How to get a decent public return from Australia's gas resources—A 25% export tax? Or something else?

I explain how a scaled variable royalty does the job of a super-profits tax while avoiding the accounting trickery in order to share risk and get a better public return from resources.

Have you heard that Norway taxes their gas at 78% of profits, but Australia’s offshore gas pays next to nothing in terms of royalties or resource-specific payments? Yes, Australia has a Petroleum Resources Rent Tax (PRRT), which is meant to do the job of Norway’s oil and gas taxes. But it never seems to raise much in revenue, despite recent global gas price booms.

My mates at The Australia Institute (TAI) and Konrad at Punters’ Politics have been banging the drum about this for years. Now, Senator David Pocock is calling for a 25% levy on gas exports.

I highly recommend a paid subscription—it also gets you a big discount on my upcoming in-person workshop in Brisbane on the 9th and 10th of June.

There are TWO WEEKS LEFT of discounted early bird prices.

Tickets here, and a PDF event flyer with full details is downloadable below.

Charging a market price for the right to extract minerals is not some socialist fantasy. Australia’s states own the property rights to onshore minerals and energy resources, while the federal government owns the property rights to offshore deposits.

It is the purest capitalist logic that the owner of a resource should act in a commercial manner and negotiate a market price for the right to that resource from those who extract it.

The tough question is how to price these resource rights.

Three common ways to price resources

State ownership

The first way for a government to capture resource rents is to own (partially or fully) both the resources and the company that leases those resources for extraction, refinement and sale.

Globally, this is one of the most common ways to ensure that excess profits during a resource price boom are shared with the state resource owner. It avoids the need for an extra layer of pricing and is akin to a business owning the building it operates from rather than renting it. However, it also entails the state taking financial risks on the major capital investments necessary to extract oil and gas.

The table below is from my 2024 report with Tim Helm, Rent-controlled resources: Why are we under-charging Australia’s mining tenants? It illustrates how common this approach is. Indeed, so successful is this approach in places with low-cost oil and gas reserves that resource profits replace a massive amount of taxation. Many Gulf nations, such as Saudi Arabia, have no taxes and fully fund their public sector from oil profits.

Special taxes on resource profits (super-profit taxes)

The PRRT is a type of super-profits tax that applies to offshore oil and gas in the federal government’s jurisdiction.

The PRRT essentially first allows the resource lessees a certain rate of profits, which are caught in the regular tax system. But after a certain amount of profit, a special extra tax applies to those super-profits above that.

Back in 2017, there was a review into the PRRT, which was raising very little revenue despite the expansion of offshore oil and gas.

Why not? If profits were high, the tax should raise revenue. Maybe profits weren’t high?

Right there is the catch with trying to tax super-profits. Profits are an accounting construct. There are many margins to play with to reduce top-line revenue, increase costs, and reduce bottom-line profits for the purposes of tax.

The PRRT built in features like allowing generous escalations of carried-forward losses, which do not apply in the regular tax system, and have been the main mechanism for reducing profits in the special accounts subject to the PRRT.

Imagine how this type of mechanism for paying rent to a resource owner would work for a business tenant paying rent to a shopping centre landlord.

The landlord would ask the business tenant, “Did you make any excess profits last year?” The tenant would produce accounts they have created to show that, no, in fact, they didn’t, and the two might then argue about it in an unending game of cat-and-mouse.

To avoid this nonsense, most landlords charge a market rent regardless of the income of the particular tenant.

Norway is able to administer such taxes more effectively as the state there is also a part owner of all facilities tapping their gas resources.

My submission to the 2017 PRRT review is attached below.

Royalties

Instead of taxing the bottom line profit, after the accountants have gone to work subtracting everything they can from the top line, a resource owner can simply charge for the resource based on top line revenue from resource sales, using a royalty.

This is the standard way Australian states charge for their onshore mineral and energy resources. Royalties are also common in other areas of property, like intellectual property, where owners of rights get a percentage share of top-line revenues from books, music and so on.

This is exactly what David Pocock and TAI are proposing for offshore oil and gas—a top-line tax of 25% of revenue.

Since a royalty applies to the top line, the rates are typically much lower. Coal royalties in New South Wales, for example, are about 10%. Iron ore royalties are about 7.5% in Western Australia.

These are simple to enforce, as we can just send the tax man to the port or rail line to check production volumes and prices, and companies generally have an incentive to be honest with investors about high top-line revenues and business growth.

The problem with fixed royalty rates is that price variation is high over time and across resources

A 10% top line royalty on gas revenues seems better than the PRRT for offshore oil and gas. In fact, that is what I proposed to the PRRT review back in 2017 as a replacement for the PRRT.

