Can money TIME TRAVEL to pay for our retirement? Pension bonds reveal the trick that makes many economists believe so

This financial instrument shows there is no flux-capacitor, only economic trickery, at the heart of pre-funded retirement systems

The logic of pre-saving for our collective retirement—whether with superannuation, 401K accounts, or social insurance funds—is that we are transporting money from the present into the future.

But money can’t time travel.

All money can do is be swapped for other things today (or not).

This is extremely important for understanding the potential social value of various national approaches to retirement funding, which unfortunately most economists and major economic institutions get wrong.1

I want to demonstrate how these mandatory saving funds make it look like money is time travelling, when in reality they are shuffling the financial deck of cards without adding to our ability to pay for collective future retirements.

The way to make this clear is with an idea I have mentioned a couple of times before (here and here): Pension Bonds.

I don’t think I have fully and deeply explained how this idea shows that pre-funded accounts have nothing special in them that helps pay for future retirements.

All that is in these funds are claims over future income that we mark up at a price based on the last trade of similar claims. But an age pension is also a claim over future income that could have a price today if it was traded.

Let’s see how that works.

What is an asset?

Anything that creates a legal claim on future economic value is an asset. Collectibles can be assets. Treasury bonds, which are the debts issued by state and federal governments, are assets to their owner. Company shares (stocks) and bonds are assets as they represent a legal claim to the residual incomes of the company.

These assets are all tradeable.

Sometimes assets are not. Your own business might be very difficult to trade, even though your ownership of it represents a claim on the future income of the business. Incorporating a company can help to create a legal entity where part or full ownership of your business can be more easily traded. When it is traded, the value of that legal claim to owning the business will be priced by that trade.

However, some legal claims on future economic value are not tradeable.

My children were born with a legal claim on the future value of a free school education in Australia. We sometimes call legal claims of this type a right.

But rights can also be priced if we change the institutional setup to allow them to be traded.

The conversation about school vouchers shows there is a way to do this. By changing the institutional setup of the right to public school to be one of a right to funding for a school, vouchers create the opportunity to trade (choose to allocate) that right to different schools within the jurisdiction.

It is not much of a leap to imagine that it would also be possible to allow school vouchers to be traded between people—one parent might want to sell their child’s school voucher that year to another parent because they want cash instead, and the buying parent is choosing a school that costs much more than their single voucher provides and is now using two vouchers to pay for that school.

Let’s say that a school voucher provides $10,000 per year to the school the child attends. In this example of the trade to another parent of a single year’s voucher, that would likely happen at a price a touch below $10,000.

You can see how modifying the institutional setup to allow more trades—both choosing which school to spend the voucher on, and which parent owns a voucher—starts to allow more pricing opportunities of what was initially just an abstract right.

We could then take the extra step of bundling up the yearly school vouchers for the twelve years that each child has the right to into a single tradeable financial instrument and allocate that to each child at birth. Call it a School Bond.

Through such an institutional change to create School Bonds, the abstract right to twelve years of schooling is converted into a single tradeable financial asset.

Now, consider the same trade between two families.

One family wants to get the cash while their child is young, so they sell their School Bond to another family. That bond entitles the bearer to twelve years of funding at $10,000 per year. So that trade will happen at a price somewhere near $120,000, depending on discounting and potential increases in the nominal amount of the right over time.

Notice what has happened here?

We have created new assets worth $120,000 for every child years before they need to claim their right. We have brought forward in time the value of a future liability to others (the right to schooling) and priced it today for the beneficiary of the right.

If there are 100,000 children born each year in a jurisdiction, then $12 billion of new School Bond assets are created each year!

Across society, we now have billions in new School Bond assets. We are rich!2 Put those School Bonds in pre-funded accounts and voila, school pays for itself!

Of course, money didn’t time travel, did it? The only thing that changed is that a legal claim to future value has become priced today, when previously the value of that legal claim to its beneficiary remained unpriced and ignored.

Pension bonds

I hope by now you are with me that all assets are just legal claims on future economic value. Only some such claims are tradeable at an upfront price that represents their streams of future benefits. Other legal claims on future value go unpriced and hence are ignored in most economic analyses.

Now think about retirement.

But this time, let’s take the same assets that are in retirement funds today, and prohibit their trade. Your BHP shares in your superannuation fund are yours forever and there is nothing you can do to change that.

Without the ability to trade, there would be no market value for these legal claims. These assets would be like other untraded rights to future economic value.

