The UCLA Lewis Center seems to have a problem

The financial interests of their wealthy property developer funders always come out on top in their weird and illogical reports on housing

The Ralph & Goldy Lewis Center for Regional Policy Studies at UCLA is funded by a major property developer. While the group often lobbies for progressive causes, there appear to be financial interests working in the background, ensuring particular views are espoused, and people who hold those views are hired.

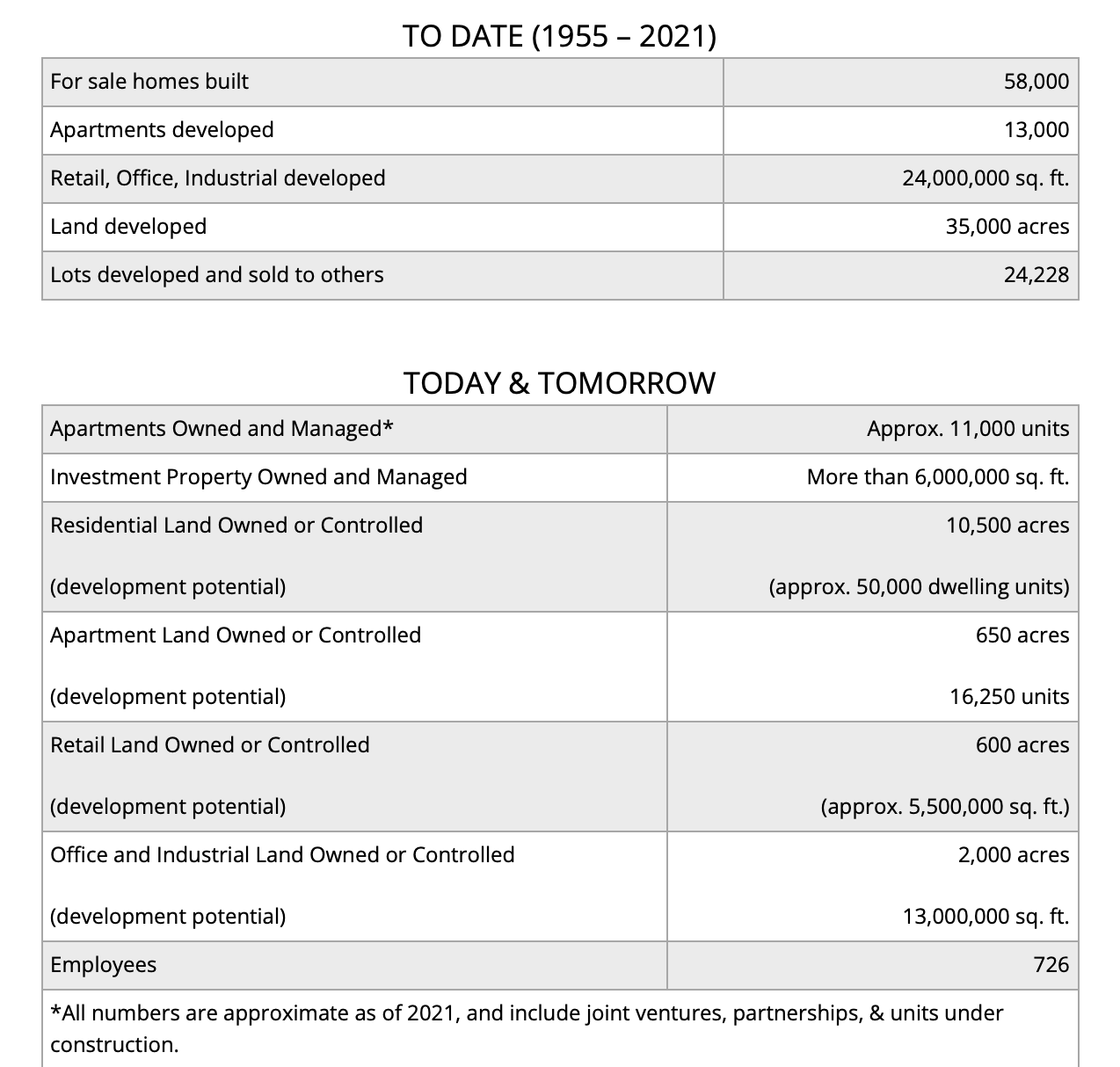

The Lewis Group of companies founded the centre back in 1989. In 2019 the Lewis Center launched its “Randall Lewis Housing Initiative”. Randall Lewis is the Senior Executive Vice President for Marketing at the Lewis Group of Companies.

The Lewis Group of Companies is one of the biggest housing developers in the United States. They report having a landbank of over 50,000 detached homes and 16,250 apartments, and own and manage 11,000 rental units. Their landbank is more extensive than most of Australia’s large publicly-listed property developers like Lendlease, Stockland, Mirvac, and PEET.

The Lewis company sold their actual construction business in 1999 and has since been a land speculation company, as reported here in 2014.