But, as you might imagine, the simplicity of a fixed royalty rate has a trade-off.

Resource markets are characterised by:

large variations in costs of extraction across deposits, and

large variations in the market price of the tradeable resource over time.

Property markets will often vary prices by location and time. For example, the price to rent a holiday home varies not only with its location, but also over the year, being much higher during peak periods like school holidays.

The illustration below shows how the variation in costs of extraction across different resource locations means a fixed rate royalty cannot share in the economic rents of lower-cost resource deposits and will discourage higher-cost deposits from being worked.

On the left, we see resource deposits ordered from Deposit A, with the lowest extraction cost, to Deposit F, with the highest cost. A fixed rate royalty will reduce the net-of-royalty price, shown by the decline in the orange price line. The shaded grey area is the royalty revenue.

Notice that the lessee of Deposit A gets a huge excess profit, or super-profit, but Deposit F becomes uneconomical because the net-of-royalty price is not high enough for the lessee to earn a return on the capital they need to invest to begin working it.

On the right, we see a situation in which property owners price optimally to leave only a small super-profit for each lessee. Each gets a normal return on capital invested, but the resource property owner collects more from Deposit A, a little less for Deposit B, and so on, while collecting nothing for Deposit F.

This would maximise the return to the resource owner while ensuring maximum output of the resource. This is the intended way the PRRT and other super-profit tax regimes operate.

In Australia, we do make some adjustments to royalty rates to reflect the differing costs of extracting different resources. For example, in New South Wales, coal royalties are 10.8% for open-cut mines and 8.8% for deep underground mines

But the other pricing issue is the variation in price over time, which can be much more important than variation in extraction cost across deposits of the same resource in the same jurisdiction.

The next illustration shows what happens when the price of the tradeable extracted resource doubles.

On the left, with a fixed royalty, the resource owner gets the same proportion of the higher revenue, so revenue doubles when there is a doubling in price. But the actual amount of excess profits may have tripled, or more, as shown on the right.

So fixed rate royalties, when prices are low, make marginal deposits uneconomical, and when prices rise, collect only a small proportion of the excess profits available.

How to make royalties work better

After this little economic lesson, what should we make of a 25% royalty on gas exports?

I think it is probably good politics but bad policy.

Yes, a 25% royalty rate when the gas price is abnormally high would be good. But gas prices rise and fall quickly.

Let’s have a quick look at the market.

Asian gas prices are high relative to the last two years at 19 USD per MMBTU. But not excessively so. Prices were half of that just months ago.

A 25% tax at, say, $20/MMBTU equals $4, leaving a net-of-royalty $16/MMBTU for the gas lessees. But at a $10 price, the same 25% leaves lesses only $8 net of royalties. At a $5 market price, they receive just $4 net of royalties.

When the global price is $20, states should probably charge more than 25%. But if the price is $5, they should charge a lot less.

Other than shifting to gameable resource super-profits taxes, what can we do?

The solution is to apply a variable royalty that operates much like progressive income taxes, with higher marginal rates at higher resource market prices.

Queensland has applied this approach to gas and coal in recent years, raising billions in extra revenue during the post-COVID resource price spikes.

Below is the Queensland royalty schedule for liquid petroleum. The royalty rate is 3% of revenue below a price of $50/bbl, with a marginal rate of 11.5% applies for prices from $50/bbl to $100/bbl and a marginal rate of 12.5% applying above $100/bbl.

