Forget land, labour and capital—BELIEFS are the supreme economic production factor

Beliefs are the first step in any economic activity. How and why do they matter, and how do we sustain the most useful beliefs?

“We are not members of a democracy Father. We are members of an order”

— Father Gabriel, played by Jeremy Irons, in The Mission (1986)

Not long after the above line is spoken in the classic 1986 film The Mission, we see the transformative effects of that order on the indigenous tribes who were contacted by Jesuit missionaries and began adopting their beliefs.

Instead of small thatched huts, we see stone walls and large timber buildings being erected. We see mass coordinated production. A primitive society is transformed into an industrious one. Tribes turn into capital-investing, state-building, trading microsocieties. New beliefs create a new social order.

Many scenes, not just in film, regularly remind me of the economic power of our collectively held beliefs. So much so that I would argue that beliefs are the primary factor of production in any economy.

This leads to many questions.

What beliefs underpin our market-based modern order? What happens when beliefs change? And can we, or should we, try to manipulate economically relevant beliefs?

I won’t answer those questions today. Just ask them, and share some thoughts about how beliefs, maybe even irrational ones, seem economically important and what happens when beliefs suddenly change.

What beliefs underpin our social order?

I’m not the first to identify the power of beliefs.

Yuval Noah Harari’s book Sapiens explains how the ability of humans to believe imaginary things exerts enormous power over our social and economic order.

Unlike lying, an imagined reality is something that everyone believes in, and as long as this communal belief persists, the imagined reality exerts force in the world. The sculptor from the Stadel Cave may sincerely have believed in the existence of the lion-man guardian spirit. Some sorcerers are charlatans, but most sincerely believe in the existence of gods and demons. Most millionaires sincerely believe in the existence of money and limited liability companies. Most human-rights activists sincerely believe in the existence of human rights.

This passage shows how beliefs, politics, religion and economic order all seem to emerge from human hard wiring for social cooperation and underpin all the major institutions of modernity.

To have a nation requires belief in imaginary lines on the earth. To have economic growth requires the belief that growth is possible. To have money, companies, and organisations requires beliefs in things that only exist in our collective minds. Trade and investment run on beliefs about the future and the reliability of trading partners.

The innovation incentive in markets also rests on beliefs.

New businesses start because someone believes something that others don’t. They believe, even if the odds are stacked against them, in what they are doing. Who starts a business they don’t believe in it?

Elon Musk believes we can start a human civilisation on Mars. I think he has now convinced many others. Is that collective belief powerful enough to make it a reality? I think it is quite clear that without his potentially irrational beliefs that space technology would not be where it is today.

Because of their supreme reliance on beliefs, markets might only emerge in a society in a limited number of ways that fit with collective beliefs. Markets in people or markets in organs? If we believe so.

Are any of these beliefs rational?

Hard to say.

If everyone else believes the same thing, then what would be irrational to believe as an individual becomes perfectly rational to believe together. Being the only believer in a scammy cryptocurrency is irrational. But if everyone else believes, then maybe not.

What matters for society and prosperity is which beliefs spread. Individual beliefs are nothing without a tribe of co-believers. If one person believes but no one else does, that belief is fragile. This post by Misha Saul reveals an interesting encounter of strong but conflicting beliefs between an individual and society.1

What beliefs matter for growth?

One place to start understanding which beliefs matter for economic progress and growth is to compare groups of humans with different beliefs in similar situations and see how they became prosperous (or not). I am reminded of a Johnny Harris video about the creation of Utah by the Mormons, whose beliefs seemed to be especially conducive to economic prosperity. Can they be compared to other communities that were different mainly in beliefs?

A problem facing any effort to observe the power of beliefs is that they come bundled together in packages in the minds of individuals and on average across the population—religious packages, economic packages like capitalism and democracy.

It seems nearly impossible, except via trial and error over many generations of societies, to determine which package of beliefs generates economic prosperity.

Since I’ve just admitted to giving up on getting a clear answer, I’ll speculate instead.

Here is a package of beliefs that I suspect would be required for a prosperous and growing society. These are what I would be thinking about as the ruler of a new society emerging from a shipwreck or other fantasy scenario about rebuilding social order.

Economic growth is possible and desirable.

This is just stealing Harari’s main point. We also need to have some conception of what an economy is, what is growing, and why it is good.Governance organisations should foster growth.

If we believe growth is good, then we should believe that any governance structure that emerges has a crucial role in trying to achieve it.Property rights are important and tradeable.

