Supply and demand: The NESTED nature of trading dimensions (Part III)

When economists talk about marginal costs do they know which margin? Let's think more clearly about ALL the margins.

In Part I of this Supply and Demand Series, I explained with a clean example of supermarket checkout queues the underlying logic of supply and demand in a market. Housing is a market where trade-offs must be made, so supply and demand must apply.

I explained how supply and demand are tools for helping understand the concept of a market equilibrium, noting that this is the imaginary point where there are no longer mutually beneficial trades to be made. The idea of a supply curve was shown to exist only as the demand curve of the current owners of the thing that can be traded.

In Part II, I dug further by explaining the importance of getting right the dimensions across which trades are made, and the source of benefits from trade. In housing, we can trade one location for another. We can trade up and down the quality spectrum. We can trade for more or less dwelling space. Across every dimension—of quantity, size, quality, and location, and more—there are trade-offs being made, and that means a supply and demand.

Here, in Part III, I explain the nested “Russian Doll” nature of margins across which trade can occur in each dimension. Yes, there are many trading dimensions, and within each, there are many margins.

What do economists mean by marginal?

In Part I, we showed how trades take place whenever the benefit to a buyer exceeds the benefit given up by a seller. The last potential seller and buyer who can profitably trade are the marginal buyer and seller. They are at the edge. The margin.

In our checkout example, when one queue is 5 people long, and the other is seven long, the seventh person is the marginal buyer of the 6th position in the shorter queue. People further up the queue have no reason to swap.

But it is also true that for the marginal buyer and seller, the last item they trade is the marginal one. They may trade many items with each other for mutual benefit until the last item they trade.

So yes, the trade of a single person from one queue to another is the marginal person, but within that person’s groceries, they have marginal items too.

Economists call this idea the intensive and extensive margins. The extensive margin is the decision whether to swap a queue, and the intensive margin is how many items you buy within your queue position.

What is marginal cost?

Remember from Part II that the price at which a trading equilibrium occurs is where the benefit given up for the last thing sold is just less than the benefit of the buyer for the last thing bought. The price is a measure of that benefit. Or, in the lingo, supply (benefit given up) is close to equal to demand (benefit received).

This is true for the last buyer (extensive margin) and the last item from that buyer (intensive margin).

Here’s where the rabbit goes into the hat in the economic theory that you might have learnt at university, which leads to enormous confusion in general, but especially around what the price of land should be (heard of the “zoning tax”?).

The benefit given up, i.e. the cost of supply, is not the same as the input cost of production. Another way of describing this is that the benefit given up to trade is the next best alternative use of the resources, including waiting to sell the items in the future.

Let me repeat that.

The input cost of production, that is, the total cost you pay for workers, equipment and so forth, is not the benefit given up when you sell.

The benefit given up is the chance to sell that same item later. That is, the price of waiting. Remember, the supply curve is just the demand curve from those who already own a thing that can be traded.

Smuggling in the assumption that the concept of supply (benefit given up) in a trading equilibrium reflects the input cost of production is a huge deal for economic theory and its application in a vast amount of economic analysis.

Here’s why.

The standard economic theory of production and pricing is based on the idea that within each firm, there is an intensive margin of production. Holding fixed the, um, fixed cost (whatever they are), firms can produce more output per period (i.e. faster) or less per period (slower). The change in total costs is thought to be the marginal input cost and hence represents the supply curve of that firm—after all, input costs are assumed to be the supply curve.