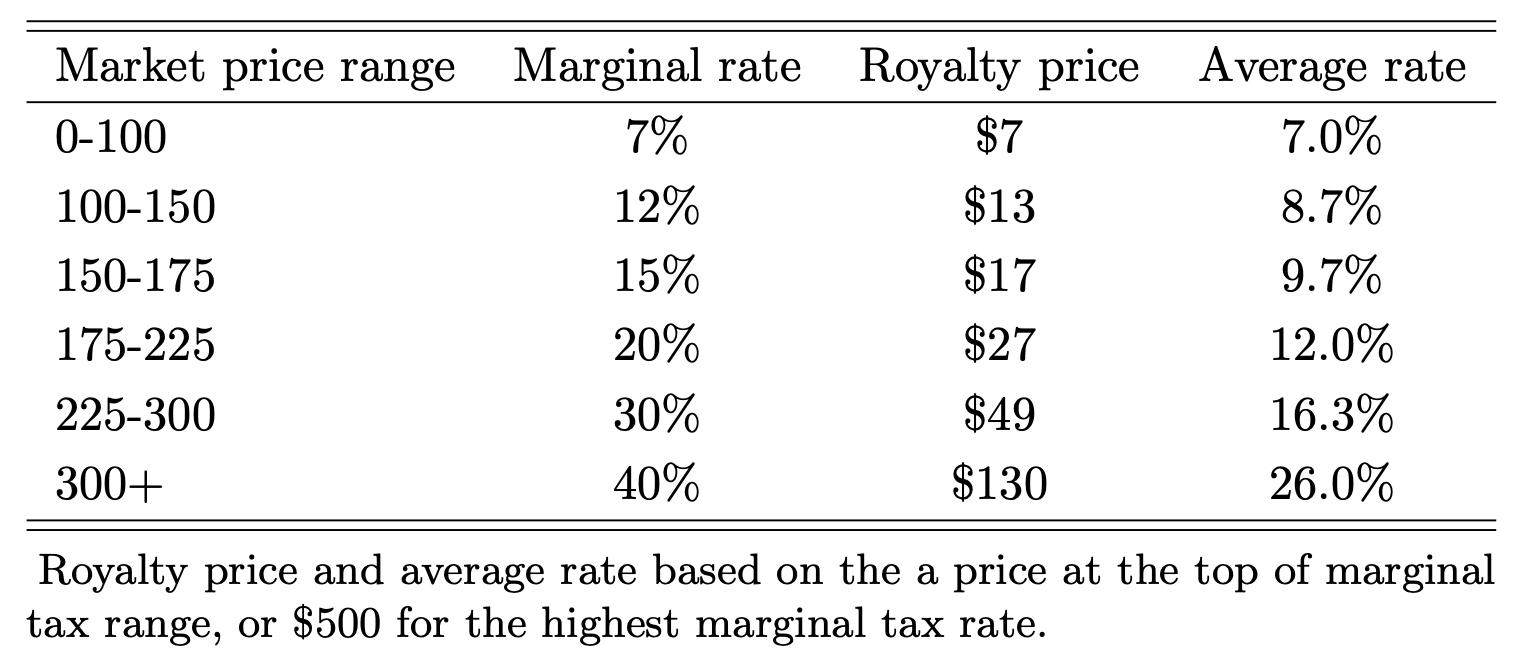

For coal, the approach is shown below, with marginal rates rising from 7% to 40%. Notice that the royalty price rises more than in proportion to the market price. This is exactly what it should do to capture super-profits.

This is the type of aggressive variable royalty schedule I would apply to offshore gas. Yes, states should charge a high marginal and average royalty when the price is abnormally high, to get a share of the boom. But they should also charge a much lower rate when the price is low. Variable royalties do just that.

Variable royalties are also a feature of privately negotiated prices. Often, intellectual property royalties are like this—the more books you sell, the higher the royalty rate you get. Applying variable royalties to resources seems te me to be a more commercial approach for government resource owners than fixed royalties.

A final royalty design tweak

You might notice that defining market price thresholds and percentage rates in a royalty schedule opens up the same problems as leaving income tax brackets fixed over time. What about inflation? What about bracket creep?

We have indeed had substantial inflation since Queensland’s variable coal and gas royalty schedules were introduced in 2022. A $100 coal price doesn’t leave mining companies and their shareholders with as much profit as it used to, especially when their input costs have risen by nearly 50% over the past few years. That is certain to lead to ongoing lobbying and endless efforts at the back end of state government to work out what kind of adjustments are necessary.

Tim Helm and I proposed that instead of fixing nominal brackets and dealing with these problems, states could instead scale the royalty rate based on the ratio of the current resource price to a long-term median price metric. This would allow for a set-and-forget approach with only one political bargain over the base rate of royalty.

The formula would take the ratio of the current benchmark price, or the current price received by a firm with longer-term contracts, and the median market price over a long period, such as 10 years. Then it would apply this scaling factor to a base royalty rate.

So if the base rate is 7% of revenue and the current market price of the extracted resource is the same as the 10-year median, the miner pays a 7% royalty.

But if the miners are receiving double the 10-year median during a boom period, they would pay a 14% royalty. This results in a royalty price that scales with the square of the current price relative to the long-term benchmark, which is exactly the kind of more-than-proportional growth in royalty revenue the schedule of marginal tax brackets is trying to achieve.

The beauty of this model is that resource prices can boom by many multiples, but cannot fall below zero. So there is a massive asymmetry of price variation to the upside relative to the median 10-year price.

The attached documents below explain this in more detail and show various simulations. They show that adopting this type of scaled variable royalty would have raised about $15 billion per year in extra revenue if applied to coal, iron ore and gas over the decade from 2013 to 2023.

So what?

