They grew substantially during the 1980s before flattening out. I speculated about why that was the case.

I suspect the lower pre-1980s rent-to-income ratios had something to do with public and council housing options keeping a lid on the private market equilibrium.

Now, Ian Mulheirn and colleagues have tried to solve this puzzle in their report, Housing affordability since 1979: Determinants and solutions. Their main data shows the general trend of rising rental costs compared to income during the 1980s in the United Kingdom which then flattened out.

They provide a detailed answer for the 1980s rent-to-income increase, with the conclusion being that

[t]he erosion of subsidies explains the decline in housing affordability for renters over the past 40 years.

Those subsidies include all policies that create a wedge between the market rental price and the price actually paid by tenants—cash support for renters, public housing, and rent controls. Therefore, the once of increase in the rent-to-income in the 1980s was the result of

the unwinding of rent controls in the private sector

reducing the scale of heavily subsidised public housing, and

scaling back cash support for renters.

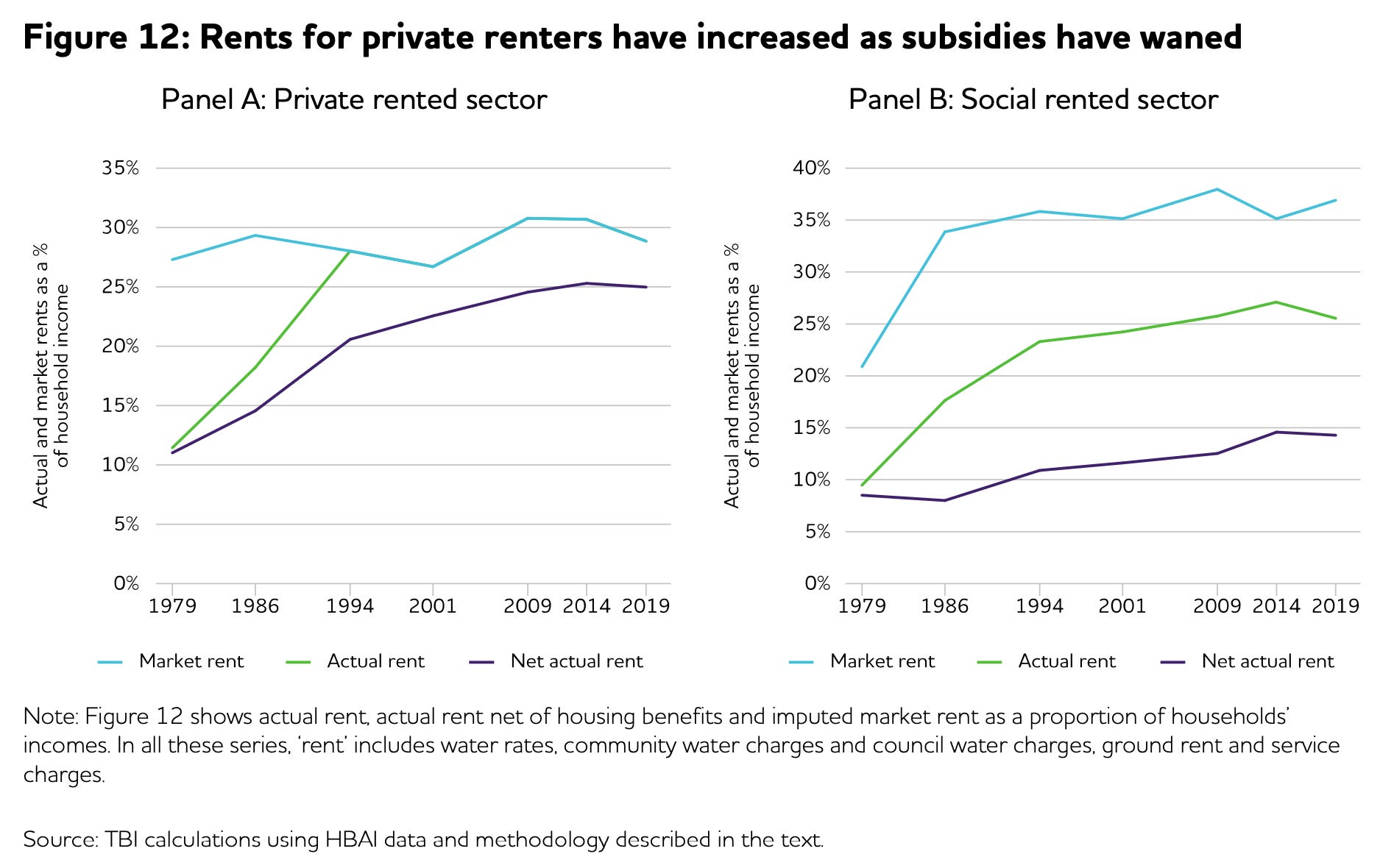

We can see that most clearly with their estimate of counterfactual market rent-to-income ratios in the private sector (left panel, blue line) which were flat throughout the 1980s up until today. So the mystery of rising rent-to-income is not a mystery of how the market changed, but of who was actually paying the market rent.1

