We're at the TAX BREAKS stage of the PROPERTY CYCLE

We've used monetary policy to try and stop homes being built. Now, those losing out are blaming charges that fund infrastructure and want a bail out.

As I explained in The Great Housing Hijack, property markets go in cycles and policy debates follow behind.

We are now at the point of the cycle where we debate taxes on new development levied to help fund associated infrastructure—infrastructure charges, developer charges, or impact fees.

Although the policy debate is resurfacing in Australia too, Canada’s property cycle is a little ahead, so that is where the debate has really heated up. There, removing GST on new homes is another policy target.

For example, here’s a property guy having a whinge, and another. Here’s an organised lobby campaign with its taxopoly board game designed to draw attention to the issue.

And here are two recent Canadian podcasts on the topic.

Tax policy lobbying is the next phase of the naked rent-seeking cycle. During the asset price boom, property owners told stories about zoning in order to get highly valuable planning changes applied to their property—higher prices meant higher allowed densities became more valuable to landowners.

Now, during the asset price bust, they want a bailout in the form of a tax break.

I’m sure all the property developers in the sector feel like they are trying to do the right thing and that taxes and regulations are limiting what they can do. But remember, markets aren’t forcing anyone to buy a property with certain planning regulations or taxes.

I want to get into the details of the often-forgotten economics in these debates.

But before I do a quick note.

Right now, Australia and Canada's monetary policy settings are trying to stop new home construction. Sure, Canada has seen a few rate cuts recently. But for over two years, from early 2022, the policy intention has been to slow homebuying and hence reduce prices and homebuilding.

So when people who build homes complain that no one is buying, what should we think?

We don’t want people buying new homes and soaking up construction workers and materials right now, contributing to inflation.

If tax changes did spur an enormous building boom, we would have to increase interest rates more to meet inflation targets. Weirdly, we too often ignore this.

Some background

In 2010 I worked at the Queensland Competition Authority assessing council calculations of infrastructure charges against the required legal method. This method was established in 2003 in response to the development industry arguing that councils were over-charging with fees on new development with no basis.

They thought it was a money grab.

The basic idea of the policy then was to ensure that new projects only paid for the additional capital needed to service them in the major infrastructure networks. To do this, required planning for infrastructure needs and costing major works in different parts of each city. Then, charges to recover only these additional costs could be levied on new projects. Since charges would be location-based, it would send a price signal about which locations were cheapest to service with new trunk water, sewer, road, parks and stormwater infrastructure.

As it was common practice for new projects to pay for their local infrastructure connections, these costs were based only on necessary trunk upgrades to accommodate the growth that was not covered by such arrangements.

Those costing efforts showed that some parts of each city were cheap to service for new development, while other parts were expensive. Charges would vary in some cases between $5,000 to $40,000 per dwelling depending on the location, reflecting differential infrastructure costs in different parts of the city.

After the financial crisis property downturn, a task force was established to review the charges. Soon after that review was completed in 2011 it was announced that the prior policy was no longer applicable and a fixed charge per dwelling statewide be adopted.

Unlike much of today’s commentary, that task force didn’t blame these charges for the downturn in development.

Queensland’s infrastructure charging regime is not the major reason the property market is experiencing a downturn, just as Queensland’s infrastructure charging regime was not the reason Queensland outperformed the country for the most part of the last decade. The global financial crisis has resulted in tighter lending conditions and higher financing costs while market participants are more risk averse.

Instead, the review reflected the simple fact that most property owners didn’t want to pay for the full cost of infrastructure for their potential future projects and wanted others to pay instead.

To be clear, in Queensland we implemented a complex costing process to tie charges to costs because property developers thought they were being overcharged. Since that didn’t result in most charges falling, we got a new story about complexity, which got the charges capped statewide.

One predictable outcome has been that development in expensive-to-service locations is now subsidised by development in cheap-to-service locations.

But an unexpected outcome has been how the fixed charge has side-stepped constant political battles over whether charges were justified by costs, and whether the right infrastructure was being planned and priced.

Perhaps this cycle, however, we will revisit the Canadian experience and argue again that it is an unjustified and arbitrary cash grab and switch back to the initial arguments.

And so the cycle goes.

Economics of developer charges

I think the most important economic questions about how these charges affect housing and property markets are:

Should new development pay the full cost of development, both on-site and off-site capital works?

How do taxes and charges on new development affect housing prices and the feasibility of projects?

Should growth pay for growth?

No one disputes that those who want a new home should pay for the construction cost of that home.

They should pay for the kitchen and bathroom. And also the water and sewer pipes. But to where should they pay for these pipes? Just to the property boundary? Who will pay to connect beyond that point and for the rest of the capital in the system that is needed to accommodate the extra dwellings?

