Submission to NSW Productivity Commissioner

Review of Infrastructure Contributions

Dr Cameron K. Murray

Henry Halloran Trust, The University of Sydney

May 2020

Download this submission as a pdf here.

Summary:

I argue that betterment is a more transparent, efficient, and certain tax base for raising council revenue for infrastructure or any other expenses. Compared to fixed-rate infrastructure contributions levied on a per-new-dwelling or per-new-building-area basis, a tax on betterment automatically adjusts to local economic circumstances, boosting efficiency.

I recommend the following:

a. Infrastructure contributions be scrapped in NSW.

b. Betterment from the planning system should be called “Community Development Rights” and a betterment tax should be implemented and called a “Sale of Community Development Rights”, or SCDR.

c. An SCDR be required at the time of planning approval.

d. The amount of to be paid for SCDR be calculated at 75% of the difference in site value when valued “at current use” compared to “at approved use”.

e. These valuations should be undertaken by a third party, rather than councils, such as by NSW Revenue using valuation expertise from within the State government.

f. Payment of the SCDR will be via

i. a 10% deposit of the assessed tax when planning approval is issued and,

ii. the balance on development completion (prior to registering the new plan).

g. For simplicity, in high-growth areas a schedule of pre-calculated betterment tax amounts on a per-dwelling or per-building-area basis can be published. These schedules will be produced by valuers based on local market conditions, borrowing from a process used in the ACT in 2012.

Key points

1. The Terms of Reference for this Review are focussed on economic issues such as improved transparency, efficiency, and certainty of infrastructure contributions. These are desirable features of an infrastructure contribution system.

However, these are not the features of a system desired by those who pay them. If contributions are raised, even if levied in a more transparent, efficient, and certain way, I expect these economic objectives to suddenly become irrelevant to the development industry. This needs to be acknowledged up front.

The development industry mostly wants lower infrastructure contributions.

For example, Queensland implemented changes to tighten up and clarify its infrastructure charging regime in the 2009 Sustainable Planning Act. These changes ensured a tight nexus between the forecast costs of identified trunk infrastructure and the rate of the charge. These infrastructure charges were published in a simple schedule (an Infrastructure Charges Schedule) linked to a supporting document that identified the infrastructure upgrade and investments planned by councils (the Priority Infrastructure Plan). It was transparent, efficient and certain.

However, because many of these charges increased, rather than decreased as expected by developers, they then lobbied to have them capped, which was swiftly done by the Bligh government in 2011.[1]

2. There is a conceptual conflict between the idea that contributions reflect efficient costs while also complying with the principle of beneficiary pays. Benefits of infrastructure investment, as reflected in the value gains to nearby property, may be less or more than the cost of new infrastructure.

3. Betterment is the name for the value gain arising from increases in property value due to external factors, such as local infrastructure or new property rights granted to landowners through the planning system.

4. For property redevelopment, betterment is the value of the new property rights that allow for that development to take place, which are, until then “owned” by the community. We know this because redevelopment rights can be sold to property owners by councils, rather than given for free.

For example, in São Paulo, Brazil, auctions are held periodically to sell to landowners the rights to construct additional density, called Certificates of Additional Construction Potential (CEPACS), raising around $USD 200 million/year in revenue.[2]

Using betterment as a tax base can help side-step many of the technical arguments used against infrastructure charges on economic grounds. Just as property rights are sold at market prices from the public when disposing of land, property rights granted through the planning system can be sold at market prices.

5. Since 1971 the ACT has taxed betterment at 75% of its market value to fund territory government activities. Their system is known as a Lease Variation Charge (formerly a change of use charge). In addition, by being the monopoly developer of land subdivisions they gain 100% of the betterment in converting rural to urban uses.[3]