They explain that

The private rented sector was small, only 11.5% of the housing stock in England in 1979, and subject to rent controls that made owning rental property unattractive. The size of the sector had been gradually declining over time as landlords sold up and few new properties entered the rental market. By contrast, the social rented sector was much larger at 30% of the housing stock in England and, as is still the case today, rents were set at affordable levels. As a result, all renters paid rents that were below the levels that would have prevailed in an unrestricted market. (p3)

Also

Forty years ago, almost all private rental property was subject to rent controls through the 'fair rents' system. Tenants could apply to have their rent registered at a 'fair rent' which was supposed to correspond to the rent that would apply in the absence of a scarcity of rental accommodation in the market. (p12)

The mystery is not about the workings of the private property market, but the decline of non-market housing options. Mulheirn sums it all up in this Twitter thread.

Another perspective

Would you believe that a second report on housing in the United Kingdom also came out this week making the exact opposite argument?

The Centre for Policy Studies report, The Case for Housebuilding, argues that it is actually regulation on the location and type of new dwellings that constrains the property market so that below-equilibrium rates of new homes are built each year, leading to above-equilibrium rental prices.

Amongst other things, they agree with the assessment of the rising rent-to-income ratio since the 1970s.

The rising cost of housing is also shown in rents. Whereas private renters spent 10% of their income on housing from the 1960s to the 1980s, rising to 15% in London, the share of income spent on rent has risen to 30% in recent years, and almost 40% in London.

And would you look at this, their whole report seems designed to argue against Mulheirn’s case.

In recent years, thinkers such as Ian Mulheirn (now of the Tony Blair Institute for Global Change) have done valuable work in highlighting that the rise in house prices is not purely down to supply. Factors such as the collapse in interest rates, the surge in global asset prices and the rise of buy to let have increased competition for property and driven up prices. Graham Edwards landmark CPS paper ‘Resentful Renters’set out the scale of the problem, including the extent to which millions of would-be homeowners have been priced out of the mortgage market due to rule changes brought in after the financial crisis.

But some, including Mulheirn on occasion, have gone further to argue that a focus on supply is misguided. He argues that ‘the current focus on boosting housing supply does not offer a solution to the housing crisis’, and that housing supply is not just keeping pace with household formation but increasingly outstripping it. He also argues that rents (which reflect the ‘real’ cost of housing) have not outstripped incomes and this shows no shortage exists.

They strangely go on to show that the housing stock has grown by more than the population and that the gap above the population growth rate has increased in the past decade.

They also show that the change in tenure, especially the decline in social housing since 1980 is significant. Yet they ignore Mulheirn’s main argument about this.

What puzzles me about this report, and the many others of this genre prepared by similar organisations in Australia, the United States, Canada and New Zealand, is that they predictably want more homebuilding than the market seems to supply, yet never propose a public homebuilder to help flood the market to bring down rents and prices. You know, just in case private property owners decide not to do that just because they can.

These reports always side-step crucial questions, like

What’s the relationship between rental price levels and the housing stock?

How few people will live in each home under these radically high supply scenarios?

Why focus on prices diverging from rents or incomes at all, as yield compression cannot be a supply issue?

Why are the same housing patterns happening globally, even in cities people used to think had flexible supply?

They overlook that everyone involved in making rents and prices cheaper in the private market is currently a property owner who benefits from prices and rents rising, not falling. Some kind of massive miscoordination is required, like an asset market panic.

It seems clear to me that Mulheirn’s explanation fits the data best.

For the social rental sector, they explain that “[t]he jump in rent relative to incomes in the early 1980s due to changing composition of social tenants as better-off households took advantage of the right to buy.”

But a rent/income ratio is not like a price of clothes or electronics. The latter items are (at least in US methodology) quality adjusted so that in principle one is comparing the same item over time. Is the rent being compared for the same sq ft, similarly equipped flats? Or even same flats? How are locational differences if any factored in.

You quote Mulheirn saying that a 'fair rent' was "supposed to correspond to the rent that would apply in the absence of a scarcity of rental accommodation in the market."

Mulheirn thus seems to agree that scarcity of rental accommodation results in a higher rent, and if there was an absence of scarcity, rents would be lower. IE the subsidised 'fair rent' is equivalent to what a private renter would pay in the absence of any rent controls BUT with abundant rental accommodation.

This seems consistent with the idea that more rental accommodation would result in lower rents than would otherwise have been the case.

I agree it's odd that proponents of the 'need more supply' view don't go more gung-ho for public construction. I think their argument though is that this is much more expensive to the government budget, compared with private construction. Surely the real question here is what is the taut constraint when it comes to private construction? You argue it is to do with 'future options' and a sort of de-facto coordination, they argue it is planning.