They should pay for the garage and driveway. But what about connecting the new home via road to the existing network?

The overarching economic question is whether we get more efficient outcomes if all costs of a decision to build new homes are internalised into that decision.

That was the logic in Queensland of actually planning for the necessary trunk infrastructure for growth and costing it, then charging different parts of the urban area based on those differential costs of growth.

If development chargers do reflect the actual costs of off-site capital needed to accommodate new housing, then arguably they are making housing outcomes more economically efficient by using the price mechanism to pay for these costs, even if that means fewer homes are built. Any alternative is equivalent to subsidising new homes and hence getting an inefficient number of homes relative to other unsubsidised new goods and services.

Now, I don’t think this is the case. Most of the effects are on prices and locations, not quantities. But I think it is important to show that the argument for not fully pricing the cost of off-site capital in the price of new homes is an argument for subsidising new homes.

Lastly, I think it is important to note that rising infrastructure costs reflect the same rising inflation and costs that are in on-site construction too. So yes, developers must deal with rising construction costs and rising development charges. But you can equally say that they are dealing with rising construction costs for on-site and off-site capital, and one of these is paid with a construction contract and one of these is paid with a development charge.

The effect of charges on prices, locations, and quantities of homes

The bigger question here concerns the effect of pricing infrastructure as part of the cost of new homes on the price, location and quantity of new homes.

The effect on price is the simplest.

Generally, these charges do not affect prices. You can download a research paper I wrote demonstrating this below.

In short, when Queensland changed back to fixed developer charges, some areas needed to reduce their charges, and others had to increase them. I was able to see if prices for new homes increased or decreased to match.

As you might have guessed, prices didn’t follow.

So property owners who got lower charges kept the gains, and those who got higher charges lost out.

But surely you might say, higher costs of development must get passed on to housing prices and rents somehow?

What they mostly do is change the location and density that is optimal to build.

I explain all the nitty gritty details in this report I wrote for Auckland Council in 2022. Please enjoy.

