Oh no, home prices are above marginal cost!

There's a strange academic debate about whether the market price of homes should equal their marginal construction cost. Here's why that idea doesn't make sense.

This article is for paid Fresh Economic Thinking subscribers. Please support FET and enjoy detailed analysis such as this by upgrading to a paid subscription.

Maybe also check out the Fresh Economic Thinking YouTube channel where interviews and free podcasts are posted regularly.

What is the marginal cost of producing an extra home? This article gets into the weeds and was prompted by this tweet about where the price of homes comes from.

Price would equal MARGINAL construction cost. Otherwise, there would be an incentive to keep building.

But marginal cost exceeds average cost.

So P = MC > AC.

P-AC is the value of land, often called the site value.

This idea dominates a lot of housing economics. Here’s Harvard Professor Ed Glaeser in the Journal of Economic Perspectives.

…we show that the cost [CM: market price] of Manhattan apartments are far higher than marginal construction costs

Comparing the market price of dwellings to marginal construction costs to claim regulations increase housing costs is the core piece of evidence relied upon to argue about the effects of planning regulations.

Here’s a study from RBA researchers Ross Kendall and Peter Tulip making a similar point. And below is a typical tweet making similar claims.

So what does price is higher than marginal cost even mean?

What’s the marginal cost of extra homes?

Let’s say it costs $1 million to build a five-storey apartment building with 10 apartments, so the average construction cost is $100,000 each (which is AC, or average cost). Before construction, it may be possible to redesign the building and incorporate an eleventh apartment. However, the total construction cost of this design might be $1.2 million, which means that the extra cost, or the marginal cost (MC), of the eleventh apartment is $200,000. It costs $1 million for ten dwellings, but $1.2 million for eleven.

Therefore, all similar apartments in this location, under these cost conditions, should be priced at $200,000, as this is the marginal construction cost of an extra apartment in this building.

If apartments were priced in the market at less than $200,000, it is certainly true that eleven apartments wouldn’t be constructed on this site, as the property owner makes less money compared to building ten apartments. If apartments were priced at $180,000, building ten apartments leaves you with $800,000 after construction costs ($180,000 x 10 minus $1 million), but building eleven leaves you with only $780,000 ($180,000 x 11 minus $1.2 million).

When the number of apartments in a building is unconstrained, it is true that when and if a building is developed, it is optimal to not build any denser than where the marginal cost of adding another apartment to the building equals the market price of an apartment.

But what is not true are the additional claims that a gap between price and marginal cost determines the price effect of regulations on density.

Here are three reasons why.

What’s wrong with this claim?

