Are Australian supermarkets the "bad boys" of the economy?

Or are they just competing the only way they can?

Please consider supporting Fresh Economic Thinking — Australia’s newest one-man think-tank—by upgrading to a paid subscription.

Thank you to all my existing paid FET subscribers. You will get the audiobook of The Great Housing Hijack starting later this month via the FET podcast.

Your support helps me do things like a recent debate with Kevin Erdmann about “What makes housing more affordable? Public Investment vs. Market Liberalization”. You can watch it here.

Right now there is a Senate Inquiry into supermarket prices as well as a much more extensive and detailed inquiry by the Australian Competition and Consumer Commission (ACCC).

Supermarkets aren’t my highest priority in terms of the cost to consumers from their conduct (superannuation is far more costly - see here and here). But supermarkets nevertheless comprise a large share of household budgets and directly affect choices in our daily lives.

One dimension of supermarket competition revolves around location choices. Rules around these choices usually involve town planning regulations that seek to cluster retail activities in a hierarchy of locations.1

This article is about how town planning rules are used as the basis for often frivolous anti-competitive legal cases, with some detail on a recent case in Brisbane.

But the bigger puzzle is this: Why have supermarkets for so long behaved so anti-competitively compared to other retailers or commercial and industrial businesses?

It might simply be the case that when there are few ways to innovate your product, you innovate on other regulatory margins to outcompete your rivals (see last week’s FET #29 podcast about the electricity pseudo-market).

What else is a supermarket to do to make more money?

A history of taming supermarket behaviour

Look at what has already come out of the initial testimony to the current Senate Inquiry on the topic of preventing competition through location choices.

The questions being put to Metcash CEO Grant Ramage during his session were mostly about land banking by Coles and Woolworths.

In the context of the supermarkets, land banking is a strategy where they buy up large areas of land across the country even if they don't have plans (or permission) to build a store there, therefore reducing competition.

Mr Ramage was asked about this behaviour by Coles and Woolworths throughout his appearance before the committee, and he agrees that they are engaging in land banking.

Senator Ross Cadell gave an example about land banking in the Hunter Valley in NSW, and Mr Ramage agreed that it was an example, where supermarkets can buy a proxy through a developer, gain the centre, and remove the independence.

Senator Dean Smith followed up with more questions about land banking by the supermarket giants, and Mr Ramage responded that he didn't think it was "overt or obvious".

"It happens under the radar, there is no obligation for the majors to divulge when they acquire property, it's not illegal," Mr Ramage says, adding they notify the ACCC and councils when they see it happening.

But this is not the first time that supermarkets have been in the firing line for their anti-competitive conduct. It seems to be the nature of this industry. Brisbane-based property analyst Ross Elliot notes that a senior Westfield executive told him in the 1990s that “we would object to a competitor moving a plant pot if we thought it was in our interests to do so.”

In that 1990s era, we were equally concerned about such behaviour. Here’s a 1999 review of retail trade practices by supermarkets. It took the view that although there was a lot of consolidation in the sector, there were benefits from economies of scale to consumers. What is interesting to note from a quarter of a century in the future is that the market share of Coles and Woolworths hasn’t changed as much as you would think, up from around 55% to 65% (depending on how you count). But there is now no Franklins supermarket chain and we have ALDI doing more than a third of the revenue of Coles today.

There was then a 2002 Grocery Inquiry dealing with the behaviour of supermarkets in their contractual arrangements with suppliers.

Strangely, in 2003 there was a headline about the Trolley Wars. People were upset that Woolworths and Aldi were outcompeting other grocery stores. This demonstrates that we don’t know what we mean by competition. One company comes and outcompetes another and that is uncompetitive. You can’t have competition without winners and losers!

In that same year, the ACCC took action because of Woolworth's conduct around preventing liquor licences from potential competitors.