The trading patterns that emerge when property rights exist help societies to reorganise for growth and I suspect that intellectual property also creates strong incentives for experimentation that is hard to create in other ways.Companies and productive organisations can and should exist and be allowed to form, reform, and dissolve.

I think that structures that help people form and reform organisations while limiting individual risk from bankruptcy helps enable risk-taking and experimentation necessary for growth.People and companies should experiment with new a better ways of doing things. This is a subpart of the idea that growth is possible and desirable. I think we also need to believe in the processes that achieve that.

Households should be based around families and be allowed to make decisions independently about their earning and spending decisions.

We need to believe in the distributed decisions of households to participate and production and consumption choices that are best for them.

Are there more? Sure. Let’s hear them. I reckon the belief package is much deeper than we can reasonably fathom on first glance. No doubt there are layers upon layers.

For now, then, let’s look up to a more superficial layer and think about whether some smaller economic patterns can be explained by beliefs or changes in beliefs. Maybe that’s where we start to create an understanding of this hidden but supreme factor of production.

One place to start that seems obvious to me is the pattern of boom and bust cycles. Does the bust begin when we all suddenly stop believing in the boom?

A reasonable story about how beliefs matter is that after a certain period of good times, some people begin to believe that the situation is too good to be true. This belief, while at first not important to market outcomes, begins to cascade as others begin to believe and more people take action based on those beliefs. Believers start selling assets that they see as risky. Those actions confirm the new beliefs, which cascade further, leading to different actions, triggering financial market crashes and recessions.

Economists already think of cycles as waves of optimism and pessimism. So the basic principle of the power of beliefs to determine economic outcomes seems widely accepted. We just don’t know much more.

In fact, beliefs are the key to any repeated game theory problem. Yet too often we impose by assumption in our economic analysis one specific belief called “rationality”.

A cleaner example might be the meme-stock phenomenon, which shows that it can be rational to believe in rising stock prices for no other reason except that others believe. This is classic speculative behaviour. But are macroeconomic cycles also a result of beliefs and speculation?

Another economic pattern where beliefs might be able to be studied is that of catch-up growth of poor nations. Are certain beliefs holding back some nations, while favourable packages of beliefs help others?

What we believe → What we do → What we get

We are normally more comfortable with the language of belief outside of economics. Our clothing and customs are clear areas where belief shines through. Some cultures believe men should have long hair, and some believe men should have short hair. Our religious beliefs might dictate what days of the week or year we work.

But even what appear to be non-economic beliefs have material economic consequences. And when these beliefs change for whatever reason, the consequences for economic progress can be broad.