This is the flip side to the idea that we can also make untradeable rights tradeable and in doing so, establish a market price today for those future streams of economic value.

The age pension is a future stream of value to each Australian. Yet we cannot trade our right to the age pension away to someone who might be willing to pay quite a lot of it.

But if we take the School Bond idea of granting a right at birth in the form of a bond, and then apply it to the right to an age pension, we can see that future age pensions have an enormous value today to beneficiaries.

Currently, Australia’s age pension is about $29,000 per year for a single. The typical pensioner will get that economic value each year for about 15 years.

If I wanted to sell my Pension Bond that I was granted at birth, I could sell it to someone aged 67 who didn’t have the age pension but wanted it. That market price, after some guesstimates of escalation and discounting, might be about $400,000 as a lump sum for that tradable Pension Bond.

To be clear, the age pension is financially equivalent to a bond with a $29,000 coupon paid annually, with the term length tied to the risk of death of the owner of the bond.

So here’s the crazy part about the economic debate over pre-funded and unfunded retirement systems.

Unfunded retirement systems are just as funded as pre-funded ones, but the value today of those future rights is unpriced and hence ignored!

We are being tricked by the ritual of capitalisation, whereby only some types of legal rights are traded and their future value is priced today.

The ritual of pre-funded retirement systems

Let’s say that there is a psychological reason that people want to see large numbers in accounts today to be assured that future age pensions are indeed “funded”. What would we do?

The Treasury should issue to each Australian at birth or upon citizenship a Pension Bond, that grants them the right to the age pension.

But we don’t actually want people trading away their pensions. So instead, we can establish a market price for the Treasury by selling a dozen of these Pension Bonds each year to international buyers, or Australian residents who do not qualify for the pension.

These few sales each year would establish a market price for all the Pension Bonds for every citizen. For now, let’s say that these sales happen at a price of $400,000 for each Pension Bond.

Now, the Treasury can mark up its account with 20 million or so Pension Bonds that it holds for each Australian aged under 67 by that market price. That gives us $8 trillion of Pension Bonds ($400,000 x 20,000,000 = $8,000,000,000,000).

The total value of new Pension Bond assets would be about double the value of other legal claims to future income held in Australia’s private superannuation retirement account, which is currently $4 trillion.

We have used financial tricks to make the value of the age pension time travel into an account today to be better “funded” than the superannuation system.

All it took was a financial trick and selling a dozen Pension Bonds every so often, which costs us nothing— the Treasury gets the equivalent cash value from the foreigners who buy these newly created pension bonds!

Are you crazy?

No.

If this sounds like magic, then you haven’t fully grasped the magic behind every asset. Those Treasury bonds your superannuation account owns are nothing more than the promise of future economic value from the same Treasury that can issue Pension Bonds.

The beauty of this financial trick is that as the country gets wealthier and the real value of future pensions grows, so does the value today of the Pension Bonds. The magic of compounding keeps increasing the value of the Pension Bonds on the Treasury balance sheet.

The real trick is this.

If the Treasury sells Pension Bonds, then it should probably mark up the liability side of its balance sheet too, just as it does for other Treasury bonds. Sure, it holds $8 trillion of pension bonds on our behalf, but it also has the $8 trillion liability to pay those pensions.

There was no extra value created.

What tricks up so many is that for other assets that we use to “fund” retirement, like company shares or property, we simply ignore the future liability that they impose on the rest of us. We calculate the value today to the beneficiary of the future flow of income (the asset owner/rights holder), but we ignore that the future flow of income comes from others in the economy in the future.