In 2004, Westfield’s Frank Lowy tried to stop a supermarket on Brisbane Airport land near his Westfield Toombul shopping centre, as well as challenging a new shopping centre in Homebush in Sydney. This is a good line from that article:

The executive director of the Shopping Centre Council of Australia, Milton Cockburn, disputes the allegations of anti-competitive tactics (Westfield is a prominent member of the council). "Lodging legal action is not anti-competitive. What law says you can't defend the interests of your investors and retailers?" Perhaps Cockburn should have a look at the National Competition Council's report on planning and construction laws, which begins: "The major competition restriction in planning legislation is its potential to restrict the entry of new competitors into a market. This may result from ... manipulation of the process by commercial objectors to create delays in decision-making and significant additional costs for potential market entrants."

In 2005 the ACCC intervened to stop attempts by Coles and Woolworths leveraging their power to influence the sales of independent grocery stores.

Then in 2008, the ACCC conducted an inquiry into the competitiveness of grocery retailers, out of which came an undertaking with Coles and Woolworths to phase out restrictive leases that prevented other supermarkets from leasing within the same shopping centre.

During its Grocery Inquiry in 2008, the ACCC identified a practice where supermarket operators would include tenancy terms which may have prevented shopping centre managers leasing space to any competing supermarkets. This had the potential to impose restrictions on the number of supermarket outlets in centres and consequently fewer options for consumers.

"Over 700 supermarket leases were identified through the ACCC investigation as potentially restrictive, and this agreement addresses all those existing leases involving Coles and Woolworths, as well as dealing with all future arrangements. I welcome the cooperation of Coles and Woolworths in the development of this arrangement."

The agreement is in the form of a court enforceable undertaking that has been voluntarily provided by Coles and Woolworths.

More interesting for me is this 2010 report by SGS Economics for the Commonwealth Treasury about the planning system as a barrier to entry for supermarkets, and its comments that competition dimensions should not be a factor in planning decisions.

Yet courts were still busy with supermarkets trying to delay competition using planning appeals with frivolous legal cases even in 2012, as reported here.

Retail analysts say the result is that councils are lumbered with massive legal bills and shoppers face less choice and higher prices. More than 20 appeals against shopping centre and retail plans have been lodged in the Planning and Environment court in the past two years.

A 2009 voluntary undertaking by the supermarkets to remove restrictive lease clauses was a positive move for competition. Still, supermarkets were getting similarly effective outcomes with covenants on property when shopping centres were first developed. Here’s how that works:

"There are a large amount of centres where we are restricted from entering because of covenants," said Aldi's managing director for Victoria, Tom Daunt.

"It can be an outright restriction on the use of land by a previous owner who might be a developer for a major supermarket. The other case is clauses in leases of major supermarkets which effectively restrict competitors with quite dramatic rent reductions (if a rival becomes a tenant in the same centre).

"Covenants on available land and clauses in leases, they are all similar. They are all restrictions of trade."

It’s honestly quite something to see the frequency of these inquiries. I suspect this behaviour is economically motived in the same way that confusopolies emerge in undifferentiated industries like telephone, electricity, insurance, etc. Because there are no technology margins to innovate, you push hard on regulatory margins instead.

Of course, outside of the big two supermarkets, Aldi plays its own game, copying the colours and styles of food brands. The supermarkets have been upset about this.

He pointed to similarities between some of Aldi’s exclusive brands and national brands such as Bundaberg ginger beer, Procter & Gamble’s Pantene shampoo, General Mills’s Old El Paso taco kits and Kellogg’s Special K.

To wrap up this whirlwind history, supermarkets use their buying power to influence the actions of both suppliers and shopping centre owners to prevent competition.

Fine.

But there are also some puzzles.

Supermarkets defend their suppliers when it comes to protecting food brands from imitation. But then they also apparently squeeze these suppliers too. How do we reconcile this?

Shopping centre owners interfere with new supermarket locations on behalf of supermarkets. But I think this makes more sense because new venues compete with all tenancies and it is common to have turnover-based leases where landlords share in the turnover gains of tenants.

Also puzzling is that despite decades of concern about supermarket conduct, and what appear to be fairly aggressive tactics, grocery margins aren’t super high and the composition of players in the grocery market has changed quite a bit. There seem to be concerns when supermarkets are very competitive, squeezing down prices from suppliers, and also when they are anti-competitive.