Density

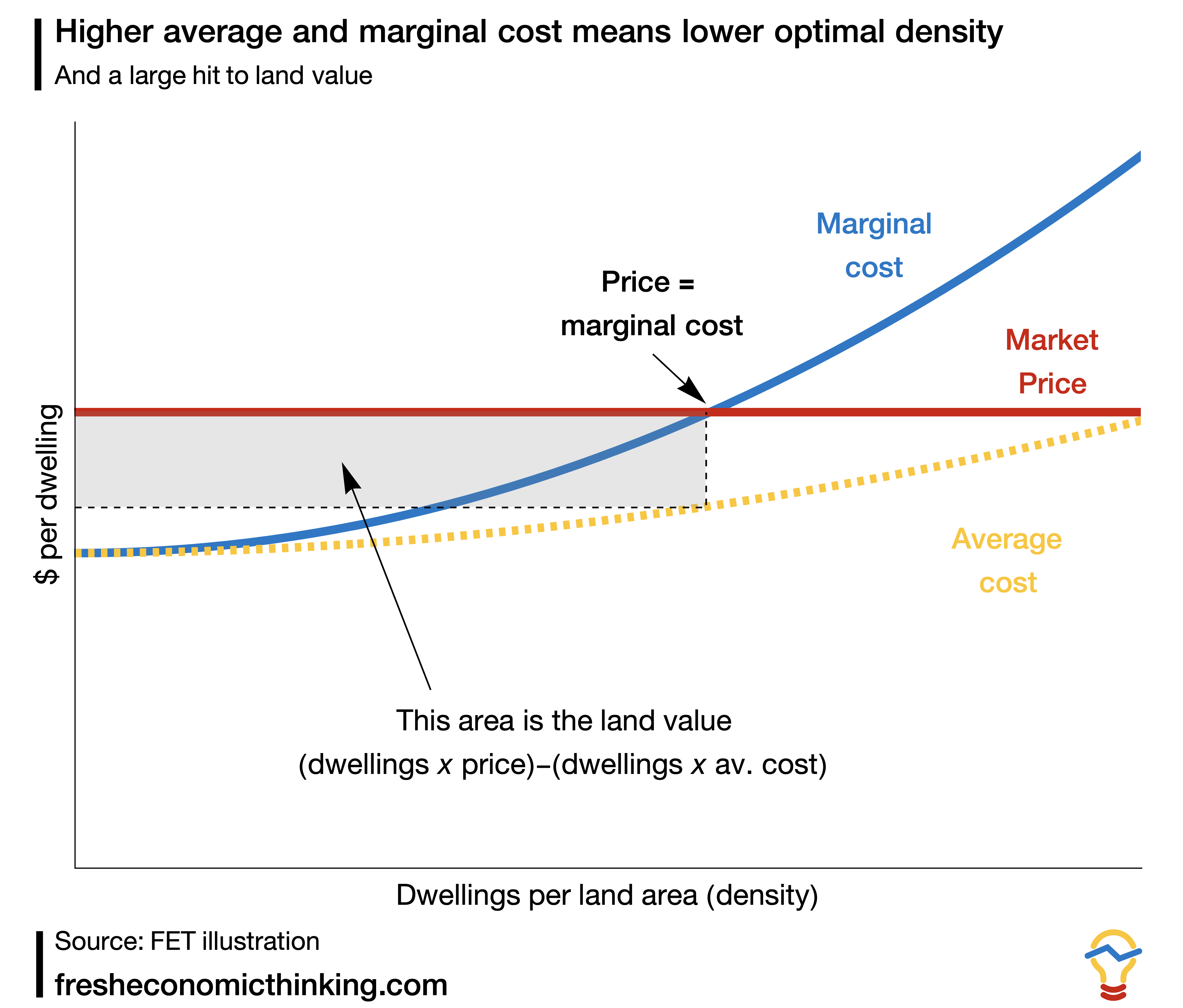

Consider how the density of a project is determined. Where allowed, apartment towers will be built at a density where the marginal cost of going higher equals the market price.

This maximises the gap between total revenue and total cost at the time of development (as shown below). Sometimes regulations intervene and densities below this are the limited maximum.

Now consider what happens when an extra fixed cost per dwelling is added. This increased both the average and marginal costs of density by a fixed amount per dwelling, shifting both curves vertically.

The effect is to decrease the optimal density and decrease the value of land (the gap between total revenue from a project and total price).

This smaller project might still be feasible, just as is often the case when regulations limit density.

But doing this project today means locking in the lower total economic gain from development. Investing in getting charges on new developments removed is probably a better investment than building a lower density housing project today.

Just like the charges change slightly the optimal density, they will change the potential locations too, by making some marginal sites unfeasible today that might otherwise be.

But remember, the pool of feasible sites is generally extremely large. The rate at which projects out of that pool are developed into new homes depends not on which density is most profitable, but whether the trade-off to waiting or building now is worth it.

Currently, waiting pays, as intended by the monetary tightening of recent years.

For more, please read this article where I dive into the details.

History of lobbying

In response to Australia’s history of lobbying to have taxes and charges on property removed, I wrote a paper in 2021 debunking many of the claims, which you can download below.

As a quick summary, taxes on property assets decrease the value of the asset.

Property prices don’t come from a summation of costs.

We know that removing stamp duty (land transfer tax) in property transactions, for example, simply means that the seller gets that money instead of the state for the same total cost to the buyer.

And if you want to double count stamp duty for both the land purchase and developed housing purchase, then why not keep going and count the taxes paid by the previous owner? Don’t they all add up?

Land value taxes are a more interesting inclusion in these calculations, as they are payable whether you build to not, and you will pay less land tax if you build faster. So only the choice of the property owner to not build quickly adds to land value taxes paid.

So what?

In Canada today it seems like the story has switched. Just a few years back it was zoning and planning getting in the way of new housing. Now, you have a developer with 11,000 approved new condos telling us that this wasn’t correct, and that actually it is the charges for new infrastructure that are the problem (listen to the first linked podcast above).

Is there ever a time that the development industry doesn’t need a bailout?

Crazier still is that he also said that they will pass on reductions in developer charges to buyers.

If they do this, then projects are not more feasible than they are now. You save, say, $10,000 per dwelling on the cost side, but get $10,000 per dwelling less revenue.

If no one is buying, prices will automatically fall regardless of changes to developer charges. Property owners will respond by adjusting where they build projects and at what density.

And, I know it’s crazy, but those developers who made the wrong bets and were too optimistic when they bought sites may have to sell them at a discount and realise the loss on that bet.

A small example from the US. https://www.smdailyjournal.com/news/local/redwood-city-keeps-park-fees-for-market-rate-developers/article_6552a948-38d7-11ef-88ec-73d96066f7d6.html#tncms-source=login

Here, Redwood City was considering reducing park impact fees for housing projects already in the pipeline. Thankfully they did not.

I shared with council an article from the same local paper describing that in a nearby town, nine approved projects, including housing projects, were on hold waiting for lower interest rates and higher rents.

Basically the points you make here. Some how I think the meme "pushing a string" applies here. This string needs to be pulled.

One neat and subtle point you make, that I had not considered, is that one cannot believe reduced fees would both expedite construction AND reduce rents. If fee reductions lowered rents, project revenues-less-costs would be unchanged, and time-to-market decisions would be unchanged.

This is a solid breakdown—removing developer charges isn’t a magic fix. Market dynamics and monetary policy still drive timing, location, and density.