Things I've been up to lately

Links to podcasts, writing, news, barneys, and some interesting charts

Podcasts

I had a lovely interview with Catherine Cashmore recently about housing, property, tax, Georgism, and more, on her excellent Cashmore's Real Estate podcast.

A long chat with Unlearning Economics about housing economics, corruption, rent-control, pluralism in the economic discipline and education.

Writing

I wrote this opinion piece for the Syndey Morning Herald about how I went from a super fan to super’s biggest critic. In Australia, our compulsory retirement savings system is called superannuation.

Here is a more detailed report about the design problems with compulsory savings schemes as a retirement policy. I hope it is clear if you read it why I think they cannot be resolved, and why the fairest and most productive solution is to unwind the system altogether and give people their money back to spend as they please.

Here is a new working paper that presents metrics that help show how important the absorption rate is to how many new homes get built. I will write more about this in the future.

Earlier this year I wrote a report for Shelter NSW about funding public housing. The basic idea is that we have tied the hands of public housing agencies with limits to the

News

The result of a long interview about super-for-housing and major issues with the super system generally is this piece by Daniel Teng at Epoch Times.

I was featured in this piece that asks why the over-55s and retirees are so well-catered for in the property markets, but first home buyers are not. Why are there so many retirement villages but no first-home-buyer villages?

Barneys

“Chiefly Australian slang. To argue, to quarrel. A fight or disagreement.”

The stock and trade of my business are ideas. This means I end up in debates about niche methods, data and theories.

One of the big ones I’ve had for years now is about a method used to calculate the “zoning tax”—that is, how much higher property prices might be because of planning regulations.

My view is that the method shows no such thing. But many still want to believe.

A new substack post by Bryan Caplan is a good attempt to understand the method in more detail. He concedes that the method does capture physical attributes that have nothing to do with zoning.

But I think like most supporters of the method, he doesn’t quite yet grasp how crucial to the result is the assumed counterfactual, and how implausible that assumption is. The method assumes, with no justification, that the “free-market” outcome is that all property is priced the same on a per-square-metre basis regardless of the size or shape of the lot (and that all housing lots are the same size).

The question is therefore about what pricing in a property “free-market” looks like. To me, that leads to the question of why property titles in a “free-market” have a positive value at all? I consider this question here.

I have responded here to the key disagreements.

Charts

Lastly, here are a few key charts that I’ve created for various projects I’m working on at the moment that might be of value to those interested in planning and housing markets.

The first deals with the zoning tax barney. Below are the lot size and price combinations for a major subdivision in Queensland. The private property owner here is free to choose the lot sizes and prices in the project. The interesting thing is that they a) choose a variety of lot sizes and b) price them at lower prices per square metre as lot size increases. The free-market outcome here has a big zoning tax. This is consistent with my results of finding the same in a) simulated data, b) 1850s colonial Australia property records, and c) archeological records of property transactions in ancient Mesopotamia.

In Auckland, approvals and prices seem to track together. One of the puzzles of the arguments around planning and housing is why the market always seems to be able to double, triple, or quadruple the rate of approvals when it wants. Perhaps the market has its own built-in speed limit?

