Deceptive debt burdens

“Our grandchildren will inherit the government's debts” is a common phrase. But it is wrong, and economists should point that out. But many still believe it.

The fact that many economists still think that government debts are a burden on future generations is a puzzle to me.

There is one right answer.

No.

There are two reasons for this, as I noted in this tweet.

The first is somewhat obvious. Every debt liability is another’s loan asset.

Your mortgage? Your debt liability and the bank’s loan asset. Government debt? The government’s debt liability and the bondholder’s loan asset.

Every debt comes with a corresponding asset. By definition.

That should be the end of it.

But even if you, for some reason, did not accept this, and still think that the cost of debt can be passed into the future, this would still not burden our grandchildren.

Because if the current generation can push burdens into the future, so can our grandchildren. We’ve discovered a magic time-travelling solution to all our debt problems!

Modelling tricks

One of the ways people will “prove” that debts can be a burden for future generations is with an overlapping generations (OLG) model.

But the trick in this approach is that creditors and debtors get relabelled as “generations”. That’s how the rabbit is put in the hat.

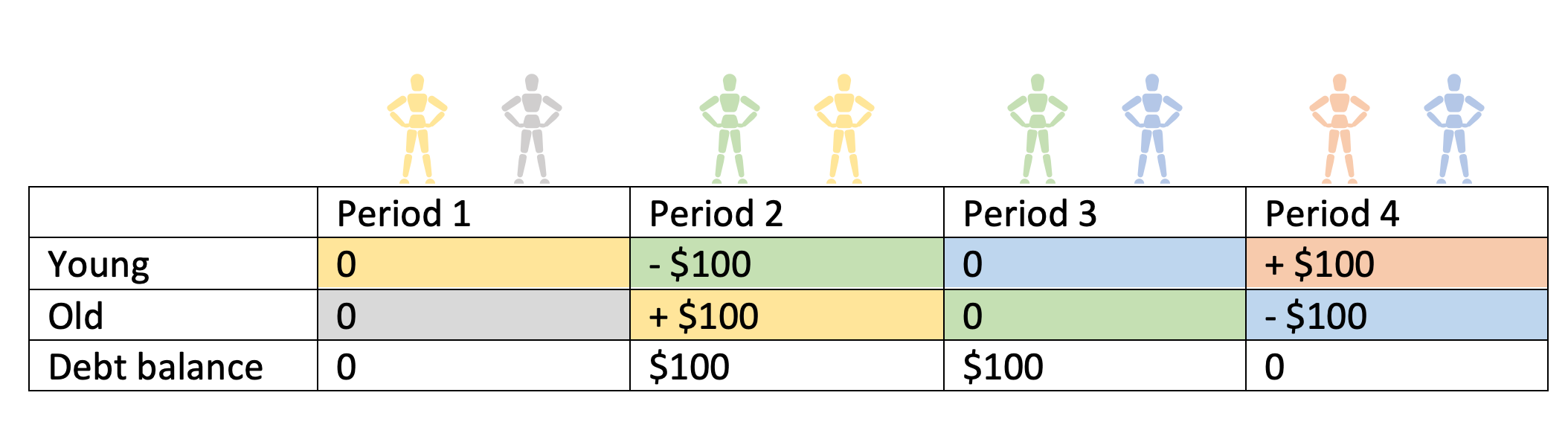

In the table below, I show the basics of the OLG model. In each period, two “generations” are alive, with each generation represented by a colour. The cells in the table are shaded with their colour (i.e. the yellow generation is young in Period 1 and old in Period 2).

The numbers in the cells in the table are the size of the net transfer that takes place between generations using debt. In Period 2, we show the government borrowing from the green young generation to give the old yellow generation $100, creating a debt balance of $100 that carries forward into the future.

Then, in Period 4, the government repays the debt by paying back the young from the old.

On balance, we can see that the yellow generation, that lived in Period 1 and Period 2, was able to consume $100 of extra goods over their lifetime because of the debt taken out in Period 2. The future blue generation, that lived in Periods 3 and 4, consumed $100 less in their lifetime because they repaid the debt when they were old in Period 4 that they did not incur.

So it seems like the debt taken out to give the yellow generation money cost the future blue generation that wasn’t even alive at the time.

But this is silly. In Period 2, there are creditors and debtors. In Period 4, debtors repay creditors. Generations don’t repay each other. Governments repay bondholders. Those bondholders will be the descendants of the green generation who gave up the resources initially to facilitate the debt (i.e. buy the bonds).

Why is the blue generation paying the red generation, neither of which was alive at the time of the debt being incurred? The red generation could just as easily repay the blue generation. After all, we are just arbitrarily assigning creditor and debtor roles to future “generations”.

We can also see in this simple model that the economic cost of the debt is paid when it is taken out. The green generation transfers resources to the yellow generation in Period 2. The transfer is complete. The debt transferred resources exactly at the time it was taken out.

Counting one side of the ledger

We know debt must transfer resources at the time, not push the resource cost into the future because debts are agreements that can be changed. We can write off debts. If debts could push the burden into the future, we should take out lots of debts and then write them off so as to never have to face that mythical future burden.

Another way to think about this is to ask the question “are financial assets a net benefit to future generations”? The answer here, again, is no. Because the asset is also a liability to others. That Treasury bond asset your grandchildren might end up owning? That’s a liability for the future Treasury. That Apple stock you own? Its value comes from the high profits from future customers, which is a cost (liability) to them.

As I’ve explained before, compulsory saving schemes intended to “pre-fund” retirement income systems don’t actually change the economic transfers involved. They suffer from the problem of merely counting one side of the ledger, the asset side, and ignoring the liability side. The idea of government debt being a future burden suffers from the same problem, but in reverse, of counting liabilities but not assets. And sometimes we trick ourselves into thinking otherwise by renaming creditors and debtors as “generations” in the OLG model.

This ignores several important components:

1. If the federal debt grows faster than GDP - which it is now - this causes interest rates on government debt to rise steadily. To fund these interest rates, the government either has to a). raise taxes, b). cut spending, or c). monetize the debt via some form of money printing. There is no fourth option. This means that deficit spending to fund entitlement spending guarantees that future generations will either receive less, get taxed more, or suffer higher rates of inflation that erode savings.

2. The amount of money in circulation is unrelated to the total value of goods and services in the economy. When the government spends more than it takes in to fund entitlement spending, it allocates more scarce resources to those receiving benefits at the cost of those who do not. Whether or not future generations "inherit the debt" is irrelevant to the fact that we currently allocate nearly half of the federal budget to citizens who will not produce any economic value until the day that they die. That is a generational transfer given that demographics dictates that those benefits will not be available for younger generations.

3. Much of the spending on older generations is non-productive or flows out of the US economy. Purchases of imports, international travel, care provided by immigrants who send money out via foreign remittances, and medical care for seniors with incurable, terminal illnesses all results in no long term benefit or return. Whether we should allow these things or not is a policy choice; whether they have long term benefits for the American people is simply not in dispute.

The whole idea that there is a magic money glitch where you can simply borrow as much as you want for as long as you want without consequences is an absurd farce. If something doesn't pass the common sense test, it simply will not work regardless of how many complicated accounting schemes attempt to show otherwise.

You haven't lived in the Global South, obviously. Cost of debt is inflationary, especially when graft & corruption (& in the Global North, rorts) is involved. I hope Australia doesn't learn the hard way.