The company, which reported more than $1 billion in assets in 2004, sold its homebuilding division in 1999 to the venture that became KB Home. The sale brought in liquidity and transitioned the company to one that put Lewis in a more speculative position as a master-planner and manager of residential, retail and commercial development.

In that same 2014 article, Randall Lewis is quoted explaining the company’s landbanking and drip-feeding strategy quite clearly, with a target of building only 3% of their apartment landbank each year (500 out of 16,500).

…the Lewis Group has shown it is forward-thinking and strategic in its approach.

“We would like to do 500 apartments per year over the next five to 10 years,” Randall Lewis said of the Homecoming and Santa Barbara lines, which are among several lines of rental homes designed for California and Nevada that go back as far as 2004.

This collection represents a fraction of 15 to 20 master-planned communities — that the Lewis Group has on the books.

There is no way that a land speculation company with a balance sheet in the billions has an interest in policies that bring down the value of property assets or force them to develop faster than they want. They are also a landlord with 11,000 units. So they will never allow any admissions that rent control can be beneficial, just as they will never promote any policies that reduce housing rents by other means.

This is why, like the property lobbyists in Australia and elsewhere, the research from UCLA’s Lewis Center is heavily focused on planning regulations. A focus on planning provides a good excuse to boost the density of homes allowed on a particular property, which is beneficial for current owners but doesn’t impose a time limit on when or how fast they are built. These rights to higher density development just get added to the landbank for free.

That the Lewis Group could build 66,000 dwellings with no zoning changes if it wanted on property it already owns, but only plans to develop a few per cent of them per year, is a fact that the UCLA researchers have a huge incentive to ignore.

Two UCLA Lewis Center reports reveal the logical contradictions and peculiar reasoning that come about when trying to shoe-horn reality into policies that suit your financial backers.

A review of planned capacity and affordable housing

A commentary of value capture

Planned capacity

The first report concerns the capacity for new homes in the planning system.

They look at zoned capacity (called “inventory” in the lingo of the regional housing needs allocation, or “RHNA”) in cities across California and find that only about 9% of it is taken up in an 8-year planning period.

They go further to note that the zoned capacity estimates are terrible anyway.

It turns out that more than 70% of new Bay Area homes during our study period were built on non-inventory sites. Also, in larger cities, projects that were proposed and approved on inventory sites tended to have more units than what the housing element assumed for the site. (p8)

It has been known for decades that zoned capacity estimates in the RHNA process are terrible predictors of actual housing outcomes, and compliance with zoned capacity estimates has no effect on outcomes. This research from 2003 found

…no detectable relationship between housing element compliance and the percentage increase in housing across these communities during the 1990s. Thus, for all the potential merits and benefits of housing element compliance, one must look to other factors to explain why some cities experience rapid housing development and other cities experience little.

Other work relied on in this report is by Romem, who showed that just a fraction of a per cent of property parcels in Los Angeles end up with permits for new housing each year. I’ve put that data in the below charts. Notice the more than 3x variation through the cycle.

This evidence would suggest that zoning and planning are not binding on the overall rate of housing development (i.e. the absorption rate). The estimated zoned capacity is 11x more than used, variation of more than 3x occurs within any capacity limit, and even then, sites are usually developed to higher densities than the estimated zoned capacity. And most development happens on other sites anyway.

This does not support the idea that a fixed per cent of zoned capacity gets pushed into development.

But the authors of this report instead ignore this evidence and conclude that more zoned capacity (inventory) must be made available and will be forced through to new dwellings at a ratio of 1:10 of that capacity. They explain their reasoning with this analogy.

It’s like a university that wants 1000 students in its freshman class deciding to admit just 1000 students, even though the university knows from past experience that only about a quarter of admitted students will enroll. Given a 25% yield, the university needs to admit 4000 students, not 1000, to fill a class of 1000. Similarly, if a city knows from past experience that only about a quarter of developable sites tend to get built out during an eight-year period, the city needs to zone for four times its RHNA in order to accommodate it.

I like the analogy of student admissions. I’ve used it before to explain the exact opposite claim that planning is not binding, and why their interpretation does not follow the evidence they present. They keep assuming in various ways that the market wants to build faster, even though their evidence is that property owners are essentially unconstrained by the made up zoned capacity figure. They cannot comprehend that the market has a built-in speed limit on development.

If the researchers truly believe this I would suggest the talk to their benefactors the Lewis family. Ask them about how quickly they develop new housing and under what market conditions. Maybe ask what they are doing with a landbank of 66,000 dwellings.

By the way, the same nonsense process of requiring councils to meet housing targets through their zoning applies in much of Australia too. And the same lack of relationship between targets and outcomes happens here too. Maybe that’s something to look into.

Value capture

A second report is on upzoning and why it doesn’t add value to property. This report pushes the same “more capacity forces more new housing onto the market” line.

They start with the competition story about property rights that I recently debunked. They consider two scenarios of incremental upzoning and mass upzoning and explain the logic of price competition that they think will follow mass upzoning like this.

