Why are some homes empty?

A new report from Prosper Australia documents this puzzle and asks what insights we can get from this "window onto waiting"

A new report on Speculative Vacancies by Tim Helm, Research Director at Prosper Australia, is out now (full disclosure, I currently do consulting work for Prosper on other projects).

Using water meter data for every residential dwelling since 2018, Tim looked at trends in long-term unoccupied (empty) homes on a suburb-by-suburb basis across Melbourne.

The concept of a long-term empty home is different to what we call housing vacancy, which typically refers to the number of rental advertisements, whether those homes are occupied or not. It is also very different to the concept of empty homes on census night, which is the source of the notorious one million empty dwellings figure.

Looking at this more comprehensive measure of properly empty long-term homes helps illuminate a big unresolved issue in our understanding of housing markets.

As the report says, it is “A window onto the economics of waiting and the hidden barriers to housing supply."

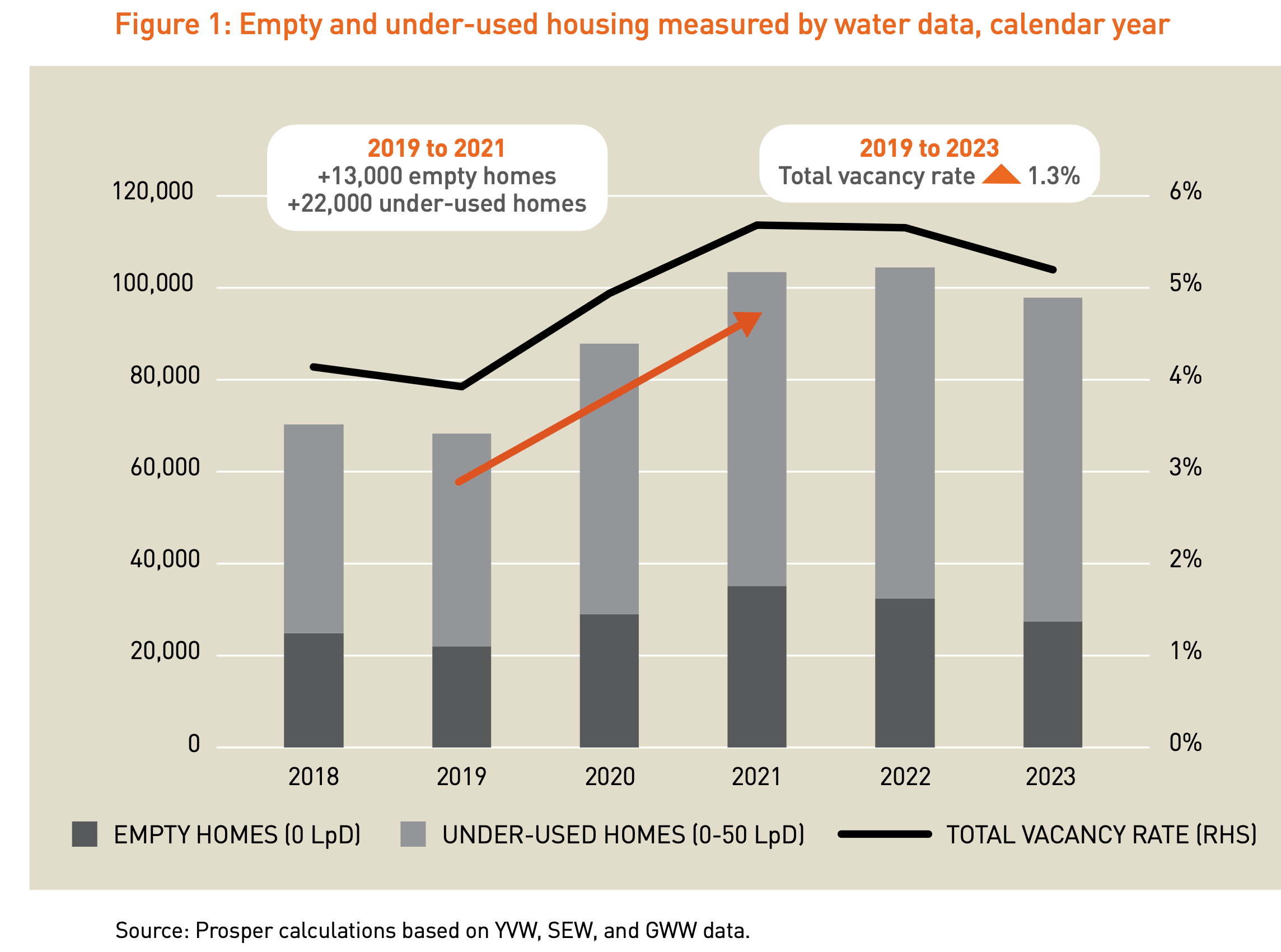

What it shows

The basic story is that the number of year-long empty homes in 31 council areas across Melbourne (excluding 33 postcodes with a high proportion of holiday homes), grew from around 23,000 in 2018 and 2019 (or 1.4% of all dwellings) to over 35,000 in 2021. That’s a one-third increase.

For homes with less than 50L of water use per day over the calendar year, the rate grew from about 3.9% in 2019 to over 5.7% in 2022, before falling a touch in 2023 to 5.2%.

It is also interesting to look back on previous reports and see that in 2012, only about 12,000 dwellings were empty year-round (with no water use) so the number in 2018 was already double the number just six years earlier.

The top ten postcodes in 2023 all had more than 10% of homes using less than 50L of water per day, and a surprising number of postcodes had 3% to 5% of homes with not a drop of water used for 12 months straight.

What it reveals

This is the more interesting part of the report. Let me quote at length.

We don’t understand vacancy well. There is little research on what drives it, partly due to limited measurement.

Some explanations centre on growth- focused investment strategies, investor inattention, tax avoidance, drawn-out estate settlements, loan conditions for investors, and slow adjustment of price expectations. But there is little evidence on which factors matter most or which policies would have the biggest impact.

On another level vacancy can be explained as a result of inequality – a sign that renters cannot afford to outbid the convenience value of an empty investment property. Some homes remain empty simply because their wealthy owners feel no need to use them.

