Ownership illusions: Competition

Part 1: If our theory of competition relies on the incentives of owners, how do we handle broad structures of cross-ownership?

I have a new working paper out with co-author Tim Helm, entitled Ownership Illusions: When ownership really matters for economic analysis.

The basic argument is that in economics, a common unit of analysis is the firm. Firms are assumed to independently maximise profits, subject to the well-recognised caveat that incentives of owners and managers can differ. Less well recognised is how ownership structures themselves affect incentives, behaviour and economic outcomes. With the wrong assumptions about ownership and when it matters, economic analysis can misrepresent economic reality.

We call this class of situations ownership illusions.

In the paper, we look at four situations where failure to recognise the structure of ownership leads economic analysis astray.

In competition policy, the incentives of firms are blurred by cross-ownership, leading to questions around the validity of default models and exactly how the incentive-driven process of competition is to be understood.

When assessing the economic performance of private or government-owned businesses, the capital value of ownership is usually ignored when in public ownership but is a primary metric of success when in private ownership.

Retirement income systems reliant on individual ownership of financial assets are often inaccurately described as “pre-funded”, by way of contrast with pay-as-you-go or “unfunded” public pensions, regardless of differences in underlying capacity to support cashflows but simply because there exist no priced ownership rights for future pensions.

In housing policy, the idea that competition between landowners can push down land prices reflects incentives from product market models where ownership dispersion matters, not those from the “location franchise” model of monopoly that land involves in reality.

Today, I want to expand on the first of these situations.

