Ownership illusions: Private and public businesses

Part 2: Why is the value of business ownership ignored for public owners, while this same value is a prized economic metric for private owners?

Read Part 1 of this four-part series at the link below.

In case you missed it, I have a new working paper out with co-author Tim Helm, entitled Ownership Illusions: When ownership really matters for economic analysis. In the paper, we look at four situations where failure to recognise the structure of ownership leads economic analysis astray.

Today, I want to expand on our second situation.

Part 2: Public and private business ownership

Selling government businesses is commonly thought to generate additional cash revenue for general spending. It is also commonly thought that buying businesses through sovereign wealth funds can generate a risk margin over cash, and thus improve the long-term public budget position via differential returns.

How can selling a business for cash improve the budget position yet the reverse trade of buying a business with cash also have the same effect?

The contradiction is due to another ownership illusion. Governments do not record accurate balance sheets, and the capitalised value of revenue from operations is not generally reported.1 But when a business is held in a sovereign wealth fund or other such financial entity its capitalised market value is regularly estimated, reported, and used as a metric for success.

In this illusion, ownership patterns are irrelevant to the economic reality of asset wealth, but economic analysis may be misled by reliance on reporting metrics that misrepresent this reality due to accounting inconsistencies. Political messaging that portrays cash proceeds from sale as additional revenue misleads to an even greater extent, trading on the public’s confusion about these concepts.

A real-world example and thought experiment can illustrate this point.