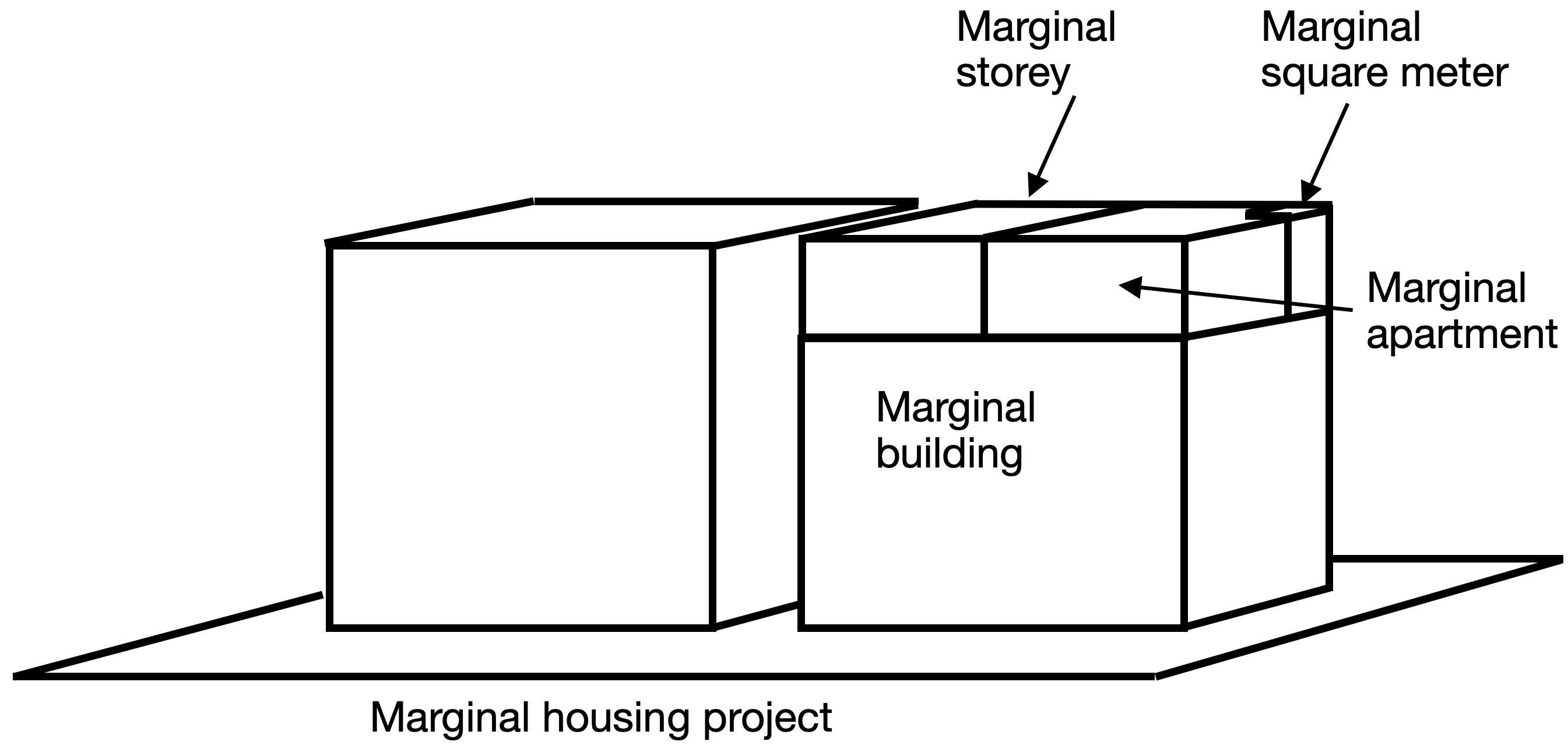

1. The coastline paradox or Russian doll problem

We have so far only looked at an extra marginal dwelling per site (the marginal dwelling density). But there is also the marginal storey per building (the marginal height), a marginal building in a housing project (the marginal building), and at each location there’s a marginal housing project (the marginal project)!

Within each dwelling, there is also the marginal square meter of extra space (the marginal size), which could come in the form of the marginal bathroom, bedroom, patio space, or extra car park, each with its own marginal cost. There are quality margins as well.

Let’s not forget that there is also the marginal dwelling built per period of time (the marginal absorption rate) to consider, something that is always ignored.

Here’s an illustration of this Russian doll of margins in new housing.

Here’s the first problem. On which of these margins should price equal marginal construction cost?

It can’t be all of them.

We know that construction cost for a dwelling with the same market value increases with density. Because of this, the smaller the margin you measure, the higher the marginal cost observed.

Here’s a table with a stylised round-number construction cost profile for these margins for a housing project with 20 dwellings in the following arrangement.

Two buildings

Five storeys each building

Two dwellings per storey

100 square meters per dwelling

Notice anything? Many margins mean many marginal costs on a per-dwelling basis.

Now imagine that I go and look at construction costs and market prices of buildings traded and see that the marginal cost of a building is $1,000,000 but the market price is $4,000,000.

What can I infer here?

Now imagine that I go and look at construction costs and market prices of dwellings and find that the marginal cost is $200,000 and the market price is $400,000.

What can I infer here?

Finally, I look at the construction cost and market prices of square meters of apartment space. Here, I see that the marginal cost is $3,500 and the price is $4,000.

These are all just arbitrary units of measurement. One says that three-quarters of the market price is a deviation from marginal cost. Another says that half is a deviation. And another says an eighth is a deviation.

