Harvesting housing supply

There is a common thread between the boom in lumber prices in the U.S. and dynamic models of housing supply.

That common element is that lower interest rates make it optimal to both harvest trees slower and build new homes slower. Let me explain.

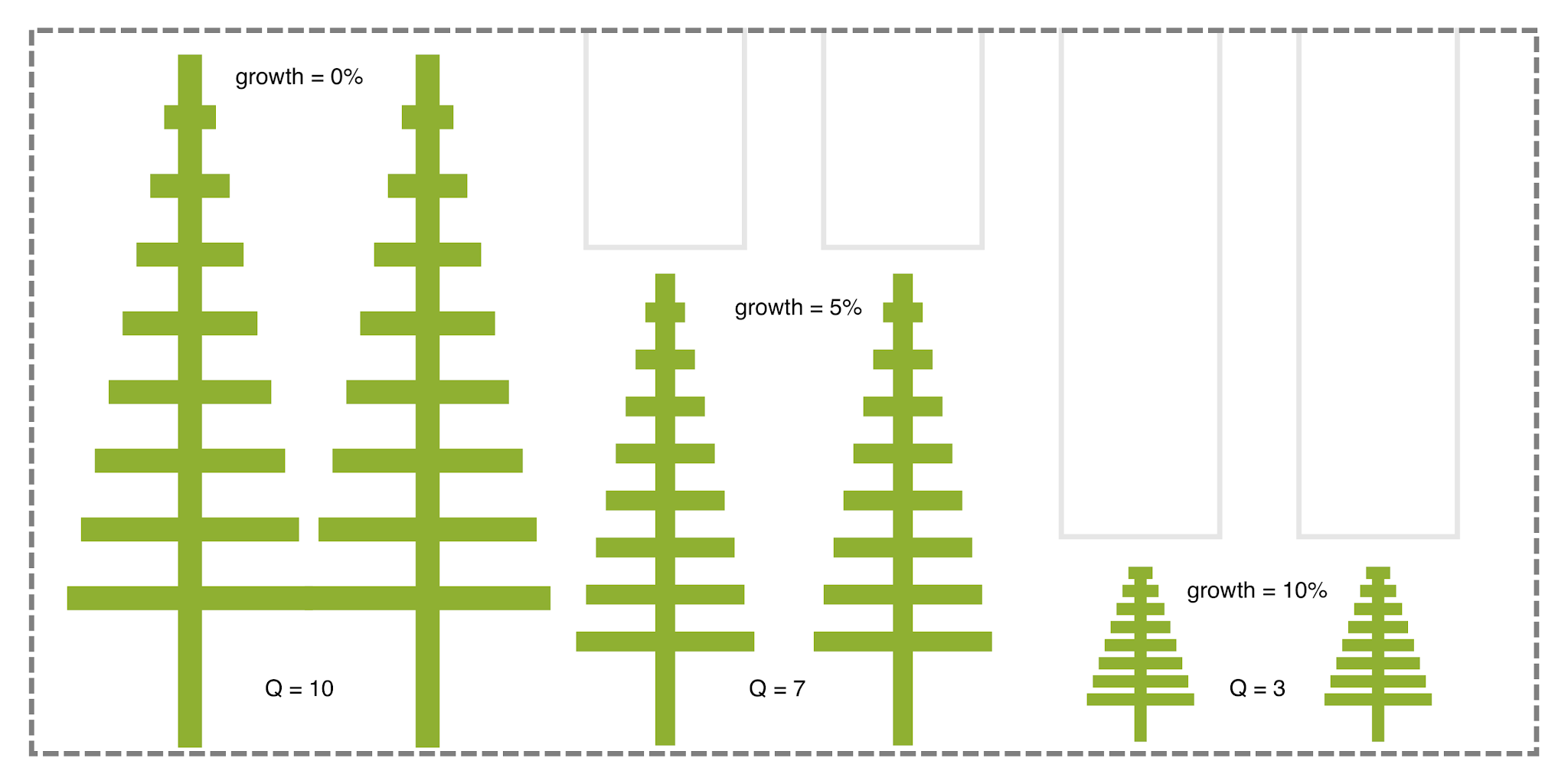

Take a look at the diagram below representing a forest with trees at different stages of growth.

The stock of potential timber from trees at different stages of growth is marked as Q. So 10 tonnes of large trees, 7 tonnes or medium trees, and 3 tonnes of small young trees. A total of 20 tonnes of timber there.

But each stand of trees with a different maturity has a different rate it grows per year. Young trees accumulate timber faster (proportionally) than older trees. The growth rates for the trees in each stand are marked—the oldest grow at near enough to 0%, the next at 5%, and the youngest at 10% per year.

Given this forest with a stock of 20 tonnes of timber, how much is optimal to harvest each year?

The trick to thinking about this question is to realise that the trees are assets, quite literally growing in value each year. When you harvest a tree you are swapping a "tree asset" for a "cash asset". The way to tell what is optimal is to compare the return from the tree asset that you give up to get the return from the cash asset. For example, if you can earn a 7% return from cash, you won't harvest a tree that is growing in size, and hence value, by 10% per year. It's a losing trade to give up 10% to get 7%.

In this forest, we harvest 10 tonnes this year if the interest rate is below 5%, and 17 tonnes if it is above 5%.

When it comes to forest management, lower interest rates mean slower harvesting of timber. If interest rates fall from 7% to 3%, then all the trees growing at a rate between 3% and 7% per year should be left to grow rather than be harvested and replaced with saplings. This is well understood when it comes to harvesting forests.

But it is not well understood when it comes to "harvesting housing development opportunities".

Undeveloped urban land is a lot like a tree—it grows in value without being developed (harvested). Like our forest, we don't just develop all land as soon as the revenue exceeds the cost. We optimise the rate per period to maximise value from the site (or set of sites). This is why developers stage housing subdivisions as much as possible.

A lower interest rate changes the trade-off between owning undeveloped land and getting cash from development. It makes a slower pace of housing development optimal, all else equal.

Not all else is equal, obviously. The price adjustment to lower interest rates generates demand that new housing supply responds to—interest rates are not the only factor. In the last 20 years, we have relied on this temporary demand-boosting effect of interest rate reductions to generate supply, but this has led to structural low-interest-rate conditions that will not encourage supply when demand falls.

In housing, optimal harvesting is called the "housing supply absorption rate". I explain it here.