The debate about taxing gas needs to have some sensible economic logic behind it. A 25% flat royalty on the top line might be fine if gas prices never fall substantially. But we know that resource markets are subject to booms and busts.

A scaled variable royalty can achieve the same outcome in a boom, and an even higher average royalty during very large price booms, while scaling back automatically when resource prices inevitably fall again.

Combine this approach with different base rates for deposits with quite different extraction costs and states could end up with nearly the full effect of an economically ideal super-profits tax without any of the accounting trickery.

As always, please like, share, comment, and subscribe. Thanks for your support. You can find Fresh Economic Thinking on YouTube, Spotify, and Apple Podcasts.

Why not just charge 5% per annum on the declared unimproved value of the resource with the option to buy the lessee out at his own valuation?

Part 2 of my comment follows.

My view is that royalty regimes taking a percentage of nett in situ value have been too readily dismissed. Let's look at two reasons for dismissal that have been suggested by Cameron.

It was claimed that the Petroleum Resource Rent Tax (PRRT) has not collected enough money for government, in contrast to the Norwegian regime that is based on realised nett value of petroleum resources in situ. That is a reason to prefer and look seriously at the Norwegian regime, not to reject all regimes purporting to be based on realised nett value.

The PRRT rate is much lower than the Norwegian rate. Also, the PRRT allows carry-forward of undeducted expenditures at ridiculously generous, arbitrarily determined rates of interest (to "play safe"). This has been accompanied by an exploration tenement regime that induces explorers to bring forward exploration to find something so as to obtain secure tenure. This incentive has been reinforced by the high carry forward rate. Together, these arrangements undermine the base of the PRRT and consequent revenue. In contrast, the Norwegian Government adopted a "go slow" policy that avoided premature exploration to capture tenure. Also, it avoided allowing ridiculously high carry forward rates. The Norwegian system has evolved over time, and it is now a cash flow levy that captures economic profit by effectively exempting the relevant firm's actual minimum required rate of return from the levy (sometimes called a Brown tax, as it was put forward by E. Cary Brown (1948)). So, it avoids the PRRT flaw of allowing unduly high carry-forward rates. If governments want to avoid immediate refunds to explorers for and development of natural resources that accompany a cash-flow based regime, they could guarantee future full deductibility and therefore drop the carry forward rate under a resource rent royalty/tax to or close to the long-term bond rate. They could also require carry forward of unrecovered depreciation of exploration and development expenditure, rather than the outlays as spent. These things are explained in the Henry Tax Review report (2009).

It has been claimed that administration difficulties and costs associated with effort to avoid a levy on realised nett value in situ or economic profit are reasons to opt for another form of royalty regime. However, the Norwegians have been able to administer a levy on realised nett value in situ, and collect a vast amount of money after deducting administration costs. Why can't Australians do this too? Can't we learn from the Norwegians? I believe we can.

If there is a large amount of money at stake, surely it is worthwhile to engage smart people to work out how to collect that money and then do so. The Norwegians did.

The Norwegians sensibly recognised that the levy rate needs to be kept well below 100 per cent to avoid an incentive not to realise the nett value in situ. Cameron reported that the Norwegians still collect 78 per cent. Surely, we can too. They have shown that it is not necessary to set a low rate like the PRRT rate of 40 per cent.

If we want to collect a higher proportion of realisable nett value than 78 per cent or if we think that rate provides too much incentive to avoid the levy, competitive cash bidding could be used to allocate exploration tenements. Making bids deductible or not when calculating liability under the levy on realised nett value will alter the timing of government revenue. Cash bidding also would help avoid dissipation of realised nett value through premature exploration to capture tenure.

The suggestion by a commentator to impose a levy on unrealised value of resources in situ at the tenement holder's valuation with a government option to acquire it at that valuation is worthy of consideration.

Nearly 60 years ago, Mason Gaffney made a case for imposing a levy on unrealised value of resources in situ (Extractive Resources and Taxation, Madison: University of Wisconsin Press, 1967, pp. 402-409). He observed that the assessment or valuation was an obstacle needing to be addressed. The option proposal would be a good place to start in overcoming this obstacle.

I am not a fan of the type of royalty regimes favoured by Cameron and Tim that apply higher marginal rates to revenue at higher prices. These regimes ignore costs which differ between commodities, between extraction operations, and between units of extraction/production within an operation. These regimes do not adjust automatically to differences between prices and marginal costs. They require constant tinkering to adjust to changing realities. Critics often focus and make misleading statements about the level of higher rates, but a commonly overlooked issue is the level of lower rate settings. These can cause great damage when commodity prices are falling while marginal costs are rising.

That's enough from me for now to stir up some debate.

Ken Willett