Which one shows the price effect of regulation?

This problem is akin to the coastline paradox. Depending on the length of the ruler you use, you get a different length of the coastline. A longer ruler means a shorter measured length. In our case of dwellings, this means that the larger your unit of measurement, the lower your marginal cost relative to the price of that unit.

2. The density problem

Another problem is that the marginal cost of adding an extra dwelling of equal value rises with the density of housing projects.

The extra marginal dwelling in a five-storey building has a much lower cost than the marginal dwelling in a 100-storey building. The marginal cost of adding height and dwellings when designing tall buildings can be double or more than that of smaller ones. The charts below are from my Feasibility Guide for Planners. They show the rising average cost per square meter for denser projects, and even faster rising marginal costs.

So which marginal cost sets the price of housing in an unregulated market? Is it $2,500 per square meter? Or $8,000 per square meter?

We can only know if the price is above marginal cost if we assume a particular density. But there is a density where the marginal cost will equal any price. There is not one marginal cost, but many different ones. The point where marginal cost equals price only tells us at a specific point in time what the profit-maximising density is at that time. Once a building is built, markets change and it immediately becomes the “wrong” density again. I explain this density equilibrium concept in detail in my new book The Great Housing Hijack.

Even if regulations limit density to a point where the marginal cost at that density is below the price, it doesn’t tell us anything about the quantity of homes, since density and quantity are not the same.

3. The true marginal cost problem

The difference between density and quantity brings us to the final problem. The input cost of constructing one extra dwelling of density on a site not the marginal cost of a dwelling per period. It is the marginal cost of density or dwellings per site area.

The marginal cost of building homes during this period (the marginal cost of production) must include the opportunity cost of the next best alternative. This includes the cost or benefit of waiting until the next period.

At any density, whether this is regulated below a density that might otherwise be chosen, the marginal cost of developing homes today is the forgone benefit of waiting until tomorrow.

Developing housing is a portfolio reallocation. Waiting provides a return from the increasing value of owning an undeveloped site asset and a return from interest on the cash asset that needs to be combined with that undeveloped land to get a new housing asset. There are also effects of building faster today that depress prices tomorrow. Thus, the marginal cost of building an extra new home today (housing production, or supply) is the forgone return from waiting.

This is the problem I tried to explain in my Housing Supply Absorption Rate Equation paper in The Journal of Real Estate Finance and Economics.

But no one cares about this more appropriate marginal cost for some reason. Indeed, there is widespread confusion about density and supply. The whole idea that the marginal cost of extra housing density should equal the price stems from this misunderstanding.

So what?

We need to throw out the idea that when the price is above marginal cost we have learnt something about the quantity of homes in a market relative to some optimum. Instead, all we know is that today’s market prices mean higher densities are probably privately optimal for some property owners should they decide to build homes today. But will they? Because they know that there is a cost of developing today in the form of forgone returns to waiting.

Did you know that Fresh Economic Thinking is now on YouTube? Check it out and subscribe to the channel to catch videos of Cameron’s interviews and future video content.

Sounds like you think it's impossible to operationalise the concept of marginal cost of supply in any diagnostic test of the competitiveness of housing markets, and how regulations vis-a-vis the natural monopoly in land contribute to that.

That seems quite significant.

To paraphrase you, cost data can be used at best to measure the marginal cost of production, not supply, because the economic (i.e. opportunity) cost of supply includes not just production costs but the value of foregone options. (For infill I'd note this includes not only the pure value of delay but the value of extant capital lost to premature redevelopment). And even then, how you measure the marginal cost of production changes the result.

And as a practical matter, even if these problems were avoidable, any test could only apply to brand new buildings, since the optimal density evolves.

Sound about right?

When someone wants to buy a house, they calculate the amount of money they need and then seek out financing to find a home that fits their budget. In essence, the housing market is not really about housing, but rather about money. In the realm of money markets, the cost of obtaining financing has no direct correlation to the cost of a house let alone the marginal cost (whatever that might be).