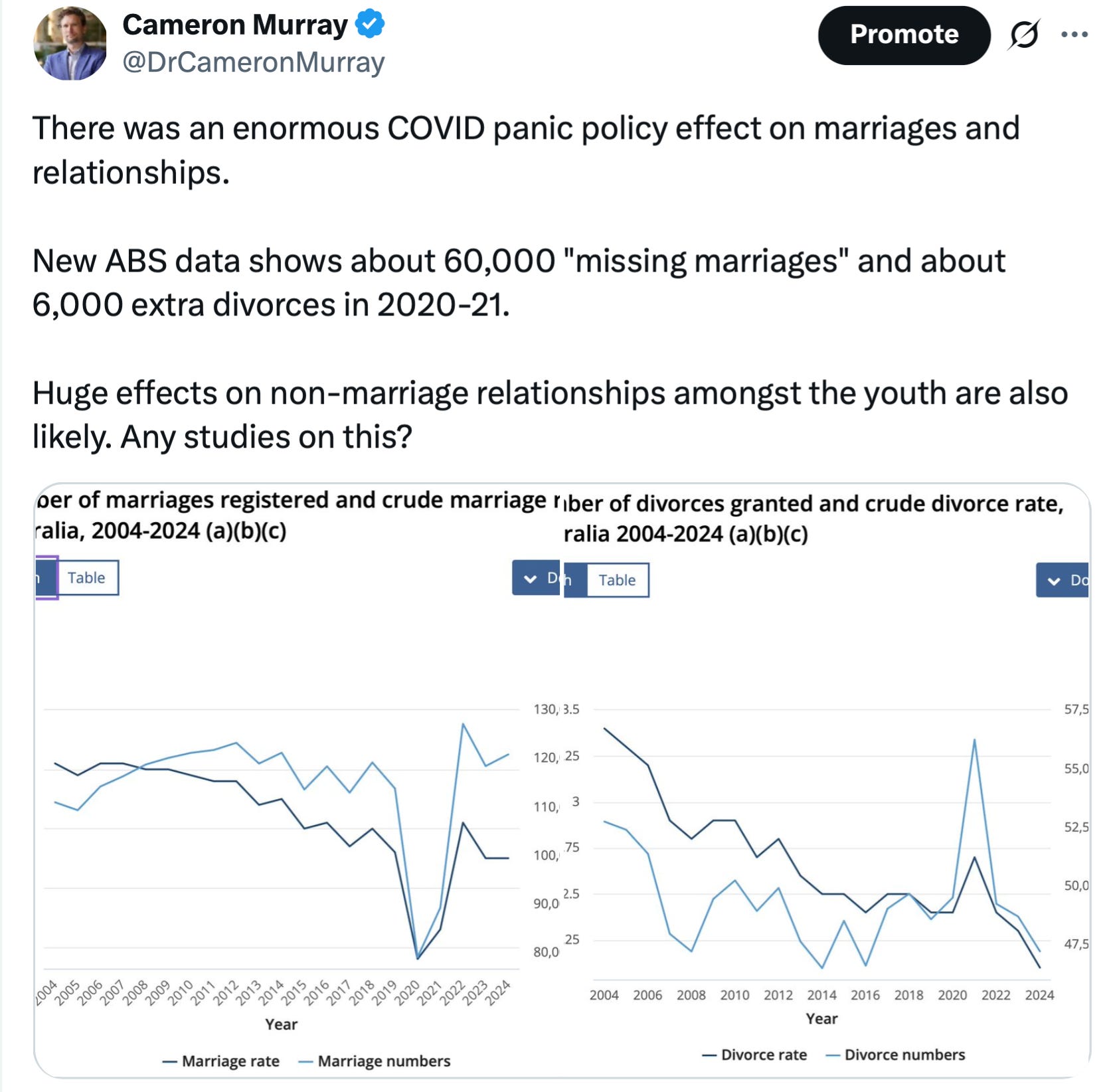

I think the best recent display of how new beliefs radically changed economic outcomes is COVID. The COVID period saw a rapid cascade of new collective beliefs emerge. This changed what we did, which radically changed the reality and economy we got.

For example, one of those realities was the effect on relationships and marriages. Recent Australian data shows that there are roughly 60,000 missing marriages from that period. We created a new collective belief that preventing socialising was more important than finding romance, and got the inevitable result.

That the world could so quickly and radically change its beliefs suggests to me that beliefs are plastic. They can be moulded, sometimes quickly, with some heat, fear and shock. Sometimes slowly with some pressure. Is a shocking change in beliefs needed to turn a peaceful nation into a war machine?

Anyone interested in long, happy, prosperous lives should at some point consider the way we pass down the generations’ beliefs that are effective at promoting prosperity, and inoculate against shocking changes to beliefs that lead to panic or war.

But this is such a tricky problem. We don’t know which beliefs matter, nor if there are even more useful beliefs we have yet to create.

To finish this train-of-thought article, I want to share an article from 2021 that I wrote for Australia’s AFR newspaper. It describes how what we do leads to what we get from the economy.

I called the things we did every day, because of what we believed, a longevity machine, as one of the results of our prior package beliefs and actions was long, happy and productive lives. It didn’t get bogged down on beliefs like I have here. But it was intended to show the power of this new belief in taking away many of the amazing things we once believed in, and thus creating a huge backwards step in terms of our economic progress.

Enjoy. I’d love to hear your comments (and scroll down for a couple of videos you might have missed).

Missing from the debate about the human cost of COVID lockdowns is an understanding of how societies produce health and longevity in the first place.

What are the economic and social ingredients of an historically unprecedented 83-year life expectancy in Australia, and are these at risk from our COVID response?

Over the past decade, Australian life expectancy grew one and a half years. That is 35 million life-years gained for a population of the current size.

The sum of all our economic and social life interactions can be thought of as a longevity machine. It produces economic wealth but it also produces health in the form of longer and happier years of life on average.

Economic and health outcomes are tightly related. A functioning economy pays for hospitals and clean affordable food and the roads and ports to ship food, medicine and other goods. Constructing sewage and energy systems, houses that keep us warm and safe, and schools that educate the next generation, are all parts of a functioning economy.

Sure, the economy is imperfect. Some components of the machine are a net negative for longevity, but the overall system does the job.

Delaying and disrupting the operation of the longevity machine costs lives. A day of delay to the machine in Australia costs 9,600 additional life years by pushing back longevity gains. By this metric, lockdowns reduce expected life-years by far more than might be gained from reducing COVID transmission.