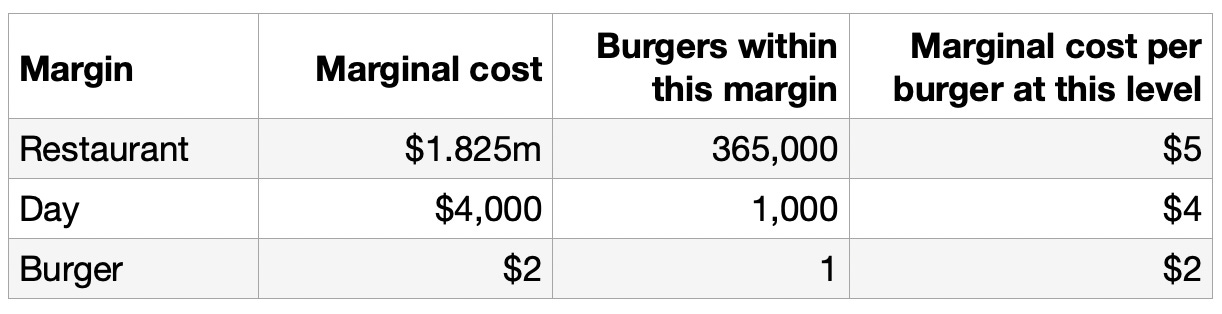

For example, at a single McDonald’s restaurant, there is a marginal cost of an extra burger on a Sunday after selling a thousand burgers that day. The fixed costs of the employees, the store and equipment don’t change when one extra burger is produced. So the marginal cost of that burger is just the cost of the ingredients that would have to be replaced for that last burger.

For a McDonald’s restaurant selling 1,000 burgers per day, the average cost per burger to cover the workers, equipment, building and ingredients might be $5. But once the workers, equipment and building are paid for, the marginal cost of the extra burger after 1,000 have been sold that day might only be $2 in terms of the extra ingredients used.

Now, let me bring together the theory of market trading and equilibrium that I have been explaining here, and the assumption that input costs, and specifically the intensive marginal input costs, are relevant for price setting.

Consider that you walked into a McDonald’s restaurant that Sunday afternoon.

You know that the fixed costs for the staff and equipment for the day have been covered by all the earlier burger sales. The staff know that too. So by the logic of supply and demand, selling a burger at any price above that afternoon’s marginal input cost of the ingredients is a net benefit to the store. If that was the only period of time to ever sell a burger again, then the price could be bargained down to the marginal cost during that period for a single burger.

We see this type of re-pricing happen near closing time in many food stores. For example, take-away food outlets that cook in batches, such as buffets, will reduce prices for afternoon specials. Just the other day, a lovely lady gave me free doughnuts from a store at closing time.

These are short-run patterns that are not the normal way goods are priced. Yes, the doughnuts I was given were already cooked and headed for the bin, so the marginal cost was zero—all costs had been incurred. But that can’t be a sensible way to understand pricing in general, which has to cover all input costs as a bare minimum.

The marginal cost controversy

In the 1940s, a debate erupted in the top economic journals about the problem of pricing at marginal cost. This debate is referred to as the Marginal Cost Controversy (you can download Ronald Coase’s contribution to those debates below).

The problem at the heart of this controversy was simply the problem I have explained using the McDonald’s example. Economic theory at the time held that socially-optimal pricing should reflect the marginal cost of production, not the average cost of production.

What’s the problem?

The marginal input cost is universally below the average input cost. So nothing ever gets produced.

Any business with any economies of scale has some upfront fixed costs which it amortises across its output over time, which means that as you produce more, your average cost falls. A falling average cost means that the cost of the extra final good is lower.

For example, if I have a fixed cost of $3,000 per day to pay for my factory and equipment, and a $2 input cost per burger, then if I sell 1,000 burgers, the average cost is $2 + $3000/1000 = $5 per burger. But if I sell one more, which is the intensive margin over extra burgers, but total cost only rises by $2, which is the marginal input cost of that extra burger.

The old-fashioned economic way of thinking was that if you can produce one more burger for $2, then the socially-optimal price is $2, not $5. So how does the extra $3 per burger get paid for?

Participants in the marginal cost controversy weren’t thinking of burgers. They had in mind large-scale infrastructure projects. Here, the problem gets worse.

If I build a bridge and fund it with a user toll, then the average cost of producing the bridge crossings is the total cost of building the bridge divided by the number of cars that cross. But the marginal cost is zero! Putting 1,000 cars over the bridge each day, or 1,001 cars per day, involved no extra cost.

Marginal cost pricing logic says that bridges should be free, and burgers should only cost what the ingredients cost the restaurant.

This is clearly wrong. Here’s why. For some reason, this critique has never been made of the standard economic view. But it really matters.