I think a lot of the games we are playing here could benefit from clearer economic thinking on what competition really looks like.

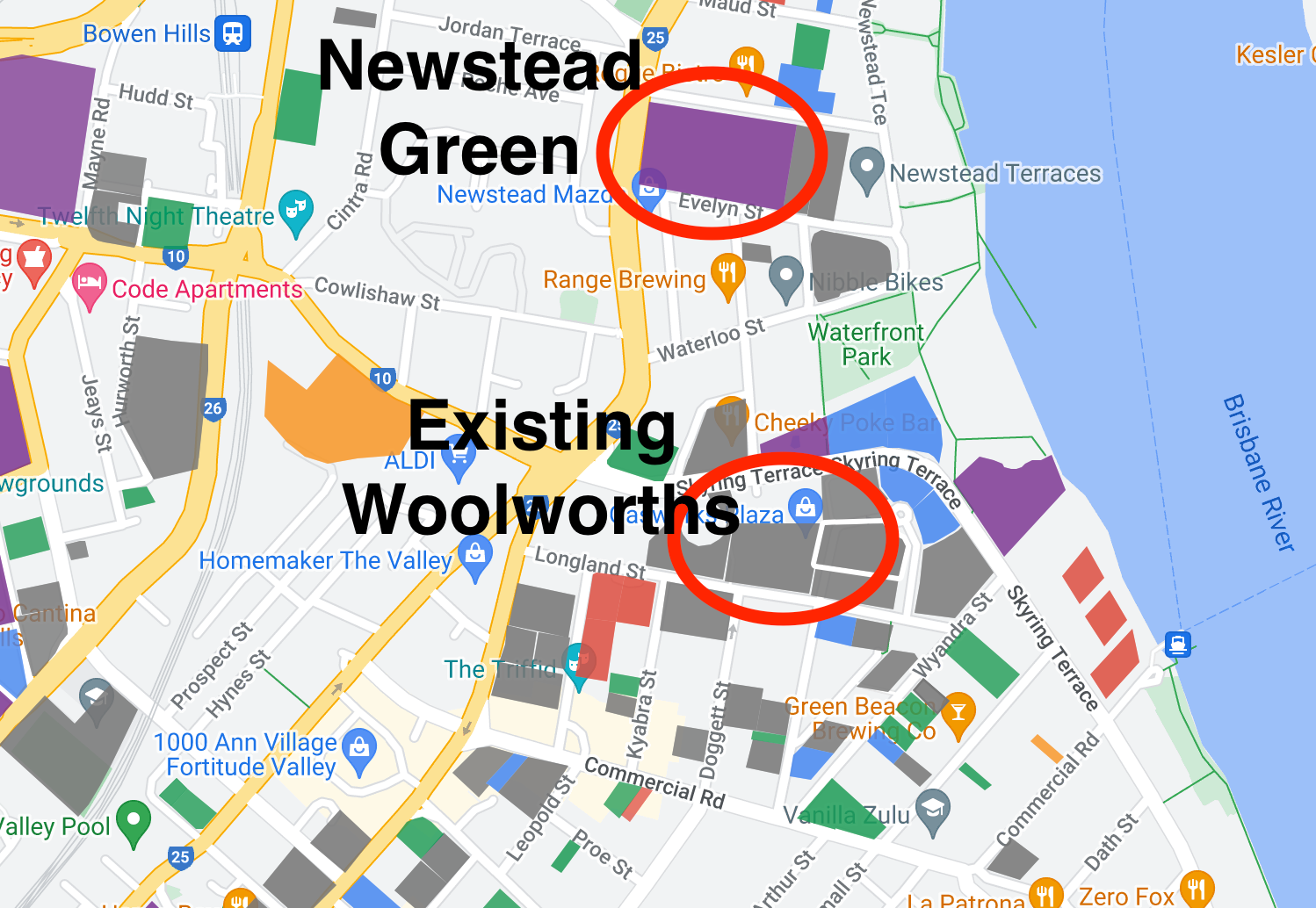

The point I want to make today is to look at a recent case I’m aware of in Brisbane where the landlord of Woolworth’s at Newstead, is challenging a planning approval for a nearby shopping centre.

