Do economists know opportunity cost when they see it?

No. They seem to be unable to answer a first year textbook question more accurately than chance.

Welcome to new subscribers. If you like this, please check out some of my other posts, such as:

Capital vs division of labour: Did Adam Smith learn the wrong lesson from his pin factory tours?

FET podcast episode #5: Why we need a public housing developer

Don’t forget to subscribe and share. Scroll down to read on.

If there is one idea that defines economics, it is opportunity cost. Unfortunately, muddled thinking about this idea means that it is applied quite inconsistently across the economics discipline. Economists can use the word to mean whatever they want it to mean.

In its most basic form, opportunity cost means your next best alternative use of resources. What opportunity did you forgo to undertake this action instead of an alternative? But it gets much more difficult to translate this idea consistently into more detailed economic theories.

I want to highlight two big inconsistencies with the use of opportunity cost in economics. To do that, I want to start with a question that triggered a mini-controversy in the discipline a few years back when it was revealed that economists did worse than chance in answering a multiple-choice textbook question about opportunity cost.

The question was:

You won a free ticket to see an Eric Clapton concert (which has no resale value). Bob Dylan is performing on the same night and is your next‐best alternative activity. Tickets to see Dylan cost $40. On any given day, you would be willing to pay up to $50 to see Dylan. There are no other costs of seeing either performer.

What is the opportunity cost of seeing Eric Clapton? A. 0, B. 10, C. 40, D. 50.

According to the textbooks, the answer is B.

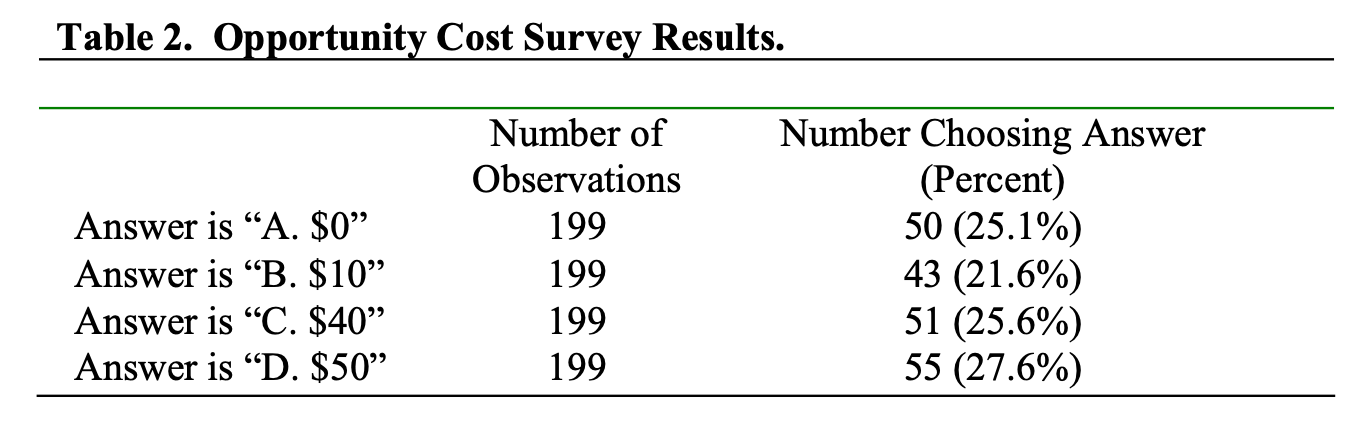

But the economists surveyed at an economics conference had answers that looked like this.

Their answers are similar to choosing randomly. Which is very odd.

There are two mistakes I see here.1

Comparison with different costs

First, the two given alternatives have different resource costs. If you see Dylan you have $40 less to spend. Therefore, a clean comparison of opportunity costs requires us to compare these alternatives

A. See Clapton for free.

B. See Dylan that night and have $40 less to spend.

If we don’t account for the full costs of each alternative, we end up with ridiculous scenarios, like comparing the profit from investing $1m with the profit from investing $1k. It makes no sense when we abstract into raw financial terms, and it makes no sense here either.