Inside every margin is another margin

There is the Russian Doll of margins on the production side of the economy as well as the demand side. Just like we had an intensive margin and an extensive margin of shoppers swapping queues and shoppers buying more items, production has similar margins.

Yes, there is a marginal burger produced on that day. But that DAY is the marginal choice of opening DAY. That RESTAURANT is the marginal choice of opening another RESTAURANT.

At each level (or margin) of production choice, supply and demand apply as these are all possible trades.

If we hold fixed the fact that this restaurant exists, and the choice to be open this day has been made, then that Sunday afternoon, the marginal (extra) input cost for a burger is $2 of ingredients.

If we hold fixed the fact that this restaurant exists, the input cost for opening an extra day to sell 1000 burgers might be $4, comprising $2 of ingredients and $2 of worker pay for that day.

If we hold neither fixed and consider the input cost of opening that marginal restaurant, then that choice might involve a marginal input cost per burger of $5, which includes the $2 for ingredients, $2 for workers, and $1 for building and equipment.

The table below summarises this simple example. The marginal restaurant costs $1.8m to run all in with equipment, workers and ingredients, for the year, but sells 1,000 burgers per day (so 365,000) at a marginal restaurant input cost of $5 per burger. The same logic applies to the marginal opening day and the marginal burger within an open day.

Clearly, the conflict between the input cost at each margin implies that prices are not set by marginal input costs. And that makes sense given our exposition in this Supply and Demand Series. The concept of a supply curve just means the demand for the current owner of an item that can be sold. For McDonald’s restaurant burgers, the current owners demand at least $5 per burger; otherwise, they will wait for the next customer.

Yes, that demand must be higher than input costs. But how much higher can vary according to pricing power and competition environments, and risks involved in that industry.

More examples

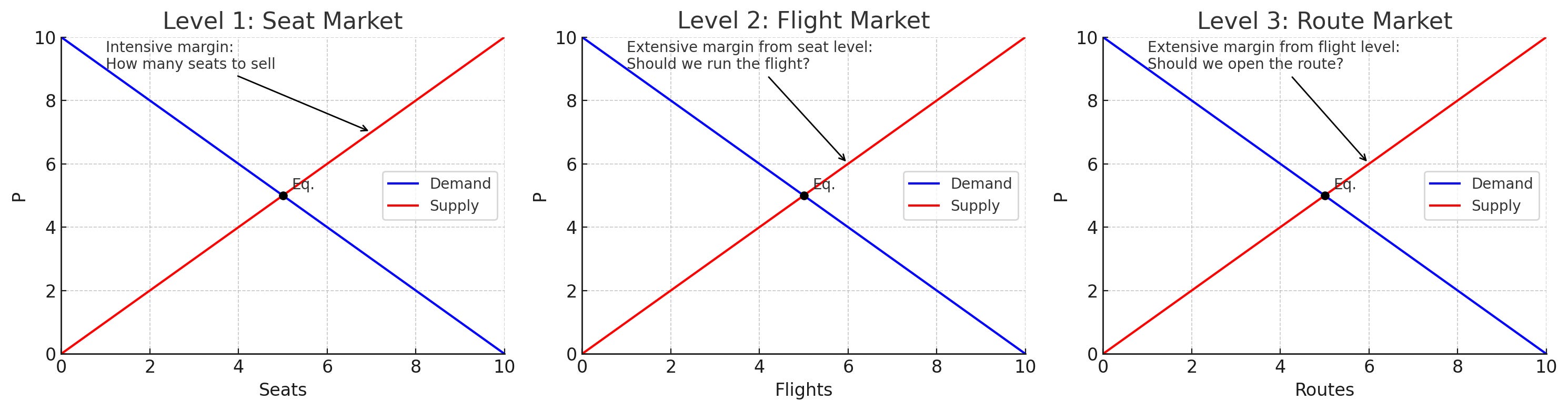

Consider airlines. We know that they sell seats at discounted prices when planes aren’t quite full.

This is the seat margin. Holding fixed the costs of the flight, the marginal input cost of selling a seat is low.