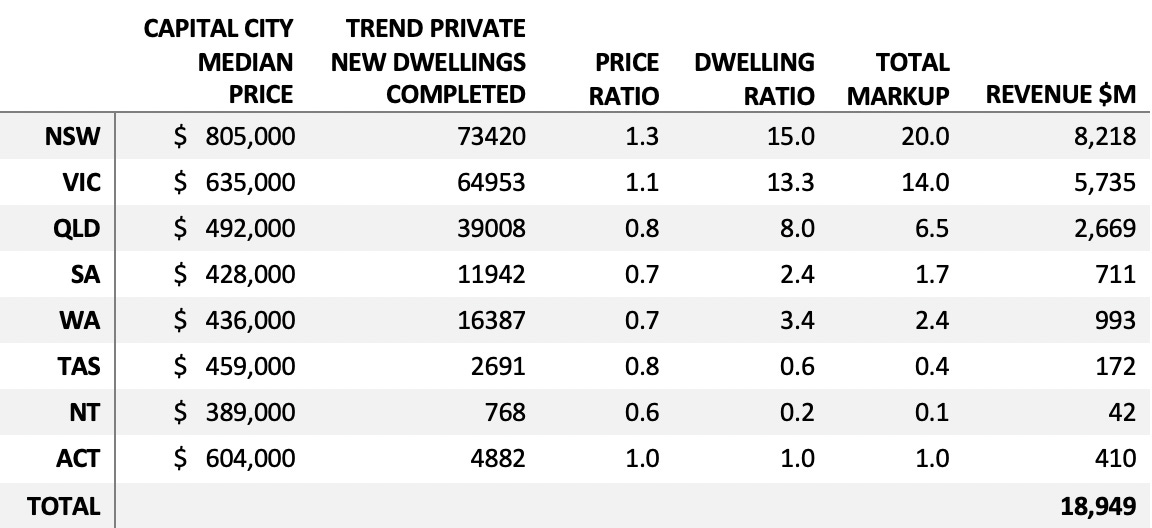

The below table scales up the revenue from these sources in the ACT for the difference in housing prices and new housing development in the other states, showing that if a similar scheme was enacted, over $18 billion could be gained by councils in other states using this mechanism.

In NSW alone, there was $8.2 billion of potential revenue in 2018-19.[4] Many other methods for capturing betterment for the public have been implements in Australian and abroad.[5]

6. This implies that over $12 billion worth of redevelopment rights, accrued to landowners in NSW at no cost through the planning system, were utilised in 2018-19.

7. From 1970 to 1975 NSW had a betterment levy of 30% of the value gain from the conversion of rural land to urban uses, raising $17 million in that time with $2 million in total administrative costs. This was used to finance the infrastructure necessary for expansion of the metropolitan region.[6]

However, political lobbying by wealthy landowners on Sydney’s fringe led to the demise of this funding mechanism.

In November 2007 the NSW Government foreshadowed a ‘Rezoning Infrastructure Contribution’ (also known as a ‘Staged State contribution’) to be paid either at the time of rezoning or at the time of sale. However, this approach was abandoned in the final package of reforms to developer contributions in NSW.

8. The beauty of using betterment as a tax base is that it prices property rights that are given away by the public that should be instead sold. The ACT system is equivalent to a 25% discount on the market price of the right to redevelop to higher intensity uses.

9. Additionally, like infrastructure contributions, the costs of a betterment tax or levy cannot be added to new housing prices. Instead, these costs are subtracted from the value of land prior to its development. On net, it is an economic transfer from current landowners to the community at large (via the council) that confers these new rights.

This is why the abolition of the Sydney Betterment Levy was such a political issue in city-fringe electorates—the value of the levy came off the value of the land with development potential.

10. Un-priced betterment is also the honeypot around which corruption emerges at both state and local levels. In most states, local councils have a history of corruption involving favourable rezoning and planning decisions. It is the fact that these decisions grant valuable new property rights for free to the recipients that fuels the corruption cycle. A recent example involves Casey Council in Victoria.[7]

A study I co-authored in 2016 showed that landowners in Queensland who were politically connected or employed profession lobbyists were much more likely to find their land within a rezoned area compared to near-identical neighbouring land, and in the process, these connected landowners gained $410m out of the $710m worth of development rights given to all landowners from these rezoning decisions.

UPDATE:

Certainty is greatly increased for the development industry by using betterment as a base for raising revenue as it solves the land purchase price dilemma. If planning outcomes are uncertain, the developer who is the most confident of a generous planning outcome will win any bid for the purchase of a development site. They will then require a generous planning outcome to justify the price they paid for the site. With a tax on betterment, they can pay only slightly above the value at its current use for the site. If they fail to get a generous planning approval then they pay less for the betterment tax. If they get a favourable approval, they pay more.