Part 1: Competition and cross-ownership

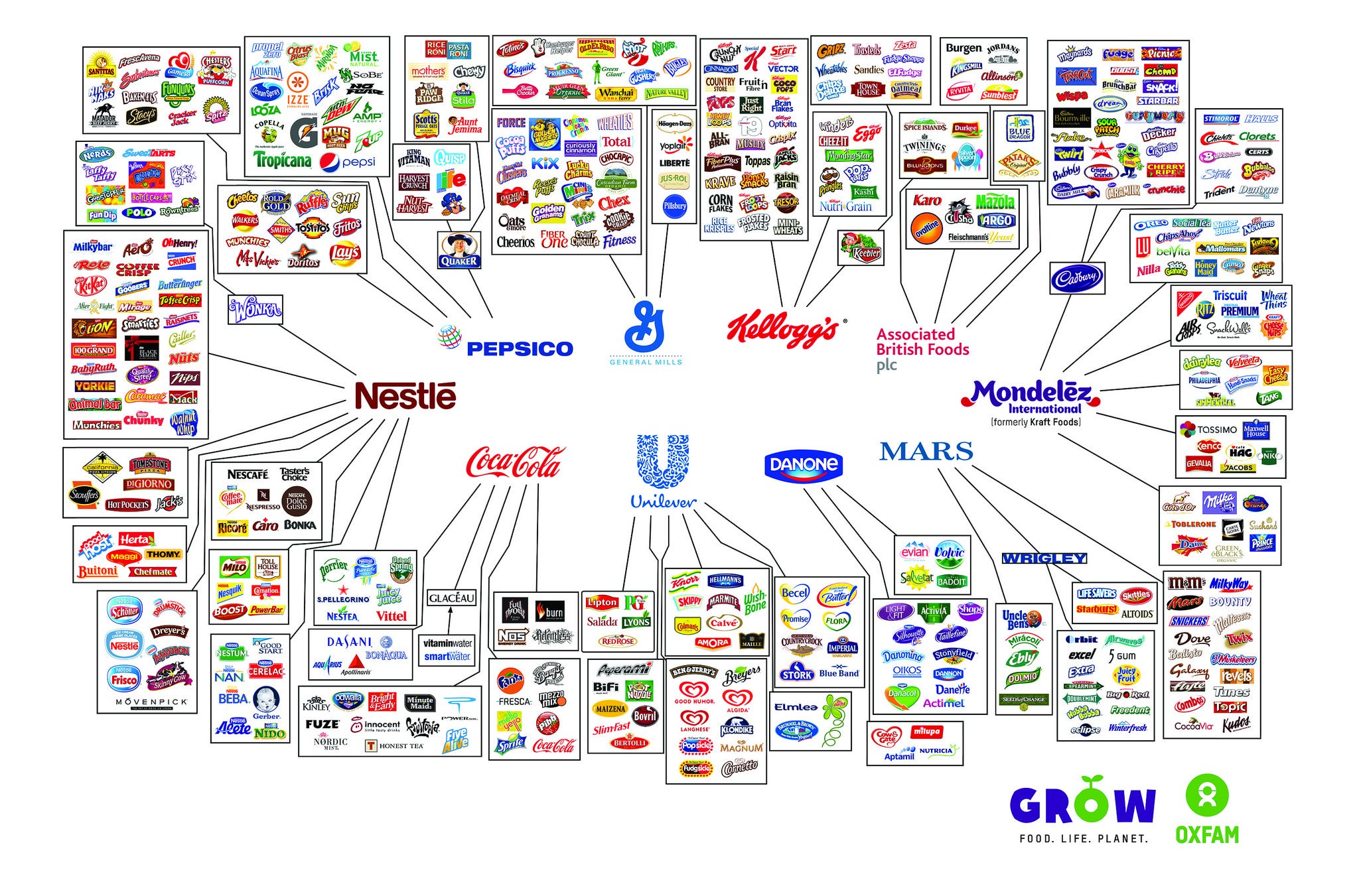

Most people have seen some variation of the above image. Or this one, which shows how 14 companies own just about all the car brands in the world. These images help highlight that ownership of brands matters for the way they compete against each other. It would be wrong to look at the image of hundreds of consumer staples brands and think “wow, what a competitive market”, ignoring that there are only nine companies that own all these brands.

I show a simplified diagram below of how we need to look at the ownership of brands to understand competition, because of the connected ownership structure via companies.

Now let’s take another step.

Who owns the companies themselves? It is possible that one person owns each of them. Or a group of people own part shares of one company.

But another scenario is that a thousand people could each own a one-thousandth share of all companies. Or a million people own a one-millionth share of all companies.

In the below diagram I show the simplified case of three owners, part-owning three firms, that each own two brands.

In this latter case of broad cross-ownership, how are profit-maximising firms going to behave? There is, after all, just one ownership structure here, so there are no independent financial incentives. All owners have the same incentive, which is for the firms to maximise their joint profit.

This is a problem for both economic theory and policy.

We explain.

One implication concerns the fundamental basis for competition itself. If cross-ownership does not affect the behaviour of firms, then the premise that competition is driven by the profit motive of owners is called into question. If it is not owners’ incentives that cause markets to deviate from monopoly outcomes, then what is it?

One possibility is that while incentives drive competition as normally understood, effective co-ordination of incentives under cross-ownership relies on operational control; ownership per se is necessary but not sufficient. Owners of minority stakes in multiple firms may be unable to effectively pursue their collusive interest when the controlling majority owners have incentives to compete. A further confounding factor is the rise in interlocking company directorships which has occurred alongside the rise of cross-ownership (Heemskerk, 2013). Does the control exerted via these formal corporate positions support cartel-like coordination? Would interlocking directors have the same collusive incentives without cross-ownership? These are questions that need further examination.

Alternatively, the notion that market outcomes have their causal origin in market concentration as the key determinant of firm behaviour may be incomplete (this is referred to as the structure-conduct-performance paradigm; Sutton 2001). The correct arena of competition may not be one of strategies set by reference to rivals and demand, within which more competitors mechanically produce more competition. It is known that if individual firms use trial-and-error experimentation for price or output decisions, a single market with many firms can converge to the monopoly outcome without explicit cooperation (Huck et. al., 2004). If collusion through trial and error is common, it raises deeper questions about the value of multiple firms, and the causal significance of concentrated ownership. Independent ownership may be of lesser relevance to price-setting than other elements of competition, like free entry.

A second implication concerns the policy environment. Regardless of how the theoretical understanding of competition evolves in an environment of broad cross-ownership, secrecy in ownership networks is likely to inhibit progress in understanding their implications. In most countries, a complete mapping of beneficial company ownership is either impossible, or held secret, and additional ownership layers are often added to the network to conceal the underlying beneficiaries. If progress is to be made in understanding firm behaviour and competition under well-connected ownership structures, observing those structures is a first step.

Of course, we are not the first to note how broad cross-ownership of firms brings a lot of economic thinking into question. We include it as a key example in our class ownership illusions because it is especially relevant to both theory and policy, and because it clearly shows how asking the question “who owns what” can radically change subsequent economic analysis.

Next time, we will look at how ownership illusions are at play in policy debates about privatisation, public business operations, and public financial investment.