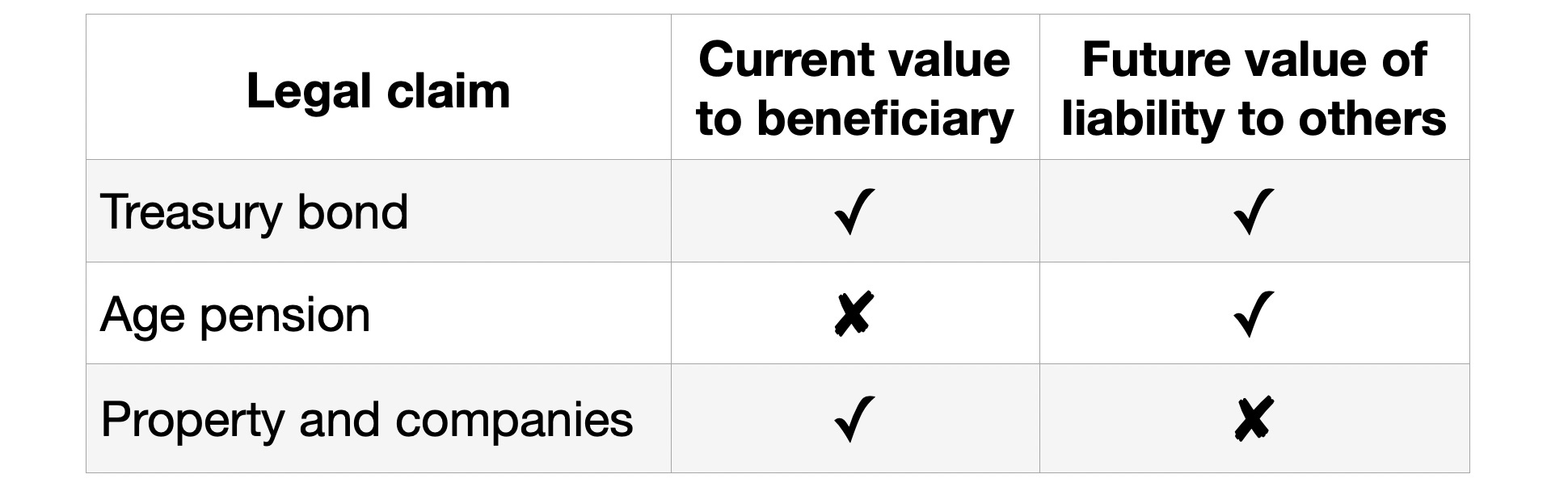

I show the asymmetry in our approach in the below table. Uniquely, we count the private value of Treasury Bonds to bond-holders today, but also their value as a future public liability. But age pensions are only counted as future liabilities, not current assets to their beneficiaries, which they could be with Pension Bonds.

On the other hand, we value the gains to beneficiaries of company shares and property assets today, but ignore that this private value comes from a future liability to the rest of us (a liability to pay prices reflecting excess profits and future rents to occupy land).

The crazy thing is not that Pension Bonds are possible and sensible. The crazy thing is thinking that because some legal claims to future value are priced today they allow some kind of monetary time travel to fund our future.

Though sometimes they get it right. This World Bank article doesn’t think funding solves ageing but focuses on longer work lives.

At the extreme, citizenship contains a lot of similar rights. It is therefore an asset. But weirdly, we do not sell citizenship, though you can imagine that if it was allowed, passport trading exchanges would quickly establish a market price for the implicit rights of the citizens of each country.

Many pension and sovereign wealth funds rely on capital gains to meet future obligations, but these gains can be illusory. Capital gains on assets such as real estate or equities do not always reflect underlying economic productivity or the ability of those assets to generate real value or cash flow in the future. This creates a mirage where asset values are inflated, often disconnected from the broader economy’s ability to support those values sustainably.

Working in Emerging Markets gave me a front-row seat to many instances of egregious abuse of the idea of "funded" pension systems. You can see an excellent example of one of this systems heading toward implosion right now in El Salvador.

These systems are less hhonest than a pure pension bond, but work similarly. Workers "contribute" to "savings", but the managers of the "savings" accounts put nearly all the contributions into government bonds.

Problem number one is that this loosens the budget constraint. The "contributions" will be used to buy bonds even when investors who monitor the credit would have long ago cut the country off. Of course, had the country kept a pure PAYGO system, the debt would still be there, hidden, but it is easier to enact parametric reform of a pension system than to default on a bond. And the fact that "pension fund managers" continue to buy debt, robotically, creates the illusion of a functional bond market and defangs the bond market that would nnormally impose some degree of fiscal discipline.

Problem number two is that these "funds" *always* get looted. Look at how Chile did three or four rounds of "early withdrawal." Argentina looted its funds early in the Kirchner administration. So now you have all these bonds dumped into the market, and account holders spent today the pv they received for the bonds. End result is that you have all the downsides of a crystallized pension debt (as opposed to implicit debt), but it is now owed to the market instead of future pensioners, and the fisc will surely have to take some care of these pensioners anyhow.

I recall many years ago meeting with one of the designers of IceIands pension system. The pension fund managers were barred from investing more than a fraction of contributions in any Icelandic domestic asset. The regulator knew that for a small country the only real savings consisted of foreign assets. The existence of a huge positive in the International Investment Position was key in Icelands efforts to unwind the giant imbalances the private banks ran up before 2008.