But at the flight margin, holding fixed the costs of operating that route and the airline itself, the marginal input cost of a seat includes the fuel, staff, and airport fees.

At the route margin, the cost of the airline is held fixed, but the cost of perhaps leasing an extra plane to operate is included in the marginal input cost of a seat.

At each of these levels, supply and demand apply. If the benefit of an extra seat sale exceeds the benefit from not selling, we try to sell it. If the benefit of an extra flight exceeds the benefit of not putting on the flight, we put on the flight.

Airlines are also a good example of how prices can vary during abnormal periods. Last-minute deals are often used if the choice of flights ends up not matching the demand for seats. And vice versa, if there is a sudden increase in buyers but no option to put on more flights, then higher prices can be charged. But the usual airline pricing must cover the total cost at every margin.

Here’s a housing example.

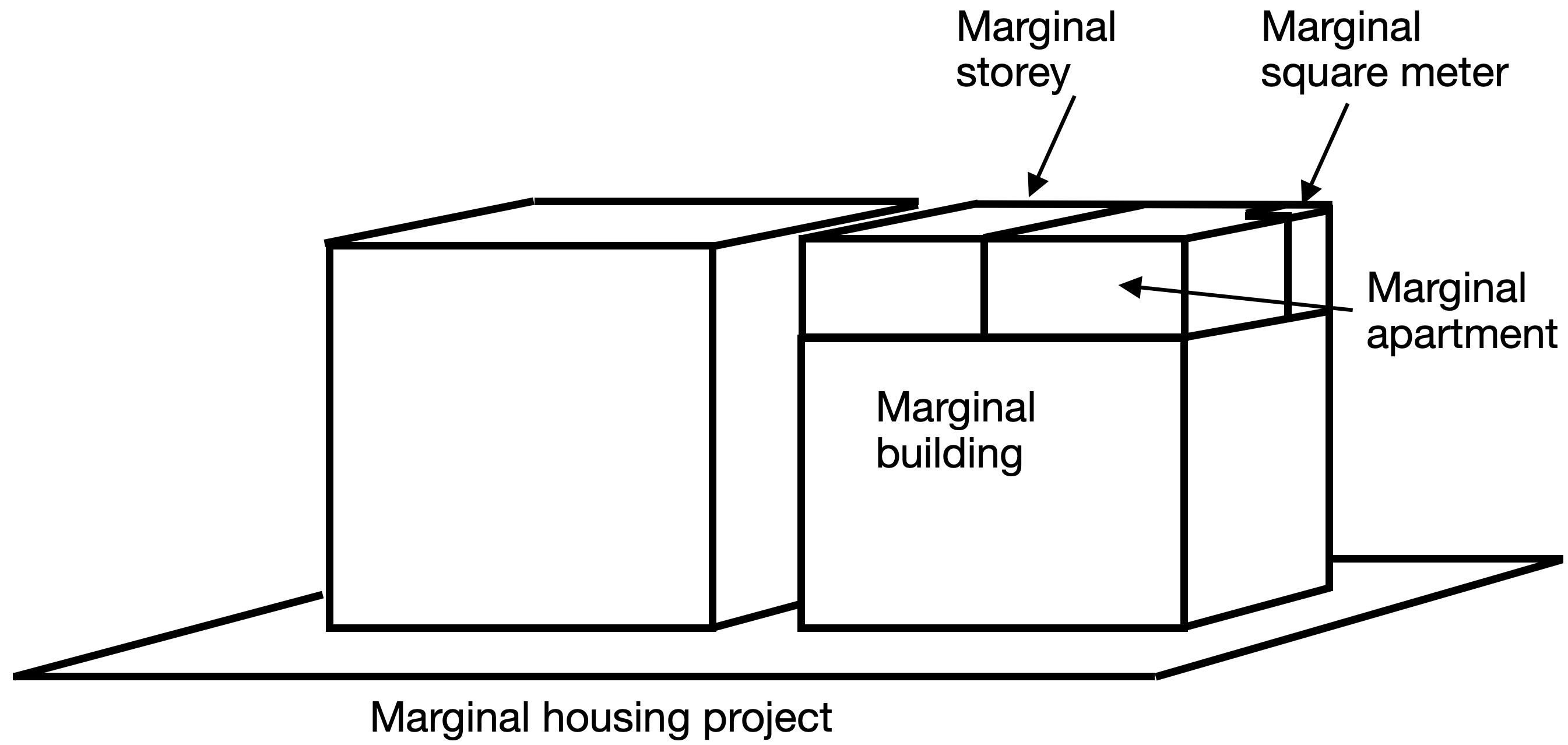

There is an extra dwelling margin per project, an extra building margin, and an extra project margin.