In developing countries like India and Nigeria, where life expectancy is much lower (55 and 70 years respectively) but growing faster, each day of delay to their progress costs 1.4 million life-years. This is an astronomically high human cost that must be accounted for and compared to plausible COVID health scenarios.

This big picture longevity machine view of how social and economic processes create longevity might seem strange to some people. But it is a useful approach when looking at large-scale disruptions from lockdowns because it is surprisingly difficult to break out exactly what elements of social and economic life produce health outcomes. Is it diet? Friendship and social support? Education? Work quality? Family stability? Healthcare services? All have individual and coordinated effects, and all get disrupted by lockdowns in a variety of ways.

We can, however, look at some of the disruptions to different parts of the longevity machine to get a feel for how they cause irreversible reductions to health.

For example, prioritising COVID medical research above other diseases is likely to slow the longevity machine. The delay of other medical diagnoses, treatments and routine vaccinations will generate huge irreversible health costs for years. Due to border closures and supply issues from lockdowns, delays to global childhood vaccination programs are estimated to have already cost over a million lives of children under age five. Converting into life-years remaining at death, this cost alone would constitute more harm to human health than COVID.

We know that average population immunity to other circulating viruses has diminished due to declines in human interaction, creating new outbreaks in children of other deadly viruses such as respiratory syncytial virus (RSV). Global poverty has taken off, as has inequality within countries. Both are factors that reduce longevity.

Mental health is on the decline, binge drinking is up, teenage suicide attempts are up, and demand for counselling services is up. Surveys of well-being show unprecedented falls.

The freedom to travel and take memorable vacations are on the decline, reducing well-being. The kindness that happens in chance human interactions in daily life is down.

Childbearing has been delayed globally, meaning many women will now have fewer children than they desire because of this delay, a blow to their well-being.

Important life events such as high school formals, weddings and funerals, family reunions, birthday celebrations, and milestone sports and cultural events for budding young athletes, musicians and performers are all off the cards, with no chance of catching up for these losses in the future.

Australian governments have been extremely proactive with economic stimulus policies, providing fuel for the longevity machine to recover. But time cannot be recovered. Many lockdown losses, such as those described above, are locked in and will be felt for decades to come.

A public health mantra is that when combatting a single cause of death, one must avoid unintended health costs elsewhere, lest you inadvertently worsen overall health outcomes by your response. This is why pandemic plans prior to 2020 did not support large-scale lockdowns, and indeed, cited risks that behavioural changes might worsen virus propagation as well as health due to other factors.

But these diverse and often hidden health outcomes do not attract much media attention. Thinking about how the sum of social and economic activities as a longevity machine can show just how big a health risk even small disruptions make.

In case you missed it

What economic theory explains why new housing is developed or not? Do we need one if the empirical record is clear?

In this video from a UNSW presentation in early July, Tim Helm and I explain why the theory and empirics are not as clear as most people claim.

Last year I spoke at length with Cahal Moran of Unlearning Economics about The Great Housing Hijack and our muddled housing policy debate, which still continues a year later. It’s as relevant as ever.

As always, please like, share, comment, and subscribe. Thanks for your support. You can find Fresh Economic Thinking on YouTube, Spotify, and Apple Podcasts. Here’s an interview on YouTube you might have missed.

Interested in learning more? Fresh Economic Thinking runs in-person and online workshops to help your organisation dig into the economic issues you face and learn powerful insights.

I often wonder whether in psychology the idea that being diagnoses with a named disorder helps people to change their behaviour because it provides them something to believe on. Rather than trying to go with sheer will power or habit, the naming of an external “god” helps change behaviour.

Are you aware of prof Richard Werner’s work Cameron? He agrees with you, and he proved the mechanism for us to achieve it has been hidden by cartel economics.

Short explanation:https://youtu.be/sClLrobRNXg?si=shIyWD7K6k0s7Iay

Long (better) explanation: https://youtu.be/StTKHskg5Tg?si=tLuh1pEYSXLR4YLS

Interesting article.

(a) If we want new housing, we can always get it, with government investment (as per JM Keynes: do we have the builders the bricks and the blueprints?). It is a political decision, not a financial decision. This spending funds the tax payer, not the other way around, a win-win.

(b) Some of your examples are not beliefs in imaginary things.

"To have money, companies, and organisations requires beliefs in things that only exist in our collective minds. Trade and investment run on beliefs about the future and the reliability of trading partners."

— these are not all imaginary, because humans also set up institutions to organize such affairs, sometimes at the point of proverbial and metaphorical guns (the tax collector). Pretty real stuff, unless you think time in a jail cell or on unemployment row is all in the mind.