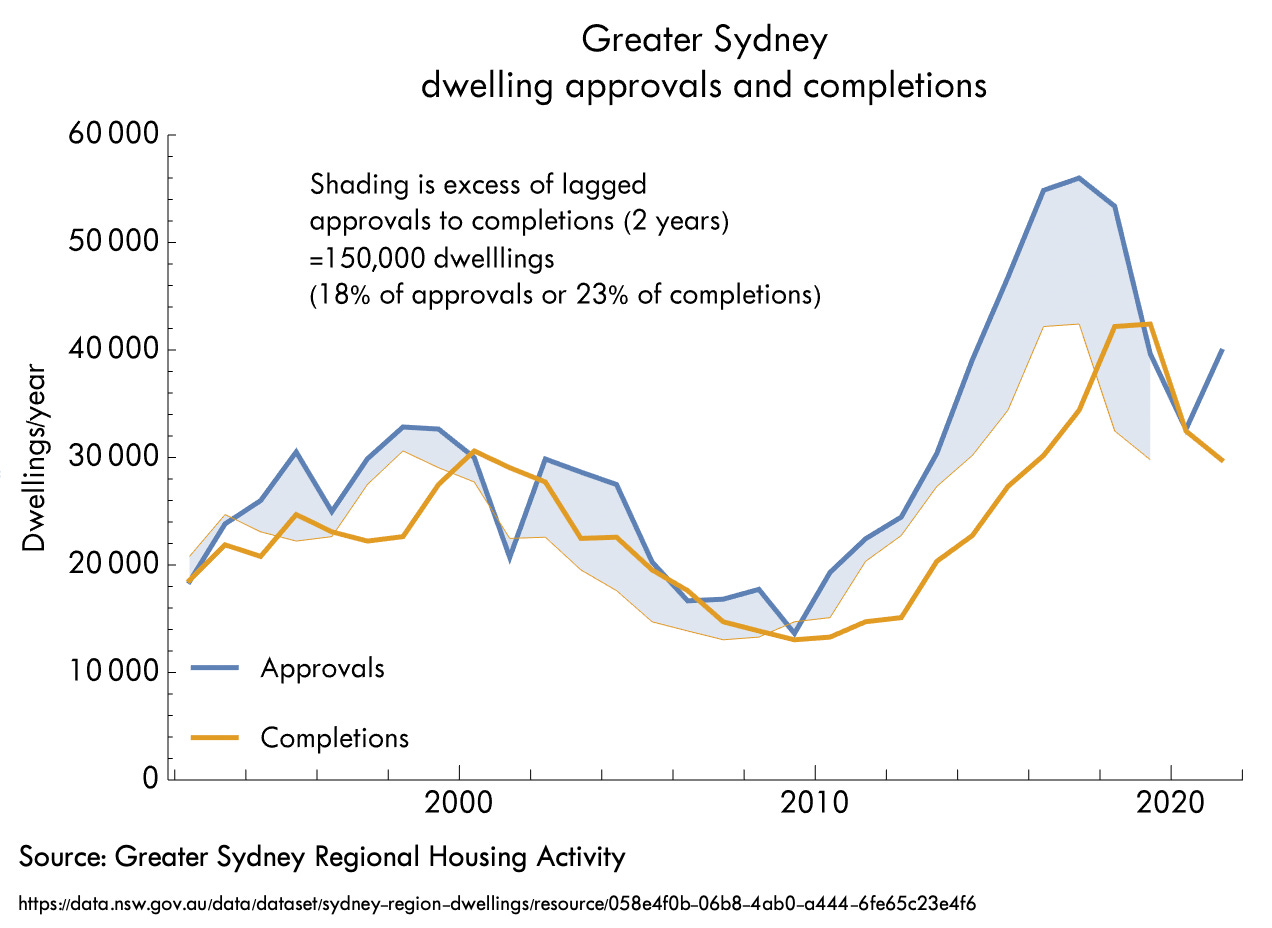

If we look at Sydney, we nearly the same pattern over the market cycle, and a growing number of unbuilt approvals during the peak years.

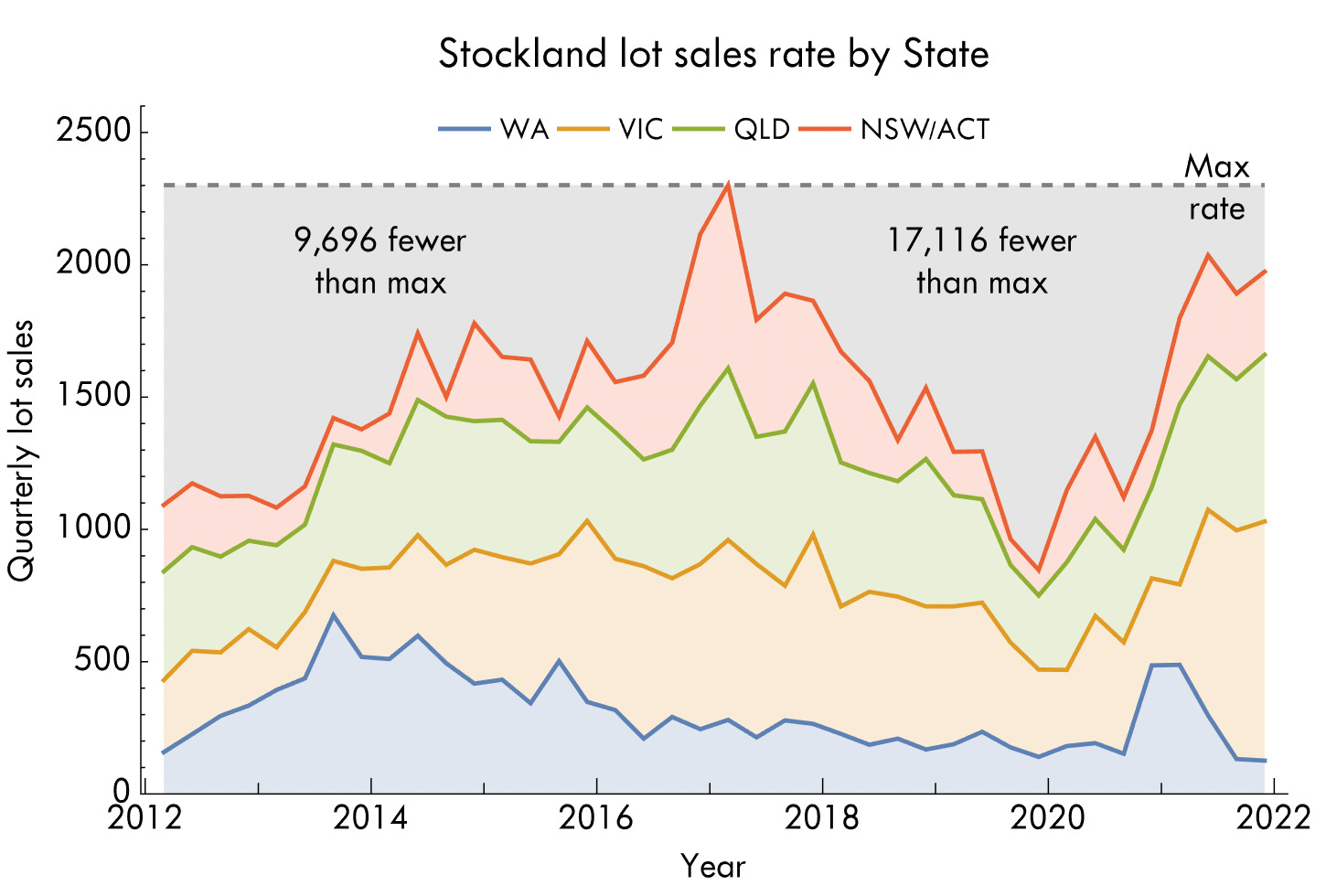

We can also look at an individual large housing developer. Stockland develops between 1,000 and 2,000 dwellings per quarter across its enormous portfolio (it has 10 projects per state on average).

They manage their sales to match market cycles, slowing dramatically when the market is soft.

Together these charts lead me ask—if developers won’t sell and build housing when the market is soft, what is the mechanism by which “unleashing supply” is meant to result in more housing forcing prices down?