The economic explanation boils down to the relative value of flexibility versus yield. The decision to leave a home vacant depends on the trade-off between option value and cash returns. (The next section explains how this also applies to land development.)

Empty property offers more options. If rents are low, landlords can avoid locking in low returns and the challenge of raising rent later. When sales prices are low, vendors can postpone sale, keeping the property untenanted to ensure the buyer pool includes owner-occupiers. If an owner plans to occupy their property in the future, keeping it empty makes this easier. The idea that property owners balance flexibility against yield is a catch-all explanation for these many and varied situations.

When flexibility is valued highly, leaving property empty is rational. As a stylised numerical example, with a net rental yield of 2.5% and a 5% sale price premium on an untenanted home, an investor waiting for optimal selling conditions would profit by keeping it vacant for up to two years.

The value of flexibility over yield is higher when yields are low and property is valued more significantly as a growth investment. This has been the case in recent decades, with low and falling interest rates. Taxing capital gains less than rental income reinforces this trend.

What about empty homes taxes?

These types of taxes, which add to the cost of flexibility of holding housing empty, seem to work to reduce empty homes and raise revenue. Here’s a table listing eleven such taxes from cities around the world.

Victoria has an empty home tax on its way.

The problems they often face are in the monitoring and enforcement. How do you prove vacancy? How can criteria be gamed?

My thoughts

I don’t think the fact that there are over 30,000 empty homes in Melbourne is what is causing rents and prices to rise. Melbourne has been a world leader in its rate of new home building in the past 15 years or so.

So I hope people don’t interpret the report as saying that this is the cause of prices.

I see it as, like the subtitle suggests, offering a window onto the economics of waiting—in other words, the value of flexibility. This is a very much overlooked feature of property markets and applies much more to vacant land without any homes than occupied land with empty homes.

Any theory of housing production (converting developable sites into homes) and housing utilisation (getting empty homes occupied) much grapple with the dynamic where waiting pays.

An interesting coincidence is that Canada’s CBC did some reporting on empty condos in Toronto a couple of weeks back too. Seems like empty homes are a normal feature of market adjustments, and we need to understand this if we want to understand housing supply in general.

Thanks for sharing Cameron

I do wonder how many vacant properties there are with gardens that require watering

Ipswich, Stonnington.