This is the dwelling margin, holding fixed the costs of the building and project, the marginal input cost of constructing a dwelling is low.

But at the building margin, holding fixed the costs of operating that business and the project, the marginal input cost of a dwelling includes the building design and construction overheads.

At the project margin, the cost of the business is held fixed, but the cost of buying the site is now part of the marginal input cost of a dwelling.

The diagram below provides a physical visual.

Yet there is a major strand of economic literature that assumes which margin is the relevant one for setting the price of homes and land, called the “zoning tax” literature (a good summary starts at 17.52 of this video). The assumption that supply is based on some arbitrarily chosen marginal input cost, rather than the full opportunity cost of a seller (i.e. the benefit forgone), is a common error in housing analysis, which you can read about in these two articles:

The beauty of markets is not that they are cheap

A focus on the input cost per unit, ignoring the different dimensions and margins, has led economists to claim that the social benefit of markets is that they produce at the lowest cost in each market (i.e. with prices reflecting the marginal cost of production).

This was the subject of the Marginal Cost Controversy. It must be wrong. Yet it is still the way economics is taught, despite the inconsistencies.

Markets price at the market price.

Yes, there are abnormal brief periods where production and investment choices are miscalculated, and some prices may deviate temporarily downwards to marginal input cost at some specific margin, generating a mutually beneficial trade during that brief period where some costs have been incurred that can’t be reversed (which economists call sunk costs). But this can’t be the norm, or why competition and market production appear to be beneficial compared to attempts to centrally plan at a large scale.

After all, no one will start a business and price at the input cost of any sub-margin.

Not only do economists smuggle in input cost assumptions into supply and demand analysis, but they also smuggle in a short-run assumption that holds higher-level production decisions fixed. But this can only happen for a very short period of time—for an afternoon at a restaurant, or for a single flight. This the not the normal way markets operate when production decisions at each level are made with roughly correct estimates of demand (or where production decisions that get demand wrong result in businesses closing and the market selecting for correct decisions).

The value of markets is not that they produce at a price equal to some marginal cost—it is that they experiment. Market producers can experiment with trade-offs across many dimensions, some of which are not obvious until they are tried, such as new technology or equipment. Through experimentation by producers, markets learn the most valuable ways to do things at each margin and across each dimension that match what buyers value. Yes, we could invest in a bigger factory and decrease the per-unit cost, but that might not be the right investment choice in this market at the higher level of factory investment margin. This experimentation happens in the bundling up of dimensions into products and services, and the choice of customers over which bundles they value most.

Markets can be experimentation machines, searching for new bundles and combinations of dimensions in products that are profitable.

So what?

When economists say the policy effects happen at the margins, they often don’t articulate which margin they mean. Yes, supply and demand simplifications can be quite accurate. For example, when unexpected increases in demand lead to higher prices, or unexpected declines in production due to weather events. Another case is where a tax on trade makes some trades from buyers with the lower benefit and sellers with the highest benefit from being mutually beneficial due to the new tax cost of trading.

But a more detailed analysis needs a much clearer understanding of which margins matter and that pricing can’t, in the normal operation of markets, be set with reference to marginal input costs of production except at the highest level, in which case prices just reflect total costs.

As always, please like, share, comment, and subscribe. Thanks for your support. You can find Fresh Economic Thinking on YouTube, Spotify, and Apple Podcasts.

Interested in learning more? Fresh Economic Thinking runs in-person and online workshops to help your organisation dig into the economic issues you face and learn powerful insights.