Strictly speaking, the correct answer is $10 minus the net benefit from my next best use of $40. But then again, maybe I don't know what opportunity cost is either!

Alternative options are not discrete

Another problem with opportunity cost is that, in reality, there is a continuum of alternatives to any action. The next best option to Alternative A is usually doing Alternative A but cutting some corners slightly. In this case, if seeing the Clapton concert is Alternative A, then seeing Clapton and going to the bathroom when your favourite song is played might be the “next best” alternative.

We could, if we want, break out any of the discrete alternative actions into an infinite array of alternatives. Each of those could be broken out again until we have a continuum.

If we zoom in on this continuum, then the opportunity cost is always equal to the best alternative, and even the opportunity cost of the best alternative is itself.

This point is important. If, for example, we think that supply curves include opportunity costs of resources, then economic profits are always zero or below by definition.

In a topic I study, property markets, this is also important. Many people think that the second-best alternative use of land sets the price. For example, in regard to the price of land for housing:

…in the absence of any restrictions on supply, the price of raw land on the fringes should be tied reasonably closely to its value in alternative uses, such as agriculture.

Why is agriculture the next best alternative to housing? Surely there are multiple residential subdivision options that are alternatives, and some will be better than others.

Property valuers (appraisers) are clear that the value of property rights comes from its highest and best use (because the second best is infinitesimally less valuable than the best). But for some reason, many economists think they know better. Valuers test out the various legal options for land use to determine which one provides the highest value to land, and it is this use that determines its value.

The opportunity cost logic, in this case, becomes more absurd when we think about the case where there are three possible legal uses of land—say agriculture, industrial, and residential (in order of value). If the second-best alternative sets the price, then you can make the land cheaper by regulating against the second-best use of industrial development, making agricultural use the second-best alternative and decreasing land prices for housing.

And I haven't even considered the case when there is only one allowable use of land. Doesn't this make the second-best use to do nothing, therefore bringing the land price to zero?

Like many seemingly insightful economic ideas opportunity cost is less powerful than it appears and often confuses more than it clarifies.

I like these analogies. The one thing I think might not be accounted for is you could end up in a scenario where "price of raw land on the fringes should be tied reasonably closely to its value in alternative uses, such as agriculture" - but not because the price is anchored by the next best use of agriculture.

I think this premise is probably still right, but the principle of opportunity cost to justify it (as you point out) is flawed. Your continuum of alternative uses alludes to this. In reality, we could draw multiple curves series for different land use values starting from an urban centre on the left axis (zero on x-axis) and moving towards the agricultural fringe on the right.

The "highest and best use" for any particular parcel along the x-axis is determined by the land use curve that has the highest land value (y-value) at that particular point.

Because of this, we would eventually expect that as we move further to the right of the x-axis of the continuum, that the agricultural value curve would become the highest y-value and thus the highest and best use. We would expect there to be intercepts between various curves and uses so land value follows a continuum without any breaks.

Thus in principle without zoning regulations we should see a fairly continuous curve and gradually declining highest and best use, which progressively has agriculture as the dominant use. And so the prices/value at the margins should be reasonably close, not because of opportunity cost, but because declining urban use value eventually becomes superseded by agricultural value.

Normally when I see this depicted, agricultural use is usually represented as y = constant (horizontal line), an oversimplification. And urban use is usually represented as a 1/x type function that approaches zero. With agricultural use eventually superseding it as highest and best use.

The question then becomes if the existing jump in land values across (binding) urban growth boundaries are caused by regulation, then how does removal of those restrictions achieve an equilibrium by altering all land use curves?

On the one hand removing the binds on agricultural land would massively boost its value to restore the continuum. On the other, perhaps opening up so many options for residential development would somewhat devalue existing residential use values if rent is determined at the margin as according to Richardo's Law - on this point I cannot be sure yet. It does seem that even with 40 years worth of greenfield land supply available in some instances, residential land prices don't really seem impacted.