There’s land zoned for higher density everywhere; the right to build more is no longer a precious commodity. A property owner with an upzoned parcel can sell their home for $600,000 to another homebuyer, as they could prior to the upzoning. But can they sell for $900,000 — $300,000 per developable unit — as in the first scenario? The answer is no, they cannot.

The owner can’t sell for $900,000 because their neighbor will happily sell to a developer for $800,000, which is less than $900,000 but more than any homebuyer would pay. The developer can comfortably outbid the homebuyer at that price, and there’s no reason to pay more. Half the town’s parcels are zoned for triplexes, after all, so as a developer there’s no need to pay much more than a homebuyer would: If they lose this bid, there are plenty of other properties to choose from. And if one neighbor is willing to sell for $800,000, another will probably accept a price of $700,000 — again well above what a homebuyer would pay, ensuring that a developer will win the bid, but well below the prices in the first scenario. The original owner, unable to capture the windfall for themselves, may settle for a price of $610,000 or $615,000.

This is nonsense. We know this because property assets are not priced based on cost. After all, most homeowners paid a small fraction of today’s market price and there are millions of potential sellers out there who, under this logic, would “happily sell” for a lower price than what prevails in the current market. They just assume people will sell property assets worth $900,000 for much less because many people own similar assets.

They then show a case study of how upzoning led to a doubling of property prices, then repeat the same competition argument with some more hypotheticals.

Value capture is unnecessary in the context of broad upzoning: Lower land prices will automatically be “captured” in the form of lower rents and sale prices. Windfalls aren’t needed to spur redevelopment, meanwhile, because eligible sites are abundant and readily available.

Imagine, for the sake of argument, that every parcel in Los Angeles currently zoned for single-unit detached homes, duplexes, and triplexes was rezoned to allow up to 10 units in modest three- and four-story buildings. With more than 400,000 such parcels in Los Angeles11, this would increase the city’s zoning capacity by at least 3.6 million units, 2 1/2 times the city’s existing stock of 1.4 million homes and more than its estimated capacity in 1960.

Let us not forget that Romem’s study showed that already Los Angeles has a zoned capacity that exceeds the current total stock of dwellings and a growing capacity. The argument here is that having 1.4 million dwellings in zoned capacity is insufficiently competitive for the production of 15,000 to 20,000 new dwellings per year, but 3.6 million will see price competition magically emerge.

The City of Los Angeles currently has about 1.38m existing housing units in the sample of parcels considered for its housing element. If each parcel that allowed for housing was redeveloped as 100% residential to the maximum number of allowable (base) units, the number of housing units in the City would more than double. The City’s zoned capacity has increased since 2010, especially after accounting for bonuses, likely due to the introduction of the City’s Transit-Oriented Communities (TOC) program.

The competition logic is plain wrong. Upzoning gifts real property rights worth real money to existing property owners.

Before I wrap up I want to also mention this report, which sensibly calls for more tax revenue to be raised from property transfer taxes. But it recommends exempting newly developed housing from the property transfer tax, something that would suit a large landbanking property developer—don’t tax their land holdings, nor the property sales they make, but tax all the property trades by others.

This report also directly contradicts the main claim in the value capture report when it states “…home prices are not determined by cost to the seller, but by demand” (p9).

Stuff like this is why I get a weird vibe when I read housing research from the Lewis Center. I’m not saying the researchers there are bad. Nor do I think they are actively conspiring in the interests of their supporters. Organisations select people with similar interests to get on board and financial motives usually steer the ship.

Some might argue that my own research group at the University of Sydney is funded by a major property owner and hence I am hypocritical for pointing this out, but I don’t think so.

Warren Halloran (1926-2020) made the decision to fund my research group in 2012. He was the son of Henry F. Halloran (1869-1953) who made substantial wealth in New South Wales property in the first half of the 20th century. Warren used the wealth he inherited and then built upon for a variety of philanthropic causes, one of which was to promote urban research.

It would be a very different story if I worked for a research group funded by one of Australia’s biggest active private developers, like, say, Harry Triguboff. You would be right to question the incentives at a hypothetical “Triguboff Housing Initiative” whose main ideas involved policies that made their benefactor more money.

The first thing that jumps out to me when they say "The developer can comfortably outbid the homebuyer at that price, and there’s no reason to pay more." is why would you assume the market is made up of a single developer and many homebuyers?

Developers aren't competing/bidding against just homebuyers, they are also competing/bidding against multiple developers who would all progressively bid up the price to the highest and best use i.e. the residual captures the full value of additional development rights irrespective what rights the sites surrounding it currently have.

Your argument that increasing "zoned capacity" doesn't increase development is based on a total misunderstanding of California housing law. A compliant housing element, especially pre-2022 cycle, doesn't increase zoned capacity. It just studies sites where a city _could_ increase capacity. Many didn't. Many others were just non-compliant without consequence. Most others found other ways to prevent development or make it otherwise financially infeasible (FAR, parking minimums, uncertainty around timeframe and approval), as the authors in the papers you cite all point out. Did you read their papers?