Rental vacancy is a symptom of price adjustment

If rents rise or fall this change must occur via the speed at which rental homes at current prices are taken up.

Welcome to new subscribers. If you like this, please check out some of my other posts, such as:

Don’t forget to subscribe and share. Scroll down to read on.

When the number of rental advertisements falls we often hear that rental “vacancy” is low, indicating a “shortage” of housing.

But this story confuses a number of concepts.

In this post, I do two things.

First, I show how rental vacancy in the housing market is analogous to the unemployment rate in labour markets.

Second, I explain how low rental vacancy is a symptom of the rental price adjustment process itself, not an independent force acting on prices (i.e. rental price change and vacancy are co-determined by the same process).

I also want to share a new “Explainer” paper of mine. It was written to help people interested in these topics grasp the underlying economic concepts, which I commonly see being misused. This post is based on material in that paper.

The labour market analogy

Two different economic concepts commonly get called the rental vacancy rate.

The number of rental advertisements in a period as a proportion of the estimated stock of rental dwellings.

The number of unoccupied dwellings in a period.

Confusion sometimes arises because in the United States the term housing inventory is commonly used to describe the first vacancy concept and the term rental vacancy is used to describe the second concept.

In Australia, the first concept is widely known as rental vacancy, and the second concept is more commonly known as unoccupied dwellings.

An analogy to the labour market is that vacancy (the first concept) is akin to the unemployment rate while unoccupied dwellings (the second concept) is akin to those outside the labour force. Just like it is possible in the labour market for the unemployment rate to fall while the number of people outside the labour force rises, the housing market can see a fall in rental vacancies at the same time as an increase in unoccupied dwellings (and vice-versa).

I did a quick Twitter poll to see if people thought the unemployment rate of people indicated a shortage in the stock of human beings. Most didn’t.

In my view, we should expect during a period of strong economic growth a decline in the unemployment rate of dwellings, just like we expect a decline in the unemployment rate of people.

But in my subsequent Twitter poll, many more people agreed that the unemployment rate for dwellings indicates a shortage in the stock of dwellings, rather than reflecting market conditions.

What does rental vacancy mean?

We can start unpicking the meaning of the rental vacancy rate (the first concept) by imagining a world with a fixed stock of renter households and a fixed stock of rental dwellings. In this world, the number of rental advertisements merely reflects the number of renter households relocating at the same time.

If the stock of dwellings and households was 100 each, and 5 households were looking to relocate that month, then the rental vacancy rate would be 5% if all dwelling owners were also seeking to match with new tenants. If only 2 households were looking to relocate that month, the vacancy rate would be 2%.

Since each renter household would be both vacating a property and renting a different property, there would always be a one-to-one relationship between renter households looking for a new home and rental vacancy.

The size of this flow would be seasonal, depending on when renters typically look to relocate.

But what about more than seasonal variation?

Trends in rental vacancy that are more than seasonal therefore reflect either

the process of repricing rental markets, because when rents are rising the need for advertising diminishes and searching is quicker, and vice-versa, or

a relative change in the total number of households relative to rental stock, such as from a reduction in household size, or

a combination of both factors.

I think reason 2. has been a factor at play in the COVID era, and there is plenty of evidence of declining occupancy rates (people/dwelling)/

But reason 1. is all but ignored in analysis of rental markets, even though it clearly plays a massive role.

Even if there are the same number of renter households, and the same number of rental dwellings, a repricing of rents will involve a decline in the rental vacancy rate. The number of advertised homes at any one time will appear to shrink as renters rush in to beat rising rents.

Just like when the price of company shares adjusts, the sell-side order shrinks relative to the buy side.

In the labour market, we currently see a decline in jobseekers advertising their wares, which is the flip side of rising job advertisements from employers. This merely shows the market adjustment process. It doesn’t provide information about whether there are too many employers (too many renters), or too few workers (not enough dwellings).

Declining rental vacancy and rising rental prices are both symptoms of the same underlying market adjustment process.

Don’t believe me?

We see claims of housing shortages in every market when prices are rising. It happened in the housing asset market in Spain and Ireland and all over the United States right up until the 2008 financial crisis. Then suddenly, there were houses everywhere!