A Brisbane case of supermarket conduct

A new trend in Brisbane is the mixed-use retail, residential and commercial precinct. One of the more successful, and still yet-to-be-completed projects of this type is in my neighbourhood called West Village, a cluster of eight towers (seven residential and one commercial) above a retail precinct with medical facilities and other uses.

The model seems to work commercially and with many large sites with existing low-density retail and industrial uses in Brisbane suburbs, there are now planning strategies and rules that accommodate this type (such as the Suburban Industrial Strategy etc).

Another example of this type of project is called Buranda Village, on the site of a dated single-storey shopping centre, which is approved for seven towers (four being residential with around 700 apartments) over a 10,000 sqm retail centre.

The flood-ravaged and now under demolition Toombul shopping centre is likely to get a similar treatment when redeveloped.

But the project I want to talk about today is called Newstead Green, on the site of a car yard in the booming inner-city suburb of Newstead. It is approved for nearly 800 apartments, a major retail, commercial, showroom and lifestyle centre, the owner of the existing nearby shopping centre with Woolworths as the anchor tenant (AMP Capital, now owned by Dexus) is appealing the decision.

You can see the locations of the two sites below.

Notice also that on this map the purple, blue, and green shading are all new towers that have been proposed, and the grey are recently completed towers. This area is seriously developing. Thousands of apartments are already approved (including in this project). This seems enough local population to support an extra full-sized supermarket, which normally needs a catchment of about 5,000 people.

To be clear, the Brisbane City Council is now defending its planning decision to approve the project. The grounds of the appeal are of course many, but this part jumps out (pages 8-9).

i. The economic impact of the proposed development upon Gasworks Plaza will be significant due to the scale of the proposed retail component, its proximity to Gasworks Plaza and the extent of the proposed development’s trade area.

ii. The retail component of the proposed development seeks to replicate Gasworks Plaza which, given its close proximity to the proposed development, will provide no community benefit in terms of convenience or choice.

iii. These impacts will seriously erode the viability and vitality of the retail tenancies at Gasworks Plaza, thereby compromising the function of Gasworks Plaza.

iv. Centres provide a focus for public and private investment and community activity. Considerable investment has been made to provide infrastructure, buildings and businesses both within Gasworks Plaza and the adjoining area. This creates a vitality which is central to its function. By diluting economic activity to another location, direct economic impacts will be significant and the benefits intended by City Plan will be eroded to the detriment of the public interest.

v. The impact of the proposed development on Gasworks Plaza would exceed 15% of sales.

The last point gets to the heart of it.

I doubt there will be a 15% effect from today, especially considering the growth of the neighbourhood that will go along with a project of this scale. They are literally saying that the new centre will compete for customers and that they don’t like it.

Since we know that competition is not a valid argument in planning, this probably won’t fly — it will just cost time, money and the resources of the courts.

But now to the original question of supermarket bad boys.

If there was no supermarket here, but still plenty of retail space, the owner of a nearby shopping centre is unlikely to engage in this type of anti-competitive legal strategy.

If it was a new commercial building, owners of nearby buildings wouldn’t take these anti-competitive actions. If it was a new industrial project, again, the same.

Only supermarkets seem to be this actively engaged in anti-competitive behaviour in all domains, especially around real estate, lease conditions (stamped out by the ACCC), planning and zoning, contract conditions with suppliers, and other regulations.

Why?

Maybe it happens in the shadows more so in other sectors. But does it? Or are supermarkets just the bad boy because they have no other innovation to offer to increase their profits?

I have repeatedly stressed that town planning is not the reason for high house prices. Of course, I don’t think it is the cause of the price of groceries either.

"grocery margins aren’t super high"

I can't remember the source, but I recall from several months back that Woolworths' Metro stores have a gross margin of > 7%. (I think this was Banducci on 'Four Corners')

In the USA, Walmart, the largest retailer on Earth [including groceries] has a gross margin of 4.0%

Quite a variance.