The Marginal Cost Controversy and its missing solution

The most famous economic minds never recognised the nested nature of economic margins. This has led to many confusions.

In the 1940s, there was a heated academic debate in economics, now referred to as the marginal cost controversy.

It is still relevant today.

Just last week, I read a paper that had to make assumptions about marginal cost and price, which showed me that the controversy is far from resolved. And indeed, the controversy is very much alive when it comes to the price of land and housing (as I explained here).

The basic controversy rested on the assumption, which still prevails today, that prices being equal to marginal cost is the welfare-maximising point of economic activity.

Marginal cost is the cost of producing an additional unit of a product in a given period, taking as given the stock of capital and other historical sunk costs.

It is not the average cost of each unit, taking into account all input costs.

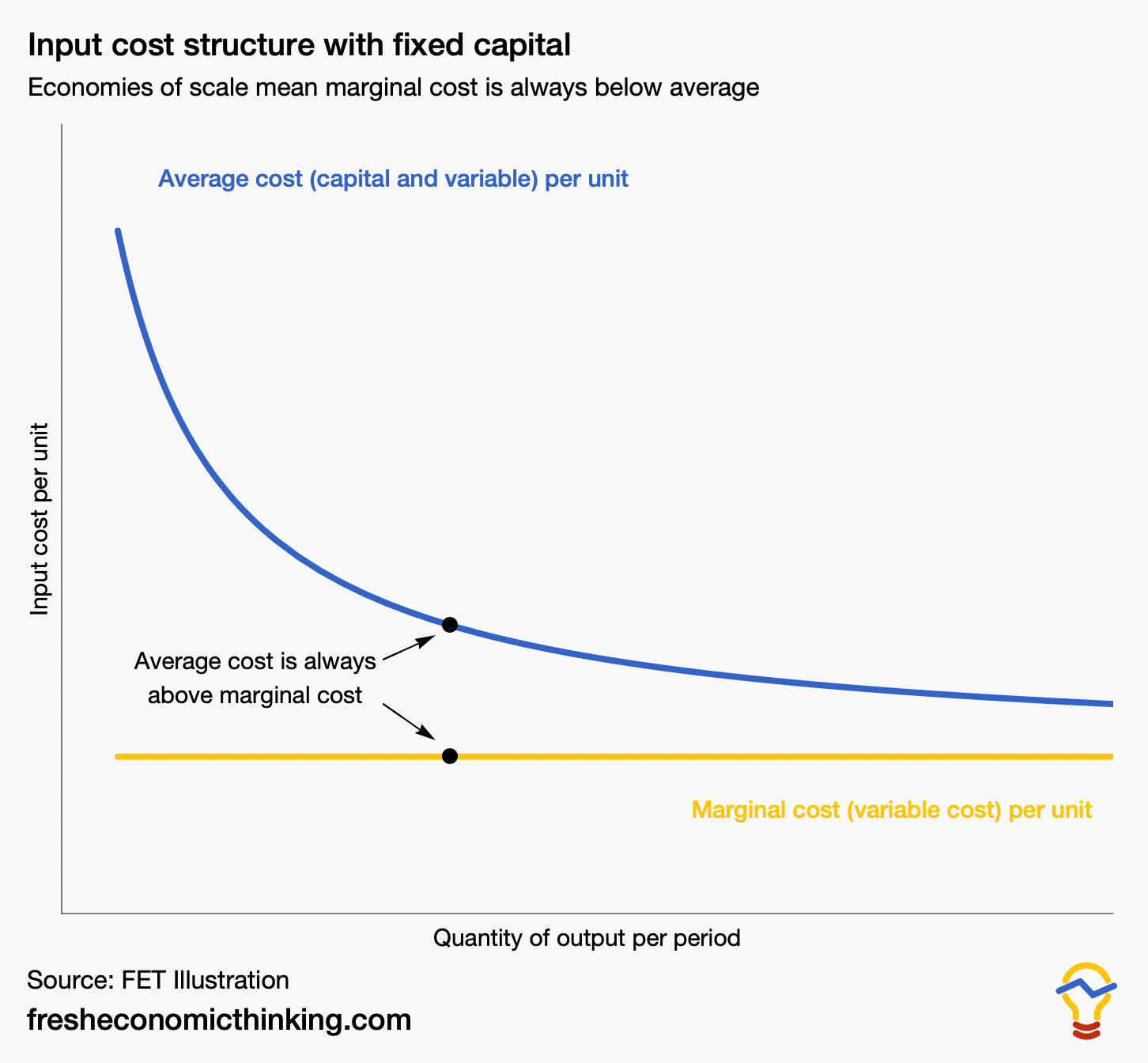

The image below helps differentiate the two cost concepts. It shows the output per period on the x-axis and the cost per unit on the y-axis. The average cost is the blue line, which includes the per-unit share of the capital costs. The more you produce per period, the lower the average unit cost because you are spreading the capital cost among more units.

The yellow line is the marginal cost of extra inputs needed to produce one more unit per period (for example, material inputs), ignoring the cost of capital.

Industries with any capital requirement and economies of scale will have a higher average cost than marginal cost. So, pricing at marginal cost means that the cost of capital investment can never be recouped.

Economies of scale are especially important in the case of city-wide utilities and large manufactories, meaning average cost and marginal cost will be vastly different, and this is why this was a major topic of economic interest in the 1940s.

The standard economic theory, then and now, says that marginal cost equal to price is socially optimal. But reality is that this can’t be true unless all capital investment is subsidised.

Hence the controversy.

A simple modern example could be software. Here, the cost of production is only in creating the code. The marginal cost of someone downloading and using an extra unit of that code is basically zero. But if the price were zero, no one would produce software because they could never cover the cost of producing it in the first place.

Standard economic reasoning of the time, and frankly, of today, is that a price of zero is the socially optimal price of this software.

So something is wrong here.

Where they went wrong

The wrong part is that marginal cost, being the opportunity cost forgone from selling in this period, and the input cost of production based on what was actually paid for capital and variable inputs, are being conflated in economic theory.

Many students of economics notice this.

They finish their first lessons on opportunity cost and sunk costs, then they get to the idea of firms and production, and the concept of cost is switched to input costs. Opportunity cost is waved away with the assumption that all input costs include a normal rate of return.

What is that normal return?

Oh, just what you could earn elsewhere on your dollar invested. But of course, you can only get a normal return elsewhere if other industries are pricing above marginal cost, and indeed above average cost!

This also presents problems because we know that market-clearing in all markets happens when rising supply curves (i.e. the willingness to sell different quantities at different prices) intersect with falling demand curves (i.e. the willingness to buy different quantities at different prices).

So how do we reconcile this? Subscribe to read on and indulge your inner econ nerd.