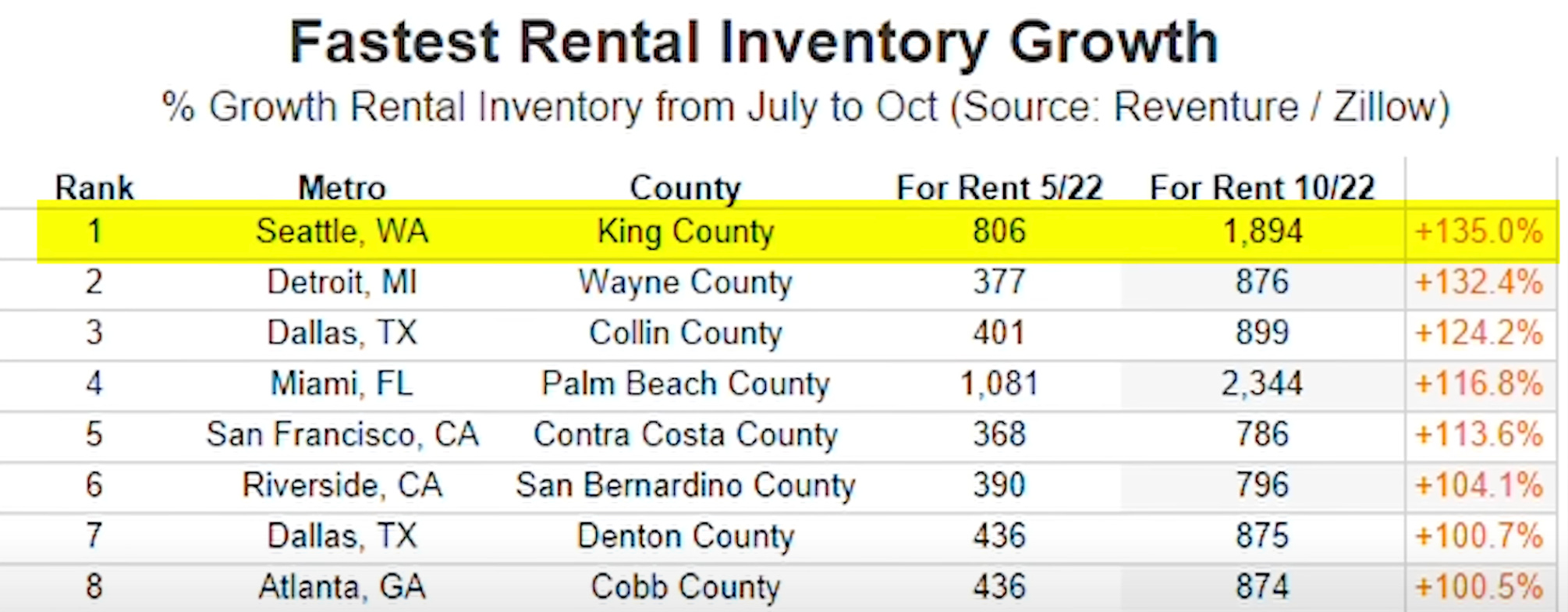

The same thing is happening now in the United States, which I think is economically about six months ahead of Australia in terms of macroeconomic cycles. Take a look at the booming

Check out this video with some recent data on this topic. Although, if we’ve learnt anything from this post, it is to keep an eye on the dates used to show the rise in rental advertisements. It’s not comparing to a year ago, but five months ago. This risks showing seasonality only. Though it does seem like such large moves are out of step with the usual seasonal trends.

Worth investigating further

One interesting pattern I’ve noticed looking at rental market data is that higher turnover in rental markets is associated with falling rents. Yet in housing asset markets, higher turnover is associated with rising prices.

This is perhaps due to renter households choosing to stay at the end of their lease to avoid paying rising market rents but relocating when rents are falling to find better value accommodation options.

And in asset markets, it could be the feedback loops of buyers being attracted to rising prices themselves.

But this needs to be investigated further.

Don’t forget to read my new paper— Explainer: Rental price and vacancy metrics —and below is the latest Fresh Economic Thinking podcast if you missed it.

I feel the polls are poorly worded. My visceral reaction to the first question was , no the people are of the correct quantity it is the job numbers which would be wrong, so I felt the poll would be happy influenced by this implication that there can be the wrong number of people to fulfil economic requirements . Although this was a simple poll to try and support the article it left me with an immediate bad impression of academically poor data research and that you support that in economics we may need to adjust the number of people to meet some requirement.

The agent terminates the lease saying the house is being put on the market, but actually pushes up the rent excessively for the next lease. The renter goes out to find a more affordable rental.

This is a manipulated market, the real estate agents are organised, renters are isolated and disempowered.

Pushing renters out at the end of a lease allows the rent to be increased excessively, also causes increased apparent demand.