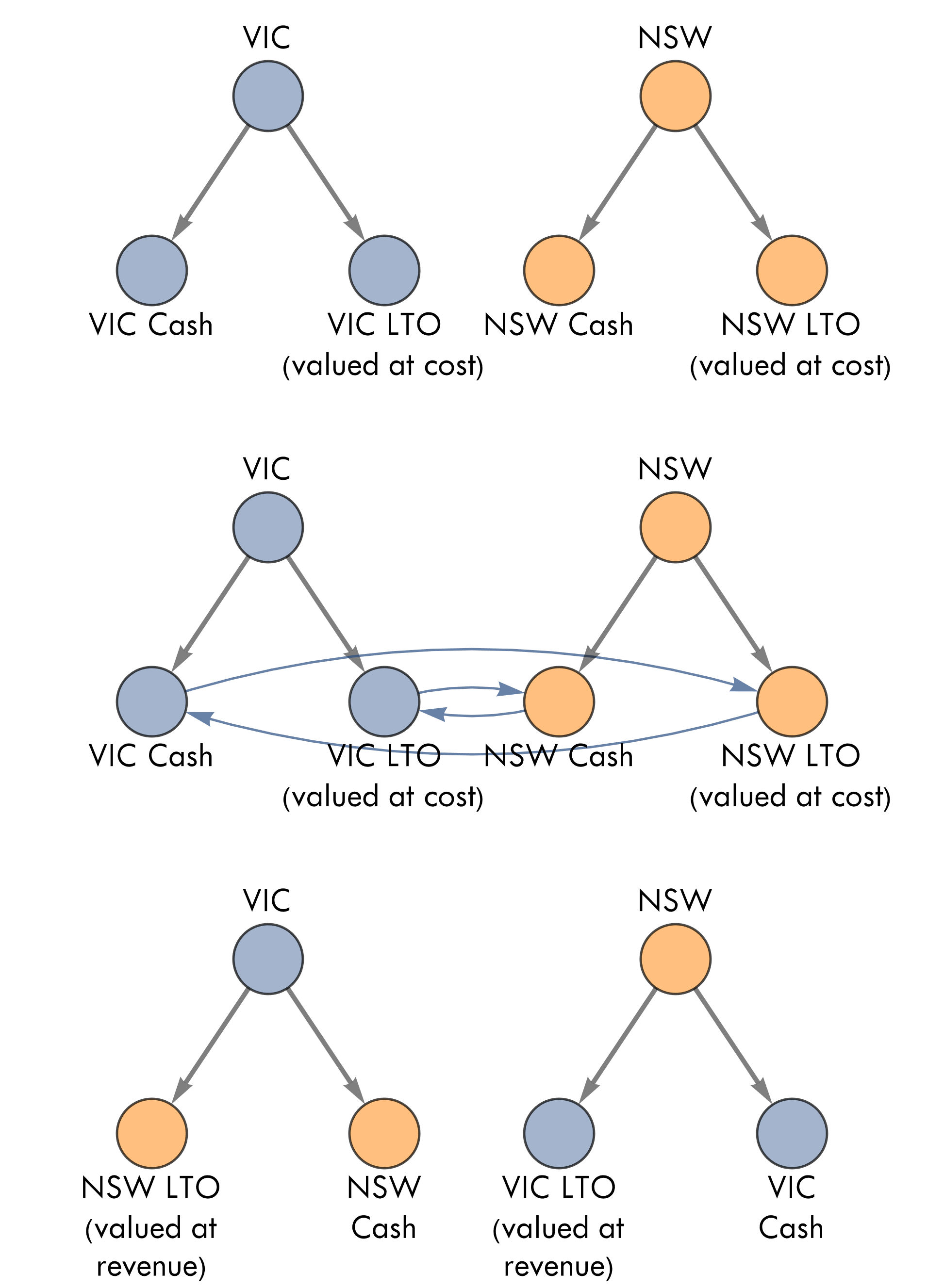

The Australian states of New South Wales and Victoria have in recent years privatised their land titles office (LTO) operations. The LTOs manage the property titles system and charge fees to users to record property sales or access records, generating a cash surplus. These privatisations effectively swapped ownership of a non-cash asset in the form of business equity for ownership of a cash asset, the sale proceeds.

The sales were described by government agencies as unlocking capital for investment with the upfront proceeds “recycled” into funding new infrastructure.

Both states also run investment funds that invest in, amongst other things, company ownership in the form of direct ownership or equity shares.

In principle, each state could have sold their LTO to the investment fund of the other state, as shown in the image below. Prior to this sale, each state would have owned cash and its LTO business (top panel). After the ownership swaps, each state would have owned the cash proceeds and the other’s LTO business (bottom panel). Reported net assets would increase for both, since the LTO revenue stream would be valued more highly when owned as an investment than as a government operation. Despite the ownership swap making no difference to combined revenue or costs, each state would think of itself as better off economically because of an ownership illusion.

Misleading metrics and political messaging aside, much economic commentary on privatisation makes clear that the proceeds from selling public businesses are not a true budgetary gain. In instances such as the LTO sales, these transactions are better understood as “tax farming”, in reference to the historical examples of administratively weak or non-creditworthy governments selling the right to collect tax to private collectors.

Economic gains from privatisation may still be expected in the form of efficiency improvements due to competition and innovation, though often overlooked is that competition can be fostered without changing ownership. Norway’s oil market, for instance, shows that it is possible to have public and private firms compete, and even have public investment funds hold part-shares of private firms in the same market.

These are more valid and economically significant policy objectives, and seeing through the ownership illusion in public versus private business holdings can allow a clearer focus on the question of whether and when privatisation is the best means to achieve them.

Government businesses providing market goods and services, e.g. public financial and non-financial corporations, are typically valued based on the market value of the business, or on capitalisation of operating results. However general government sector operations, such as the collection of regulatory fees and taxes, are only valued for their physical assets such as land and buildings

"Selling government businesses is commonly thought to generate additional cash revenue for general spending." The rationale for privatizing an asset is that it will be managed better in private hands than in government hands, so the sales price will be greater than the discounted cash flow to the government. The most reasonable thing to do with capital income would be to pay down government debt. [I see from the rest of the post that you think the reasonableness of this or something equivalent needs to be argued, so more power to you. :)]

The specific example, however raises a different issue. A provincial title office sounds like a monopoly. Selling a government monopoly to a private investor who may take fuller advantage of monopoly pricing might mean that some of the sales price would not come from greater efficiency of management. The standard neo-liberal economic prescription is to eliminate the monopoly when privatizing and would be feasible for the titling function.